CarMax, Inc. (NYSE: KMX), America’s largest retailer of used cars, is seeing a continuation of its downward trend as the firm reports its fiscal Q3 2023 financials. The car retailer posted $6.51 billion in revenue, a decrease from Q2 2023’s $8.14 billion and Q3 2022’s $8.53 billion.

Total retail used unit sales fell 20.8%, while comparable store used unit sales fell 22.4%. However, “margin management” helped keep gross profit per retail used unit at $2,237, in line with the preceding year’s third quarter.

In terms of wholesale, units sold fell 36.7%, yielding gross profit per unit of $966, a $165 per unit reduction from the previous year.

“Our third-quarter results reflect the continuation of widespread pressures across the used car industry. Vehicle affordability remained challenging due to macro factors stemming from broad inflation, climbing interest rates, and continued low consumer confidence,” said CEO Bill Nash in the earnings call.

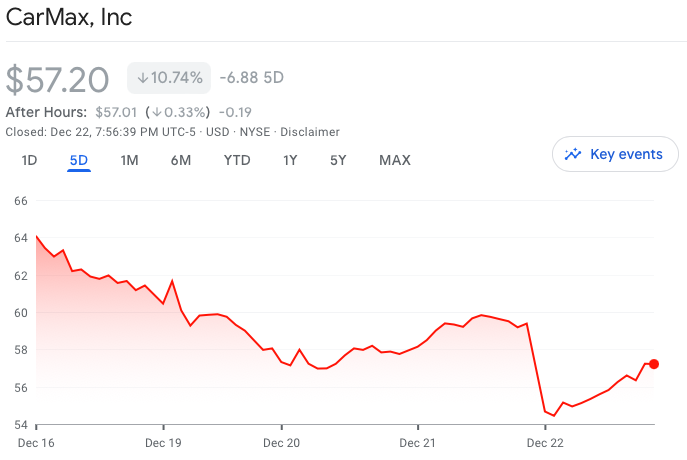

The firm’s share price fell sharply by 12% at the opening bell following the news.

The chief executive added that the firm is “taking deliberate steps to support our business for both the short term and for the long run.”

“Actions that we took during the quarter include further reducing SG&A, selling a higher mix of older, lower-priced vehicles, slowing buys in light of the steep market depreciation, maintaining used saleable inventory units while driving down total inventory dollars more than 25% year over year, raising CAFs consumer rates to help offset rising cost of funds, pausing share buyback to give us capital flexibility, and slowing our planned store growth for next fiscal year to five locations while maintaining our ability to open more locations if market conditions change,” he added.

SG&A for the quarter ended at $591.7 million, 2.7% higher from the third quarter of last year. The car retailer got a $22.6 million settlement from a class action lawsuit in the third quarter of the previous year. After adjusting for the settlement, SG&A spending would have decreased by 1.1% year on year.

“We’re not going to provide guidance [for SG&A] on how much down in the fourth quarter because, again, there’s some variability quarter to quarter. But what I’d tell you is our expectation is that it will be down year over year,” CFO Enrique Mayor-Mora said in the earnings call.

The expense line item was in focus at the Q3 2023 earnings call, with one question clarifying why the firm can’t give a guidance on SG&A. As noted by William Blair and Company analyst Sharon Zackfia, the firm has maintained the expense would decrease year-on-year but still continues to “proactively manage” the spending as if it’s expected to increase.

“Well, we expect to continue to see SG&A kind of to go down. I think on an individual quarter, it gets a little bit challenging to give you a number that we’re managing to. Many things can happen in the quarter,” Mayor-Mora answered. “But what I’d tell you is thematically and practically, we expect to continue to manage our SG&A down from a year-over-year basis.”

In terms of pushing older type of vehicles, Nash admitted that “not everybody wants an older, higher-mileage type of vehicle that’s less expensive.”

“So, again, that’s all driven by demand. And as we see consumers continue to demand that, we’ll continue to put that out. But again, not everybody is — not everyone is looking for that,” the chief executive added.

Due to substantial market depreciation and our response to purposely slow buys, the firm said it purchased 238,000 vehicles from consumers and dealers, a 39.8% decrease from last year’s record third quarter.

“One of the reasons our buys were down so far obviously, depreciation was the biggest lever, but there’s also — we made some decisions just to slow down buys. And so, there were retail cars that we purposely did not buy because of the risk of those cars in a highly depreciating type of market,” Nash explained in the earnings call.

The chief executive noted that they’re “kind of living a very similar life to what we did after the ’08 and ’09 recession” but maintains that they’re “in a better position today than [they] were back then just because [their] self-sufficiency is so high.”

As far as managing inventory, the firm was able to bring it down to $3.41 billion from last quarter’s $4.67 billion and last year’s $4.66 billion.

“This is where I think we really shine when it comes to inventory management… We really worked hard to clean up a lot… The aging inventory, it’s one of the reasons why you didn’t see more movement in our ASPs, our average selling prices, given the depreciation,” Nash noted.

CarMax Auto Finance or CAF’s overall interest margin percentage–which measures the spread between interest and fees charged to consumers and our funding costs–was 6.7% of average managed receivables, down from 7.2% in the prior year’s third quarter, as the firm started to increase its customer rates but were offset by rising funding costs. The weighted average contract rate, however, grew to 9.8% in the third quarter, up from 8.3% in the previous year’s third quarter.

“CAF penetration is up in tandem with actually us raising rates. I think that’s something we’re really pleased about. We know that generally, you’re going to lag the market. Again, we’re competing with credit unions at the higher end, but I think we’ve done a fantastic job at raising rates 40 basis points sequentially, 150 basis points year over year, and still capture that penetration,” CAF Operations Senior Vice President Jon Daniels said.

The firm also said that it is taking a conservative approach to its capital structure “given third quarter performance and continued market uncertainties.” Hence, the firm is pausing its share repurchase program. In Q3 2023, the retailer bought back around $2.6 million of shares and ended with $2.45 billion remaining balance for the program before the halt.

“We remain committed to returning capital back to shareholders over time and may resume share repurchases in the future at any time depending upon market conditions and our capital needs,” the firm said in its release.

Finally, on slowing store growth, the firm only opened one new retail location in Oceanside, California during the quarter. For fiscal 2024, the retailer eyes opening five new locations.

Given the number of actions taken, the results look like they might take time to take effect. Net earnings for the quarter declined to $37.6 million, down from $125.9 million last quarter and $269.4 million last year. The bottomline translates to $0.24 earnings per share.

“We believe we’re well positioned to navigate this environment, and I do think we’ll emerge an even stronger company,” Nash ended in the earnings call.

CarMax last traded at $60.14 on the NYSE.

Information for this briefing was found via Edgar and the sources mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.