The COVID-19 pandemic triggered a global economic crisis, sending shockwaves through financial markets. In a report titled “A Review of the Bank of Canada’s Support of Key Financial Markets During the COVID-19 Crisis,” authored by Joshua Fernandes and Michael Mueller of the Financial Markets Department of the Bank of Canada (BoC), an insightful account of the Bank’s actions during the crisis is documented.

The report details how the BoC responded to the deteriorating liquidity in core Canadian fixed-income markets, successfully restoring market functioning and supporting the Canadian economy’s stabilization and recovery.

“COVID-19 was first detected in December 2019. By late February 2020, new cases began to rise around the world, and global financial markets began to price in the risk of a significant reduction in economic activity. Between February 21 and February 28, the S&P 500 declined by around 12%. During this period, the TSX 60 declined by nearly 10%, and liquidity in Canadian fixed-income markets began showing signs of deterioration,” the report started.

In light of the gloomy economic outlook, the BoC responded, reducing the policy interest rate from 1.75% to 1.25%. This action aimed to ease financial conditions as markets were still relatively functional, and the BoC was actively monitoring liquidity in the financial system.

However, the economic impact of the pandemic rapidly became evident. A staggering one-third of Canadian businesses reported a revenue decline of 40% or more in the first quarter of 2020 compared to the previous year. March 2020 saw the loss of over one million jobs and a significant reduction in working hours for more than two million individuals. This economic downturn further reduced household disposable income, leading to decreased consumer spending and dwindling household wealth due to the devaluation of investment portfolios amid pandemic uncertainty.

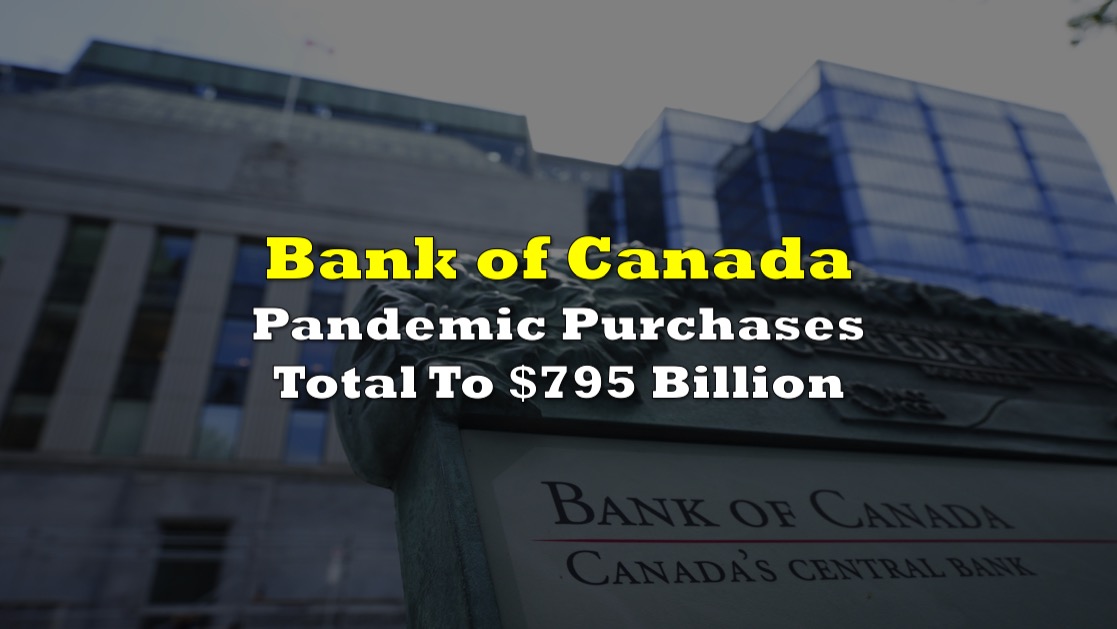

$795 billion

In response to the mounting stress in Canadian fixed-income markets, the BoC launched a suite of extraordinary programs designed to restore market functioning and ensure continued access to credit for businesses and households. These measures supplemented the interest rate reductions and other governmental support efforts.

In a summary within the report, it was revealed that the BoC “provided liquidity and support to markets through extraordinary programs and facilities” through asset purchases during the pandemic. The total of said purchases is a staggering $795 billion.

🚨🚨 NEW

— Tablesalt 🇨🇦🇺🇸 (@Tablesalt13) October 11, 2023

The final tally of Bank of Canada asset purchases during the COVID-19 pandemic is $795 Billion. pic.twitter.com/rmNEuIR7AI

The BoC’s programs were strategically crafted to address critical markets essential to the Canadian economy, supposedly focusing on:

- Easing market-wide liquidity strains

- Restoring market functioning

- Supporting the stabilization and recovery of the Canadian economy

The programs were divided into three phases. Phase 1, spanning March 12 to 31, 2020, saw the implementation of most of these programs as the BoC lowered the policy rate to its effective lower bound of 0.25%. These programs supported commercial banks’ access to funding and ensured the functioning of corporate, provincial, and Government of Canada debt markets.

Phase 2, running from April 1, 2020, to May 6, 2021, introduced additional purchase programs to further bolster the corporate and provincial debt markets. Over time, as market functioning improved and conditions in key markets stabilized, the BoC reduced its program usage. Many programs were gradually phased out during the year, except for the Government of Canada Bond Purchase Program, which shifted its objective to providing monetary policy stimulus through quantitative easing.

The Bond Purchase Program by the government had the highest tag price at $339 billion, followed by the program on extended term repo facility at $215 billion.

The report, written by BoC experts, was praising highly the central bank’s actions, stating the Bank “had to intervene quickly to ensure that markets continued to function and that credit continued to flow in the Canadian economy.”

“We document the stresses in financial markets during the COVID-19 pandemic and how these stresses abated after the Bank’s interventions: the Bank’s interventions helped ease market-wide liquidity strains, restore market functioning and support the stabilization and recovery of the Canadian economy,” the report concluded.

While the report outlines the BoC’s actions, a full evaluation of these programs against central bank intervention principles was deemed beyond its scope. Interested readers were referred to a separate source which suggests that the Bank’s programs were generally well-designed and executed.

However, the report also highlights areas where program design and implementation could be improved for potential future use.

“Potential improvements include providing increased clarity about programs’ objectives and success measures, making program duration more flexible and taking a more punitive approach when accepting certain collateral types for repo operations,” the report ended.

Earlier this month, a research paper written by Soyoung Lee of BoC’s Financial Stability Department conducted a quantitative analysis of the effects of debt relief as a stimulus policy during economic recessions. Using a dynamic stochastic general equilibrium (DGSE) model that considers the diversity of households’ financial situations, this research looks on the potential benefits of mortgage principal reduction in stabilizing the economy during downturns.

Information for this briefing was found via the sources mentioned. The author has no securities or affiliations related to the organizations discussed. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.