Emerita Resources (TSXV: EMO) has seen a second analyst begin covering the equity. This comes after Mackie Research initiated coverage on the company on June 15 with a C$2.30 price target and buy rating.

Clarus Securities last week initiated coverage on Emerita Resources with a C$4.50 price target and speculative buy rating, saying “Emerita has consolidated an enviable portfolio of advanced high-grade polymetallic projects with significant copper and precious metals credits on the Spanish side of the Iberian Pyrite Belt.”

Clarus says that Emerita’s prized asset would be the awarding of the tender for the Aznalcollar mine which was the largest past-producing mine. The mine has historical deposits, the production of which could be fast-tracked and has massive exploration upside Clarus says. They add, “a final decision on the legal dispute is in sight and we are encouraged by the court rulings to date, pointing to the potential for a favourable outcome for EMO.” Clarus expects that if Emerita wins the legal dispute, there would be an immediate C$225 million to C$250 million appreciation in their market capitalization.

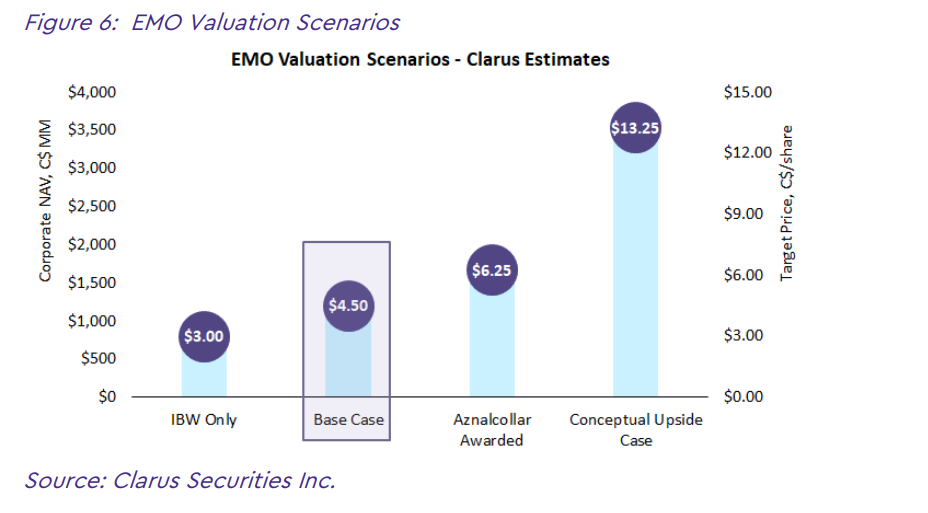

Clarus has provided a matrix for their price target, which ranges from $3 all the way up to $13.25. They say that their base case is $4.50, but that could drop down to a $3 price target if Emerita does not win Aznalcollar. But the $13.25 price target assumes 70Mt at 11.5% ZnEq in mineable inventory (@ 4,500 tpd, ~45-year mine life) at Aznalcollar, which would give the company a C$3.6 billion net asset value or $13.25 a share.

They say that drilling at the IBW offers material upside as many qualified drillers have reported resource estimates and drilling results such as Phelps Dodge and Rio Tinto at the property. The previous drill results ended with a resource estimate of 34.8 Mt, including a high-grade subset of 12 Mt at 12.9% ZnEq. They believe that the drilling done in 2021 could drive a doubling in the companies historic resource towards +20Mt.

If Emerita wins tender to the Aznalcollar mine, the mine is supported by a “massive historic resource” and will have “massive growth potential,” says Clarus. Los Frailes has a large open pittable mine with a historical resource of 71 Mt with a potential underground subset of 20 Mt at 12.6% ZnEq, and Clarus estimates that for every 100 meters of down-dip extension it could potentially add 5-10 Mt of resource.

Clarus ends the report off by saying that Emerita has a strong M&A appeal due to the scale, location, and grades of Emerita’s assets, and if they are awarded the Aznalcollar mine it will “immediately result in the Company becoming a top target for acquisition.”

FULL DISCLOSURE: Emerita Resources is a client of Canacom Group, the parent company of The Deep Dive. The author has been compensated to cover Emerita Resources on The Deep Dive, with The Deep Dive having full editorial control. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security.