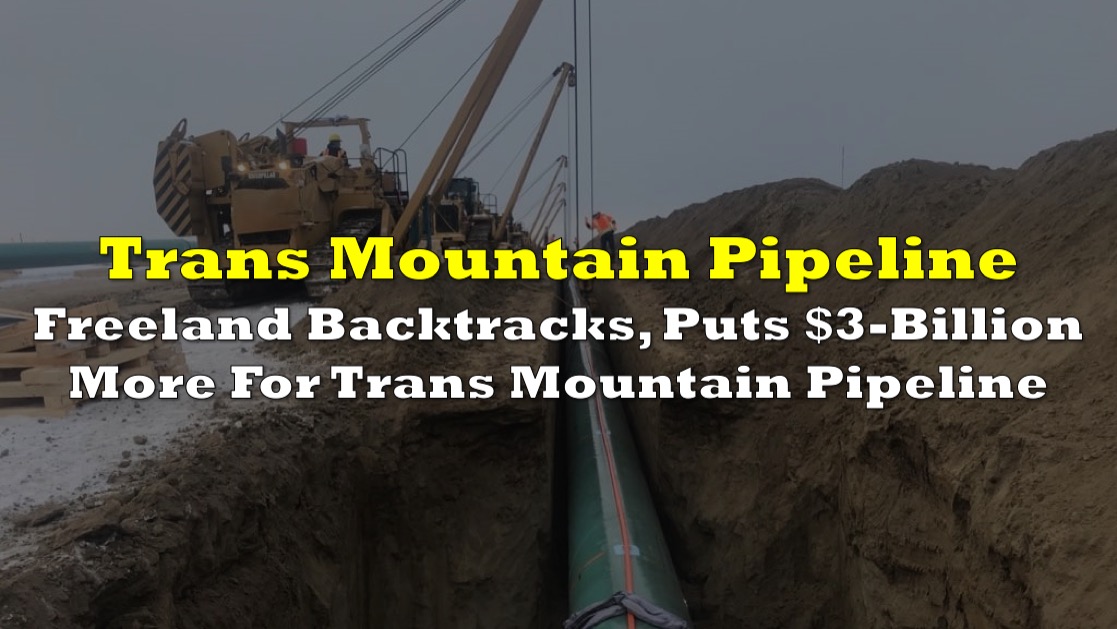

Finance Minister Chrystia Freeland announced a public financing freeze on the Trans Mountain pipeline more than a year ago. Yet on March 24 and May 2, the Liberal Cabinet approved funds for the troubled project to the tune of $3 billion, split between two loan guarantees.

The pipeline is a “integral part of Canada’s long-term energy infrastructure,” according to Marie-France Faucher, a spokesman for Finance Canada. She cited Trans Mountain’s first-quarter financial results, which include a hunt for third-party financing.

“As part of this process, the Government of Canada has provided a loan guarantee on behalf of the corporation,” Faucher said. “This is common practice and does not reflect any new public spending. The company is paying a fee to the government for this loan guarantee.”

Purchasing the pipeline came with significant political risk for the Trudeau government, and it remains a liability for the party as it prepares for the next election, which is due for fall 2025 — unless a vote is called earlier.

In 2018, Trudeau defended the purchase as a way to ensure its construction and the thousands of jobs related with it. The fossil fuel project, with its ever-increasing price tag, is now entering an era in which leaders are judged by their net-zero energy objectives.

The loan guarantees are administered by Export Development Canada (EDC), a federal Crown corporation. Projects that are deemed too hazardous for EDC’s own books are channeled through that account, which requires Cabinet approval when the international trade minister believes transactions to be in “Canada’s national interest.”

The pipeline, which runs 715 miles from Edmonton, Alberta, to Burnaby, British Columbia, was built in 1953 to transport more Canadian oil to Asian markets. The extended pipeline’s construction is expected to be completed in late 2023.

Plans to double the existing pipeline’s capacity to 890,000 barrels per day have been greeted with significant opposition from environmental and Indigenous campaigners.

Years of opposition climax five years ago, when the project’s former owners, Texas-based Kinder Morgan, concluded it was too dangerous and sold, citing political certainty as a cause.

The project is now expected to owe at least $23 billion to lenders.

The project’s cost, originally estimated at $7.4 billion in 2018, has continually risen due to various factors including competition for scarce resources like steel and labour, and the environmental and engineering challenges of the route. The current estimate is $30.9 billion, a sum that raises questions about the project’s profitability. The increased costs cannot be passed on to companies with locked contracts for oil shipment, leading to substantial political and financial liabilities.

According to a Stand.earth report from last year, a consortium of Canada’s largest banks, including Royal Bank of Canada, TD Securities, and the Canadian Imperial Bank of Commerce, has since stepped forward to guarantee the government project.

Ottawa has often tried to appease critics by stating that the government has no intention of keeping the pipeline, preferring to sell it to another company once it is constructed.

The Trudeau government has frequently stated that it is certain that an outside buyer will purchase the project once it is completed.

Information for this briefing was found via Politico and the sources mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.