Ivanhoe Mines (TSX: IVN) is recalibrating the near term trajectory of its flagship Kamoa-Kakula Copper Complex, opting for a more cautious development pace to secure the project’s long-term stability. According to an updated independent technical report released Tuesday evening, the company has lowered its production guidance for the next two years while setting the stage for a significant surge starting in 2028.

The revised mine plan reflects a pivot toward infrastructure development and more conservative underground advance rates. Ivanhoe now expects to produce between 290,000 and 330,000 tonnes of copper anodes in 2026, climbing to a range of 380,000 to 420,000 tonnes in 2027.

Prior guidance called for production between 380,000 to 420,000 tonnes in 2026 and 500,000 to 540,000 tonnes in 2027.

While these figures represent a step back from previous estimates, the company is targeting a new high of over 500,000 tonnes per annum from 2028 onwards. That level of production is then estimated to be contained for a 25 year mine life.

Management characterized the shift as a necessary trade-off to ensure the multi-decade sustainability of the operation. The decision follows a challenging 2025 marked by adverse geotechnical and hydrological conditions, including significant water inflow at the Kakula Mine. By focusing on peripheral development and dewatering now, the company aims to establish a more robust foundation for high-productivity stoping in the future.

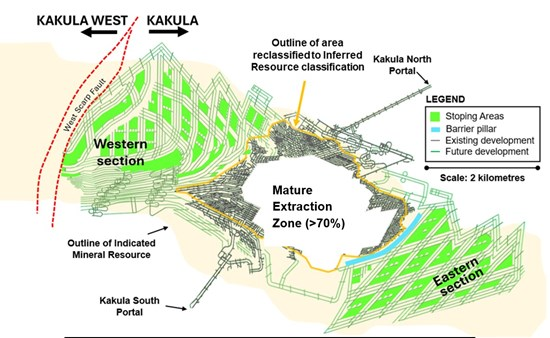

The technical report also provided a fresh look at the project’s scale. Kamoa-Kakula’s reserves sit at 13.1 million tonnes of copper, while indicated mineral resources unchanged at 34 million tonnes copper. Reserves notably fell by 25% versus the prior estimate, a result of the old Kakula Mine being removed from estimates. That removal is a function of mineral being mined, as well as the reclassification of resources due to access being lost to the orebodies.

An optimized feasibility study is also said to be in the works.

Cost structures are expected to fluctuate alongside the development schedule. Cash costs (C1) are projected to peak between $2.60 and $3.00 per pound in 2026 before declining as production ramps up, which is an increase from prior guidance that called for costing of $2.20 to $2.50 a pound this year. By 2028, Ivanhoe expects costs to settle near $2.00 per pound, bolstered by the efficiency of its on-site smelter and new solar power initiatives.

Executive Co-Chairman Robert Friedland remained bullish on the project’s strategic importance, noting that the complex is the epicentre of the world’s richest sedimentary copper district.

“Our mine combines extraordinary grade over a very long life … and we are supported by hydroelectric and solar power. Building on this endowment, this technical report sets a base case from which we will build copper production up to a new high of over 500,000 tonnes per annum,” commented Friedland.

Ivanhoe Mines last traded at $11.89 on the TSX.

Information for this story was found via the sources and companies mentioned. The author has no securities or affiliations related to the organizations discussed. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.