According to a Form S-4 filed with the U.S. Securities and Exchange Commission (SEC) on June 11 by Churchill Capital Corp IV (NYSE: CCIV), the merger between Lucid Motors and special purpose acquisition company (SPAC) sponsor CCIV could close on or around July 23. The new company will be named Lucid Motors and trade on the NYSE under the symbol LCID. This implies that CCIV shareholders will vote to approve the merger a few days before July 23.

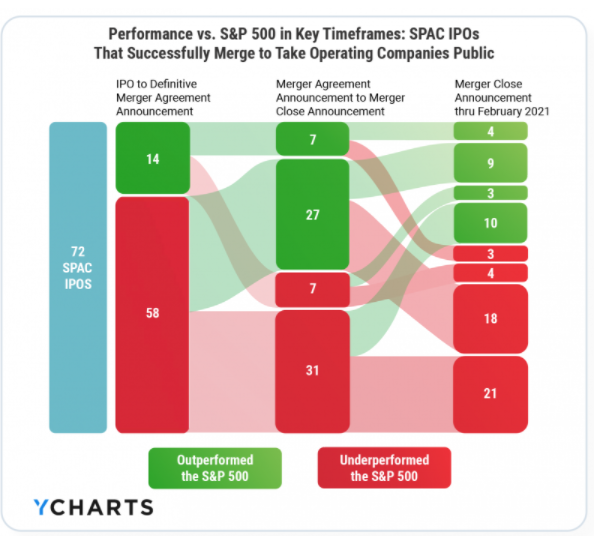

According to a YCharts study of 72 SPACs, a SPAC stock generally performs the best relative to the S&P 500 during the time between the SPAC’s announcement of a merger partner (e.g., CCIV’s February 2021 announcement of its agreement to merge with Lucid) and the merger closure date (~July 23 in this case). After the merger closes, the resultant company tends to not perform as well as during the run-up to closing.

In other words, investors effectively “believe the hype” during the run-up to merger close, but embrace it less after the merger is completed. If this template were to hold for Lucid, investors may want to consider adopting a more measured stance on Lucid Motors after the merger closes.

Lucid Motors Background Information

A SPAC deal was finalized on February 22 between Churchill Capital and Lucid Motors. The equity value of the February Churchill Capital-Lucid deal was announced at US$16.3 billion, and existing Lucid shareholders will receive a value of US$11.75 billion. Factoring in the stakes of the PIPE (Private Investment in Public Equity) investors and the original Churchill Capital SPAC investors, the deal values Lucid Motors at US$24 billion.

Based on Churchill Capitals’s current share price, Lucid’s stock market value after merger close could be around US$40.3 billion (1.6 billion shares times CCIV price of around US$25.18 a share).

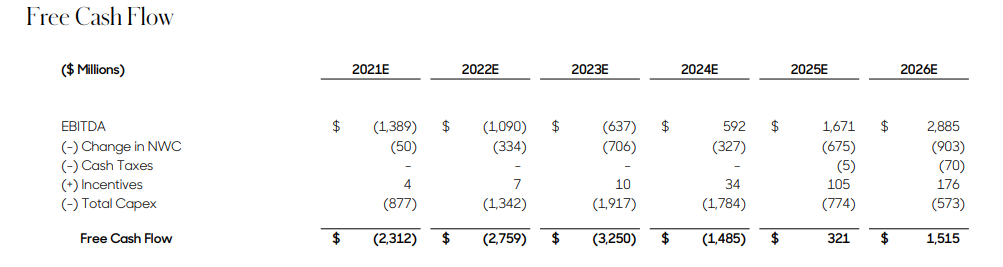

According to its own projections, Lucid will not turn EBITDA positive or free cash flow positive until 2024 and 2025, respectively. By 2025 and 2026, the company expects to realize gross margins of 22-23%. In 2026, the company hopes to generate US$2.9 billion of EBITDA and US$1.5 billion of free cash flow. So, based on estimated 2026 EBITDA, Lucid’s current implied stock market value-to-2026E EBITDA ratio is about 13.9x.

Lucid Air Details and Developments

Lucid Motors plans to include an optional autonomous driving feature in the Lucid Air. “Dream Drive” uses 32 on-board sensors and Light Detection and Ranging (LIDAR), a remote sensing method that uses light in the form of a pulsed laser to measure distances. The company claims the Lucid Air will contain the first embedded high-resolution LIDAR system in a production electric vehicle (EV).

In early June 2021, Tesla canceled the Model S Plaid Plus (500+ miles of driving range and 1,080 horsepower), the most expensive version of its flagship sedan. The company did not disclose a specific reason for its action, but Tesla, like many automakers, has been struggling with supply chain issues, particularly computer chip shortages. As a result of the cancellation, the Lucid Air Dream Edition model (500+ miles of driving range and 1,020 horsepower) will presumably hold the title of the highest-performance production EV on the market.

Bill Expanding U.S. Electric Vehicle Tax Credits Passes Out of U.S. Senate Finance Committee — But Future Beyond That is Unknown

On May 26, a bill increasing tax credits to buyers of EVs assembled by union workers in the United States advanced out of the U.S. Senate Finance Committee by a 14-14 tie vote. According to the potential legislation, vehicles with a maximum retail price of US$80,000 would qualify for a tax credit of as much as US$12,500. The Lucid Air’s price starts at US$77,400.

The bill specifies that the US$12,500 credit would phase out over a three-year period when half of all passenger vehicles sold in the U.S. are EVs. The current maximum tax credit is US$7,500 regardless of the price of the EV purchased. It phases out when an individual auto manufacturer sells 200,000 EVs. The proposed new legislation would eliminate the 200,000 cumulative cap.

A giant obstacle, however, is the virtually complete lack of support by Republicans in the full (50 Democrat-50 Republican) Senate, many of whom represent states where oil and gas industries represent large employers and contributors to the state’s budget due to tax and other payments.

If Lucid were to encounter difficulties in reaching its production targets (timeline and quantity produced), its shares could be affected. In addition, investors currently remain enthusiastic — albeit less so than a few months ago — about the future sales prospects of EVs. If that attitude were to change to a notably less optimistic one, Lucid’s stock could likewise suffer.

Lucid Motors’ merger with SPAC Churchill Capital could close in about a month. Based on historical SPAC trading patterns, Churchill Capital’s stock could perform well into the merger close date. Thereafter, stock performance could become more challenging. At that time, investors could begin focusing on Lucid Motors’ robust valuation, even when based on (potentially optimistic) 2026E results.

Churchill Capital IV Corp (NYSE: CCIV) last traded at US$25.18 on the NYSE.

Information for this briefing was found via Sedar and the companies mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.