The second most significant event in the life of a junior resource company (the first is a buy-out or production) comes when its efforts at developing a project are recognized by a major mining company.

For Max Resource Corp. that moment, after just 7 months into an exploration program on its CESAR copper+silver project, just arrived. On Wednesday, Vancouver-based Max announced it has entered into a collaboration agreement with “one of the world’s leading copper producers”.

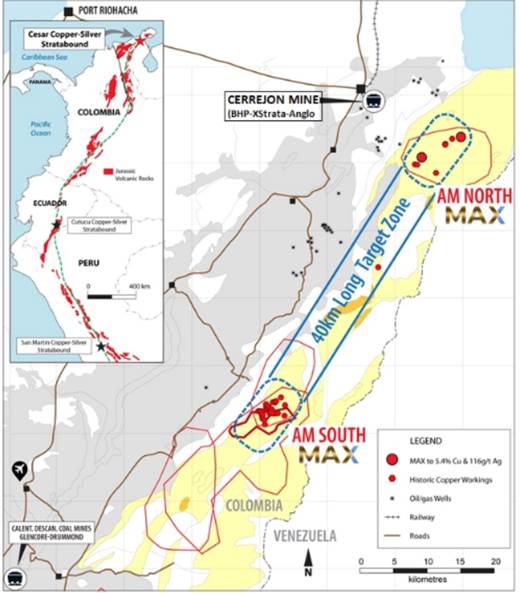

“MAX RESOURCE CORP. (TSXV: MXR) (OTC PINK: MXROF) (FSE: M1D2) is pleased to report it has entered a collaboration agreement with one of the world’s leading copper producers (“Major”) and has brought in Fathom Geophysics (“Fathom”) to carry out a technical study of the Company’s wholly-owned CESAR copper-silver project, located in northeast Colombia, approximately 420 km north of Bogota.”

This article was originally published at AheadoftheHerd.com. The original work can be found here.

The aim of the study is to map stratigraphic (rock layers) features that can help to pinpoint stratabound copper-silver mineral horizons at CESAR.

“Participation of a Major in this geophysical study marks a significant milestone for our Company and provides validation of the CESAR copper-silver project. It combines the expertise of a world-leading copper miner with Fathom’s expertise in characterizing copper-silver deposits and their surrounds,” Max’s CEO Brett Matich said.

The collaboration with the major and the study being carried out by Fathom complements a research program initiated with the University of Science and Technology (“AGH”) of Krakow, Poland.

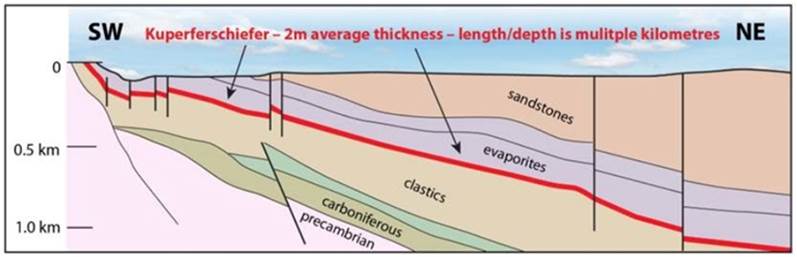

The CESAR project and its potential for hosting a “Kupfershiefer”-type of deposit analogous to a large group of copper-silver deposits in Poland/ Germany of the same name, has grabbed the attention of one of the most important research centers in the world for the study of these sedimentary-hosted stratiform copper deposits which are also large repositories of silver.

In an April 21, 2020 press release, Max says it has sent surface rock samples extracted from CESAR’s stratabound copper+silver mineralization horizons to AGH. Researchers at the university, which has worked extensively with Polish state miner KGHM Polska Miedź S.A., will conduct mineralogical and geochemical studies on the samples; also, a Masters-level student is planning on writing a thesis paper on the results.

AGH has a long history of cooperation with KGHM, the largest copper producer in Europe and the world’s second largest silver producer.

Matich added: “Max’s ability to attract the interest of a major mining company and Poland’s University of Science and Technology, reflects the technical merit of the CESAR project. The field team has now returned to the site with the objective of both expanding the footprint of the CESAR deposit and determining the continuity of the copper-silver mineralization.”

The Vancouver-based company sees similarity of mineralization at the CESAR project to Kupferschiefer as a new giant sediment-hosted copper-silver mineralized system.

Sedimentary-hosted stratiform copper deposits are among the two most important copper sources in the world, the other being copper porphyries. They typically range from 1.6 million to 170 million tonnes copper ore, grading between 0.7% and 4.2%, with a median of 14 million tonnes at an average grade of 1.6% Cu, according to a 2019 academic paper, ‘The Kupferschiefer Deposits and Prospects in SW Poland: Past, Present and Future’.

The Kupferschiefer copper belt that underlies Germany and Poland is among only three giant sediment-hosted copper deposits in the world. It is also within an elite 1% of deposits that contain over 60 million tonnes of copper.

According to the US Geological Survey, the massive volume of metal in Poland’s Kupferschiefer deposits is due to continuous mineralization that extends down dip and laterally for kilometers.

Identified resources within the giant Lubin-Sieroszowice deposit, are 1.6 billion tonnes of ore containing 30.3 million tonnes of copper and 2.7 billion ounces of silver, at average grades of 1.63% Cu and 57 g/t Ag. Reserves are 23.7 million tonnes copper and 1.4 billion ounces silver.

M&A opportunities limited

The problems with the copper industry are highlighted in a very interesting report by RFC Ambrian, a global natural resources adviser and investor.

The research report focused on the availability of greenfield copper exploration and development projects which could be the subject of M&A.

The report cites consultant Wood Mackenzie stating that by 2028, new copper projects are needed to fill a 4-million-tonne demand gap.

It also has Rio Tinto saying that small projects of less than 100,000 tonnes per year copper production accounted for 40% of new production in the last decade, and Anglo American highlighting there are limited new copper supply options and the industry faces headwinds with capital intensity and capital constraints, environmental issues and water scarcity, permitting issues and increased technical challenges.

As for mergers and acquisitions, there were slim pickings in 2019 and this year isn’t expected to log many transactions, either. Last year saw 20 deals valued at US$3.89 billion compared to 28 in 2018 worth $11.56 billion. Among the headline-makers were Zijin Mining’s $1.5B takeover of Nevsun Resources and its Timok mine in Serbia; China Molybdenum’s acquisition of the remaining 24% stake at the Tenke Fungurume copper mine in the DRC; and Jianxi Copper increasing its interest in First Quantum Minerals to 10.8%.

Most interesting from Max Resource’s point of view, in December 2019 BHP, the world’s largest mining company, became the largest shareholder (14.7%) of Sol Gold’s Cascabel project in the Ecuadorian portion of the Andean Copper Belt. The deal followed Newcrest Mining’s purchase of a 1.5% interest in Sol Gold a year earlier, putting its ownership interest at 14.6%. Recently the company secured a $150 million financing from streaming company Franco-Nevada.

The investments in Sol Gold are good for Max because Max’s CESAR project is within the same geological trend as Cascabel, which has an updated 2020 resource of 2.66 billion tonnes at 0.53% copper-equivalent in the measured and indicated category, and 544 million tonnes at 0.31% Cu_Eq inferred.

RFC Ambrian states, It appears that there is a lot of interest in SolGold and a competitive bid could occur if the Cascabel project achieves expectations. We believe there is a High possibility of a third party (including the minority shareholders) looking to acquire the project outright or taking a significant interest in the medium term.

The report gives three reasons for the decline in copper M&A: Many copper companies that are potential takeover targets have difficult shareholding structures; the number of quality asset disposals from existing copper producers is likely to be a lot lower than in the past; and there are a limited number of late-stage development copper projects with resources of greater than 3.0Mt contained copper that are likely candidates to be acquired.

Lower copper prices have also held back investment interest.

According to RFC Ambrian, there are currently 64 exploration projects with resources greater than 2.5 million tonnes of contained copper. Of those, only 19 have the potential for third-party involvement (ie., a major taking a full or partial ownership stake, or providing financing). And within that group, just five projects have a ‘High’ possibility of third-party involvement: Cascabel (Sol Gold), Los Helados, Viscachitas, Casino, and Santo Tomás.

Copper grades are declining, especially in Chile, the world’s leading producer. Of the five projects with a high possibility of M&A, only four have a grade above 0.5% Cu, with a weighted average grade of 0.449% copper excluding by-products.

Conclusion

A report by Roskill forecasts total copper consumption will exceed 43 million tonnes by 2035, driven by population and GDP growth, urbanization and electricity demand. Electric vehicles and associated network infrastructure may contribute between 3.1 and 4Mt of net growth by 2035, according to Roskill.

Back to Max Resource’s news at the top of the article, only 7 months into its exploration program at CESAR, Max is on the radar of “one of the world’s leading copper producers”. The collaboration agreement between Max and the yet-to-be-named company begins with a geophysical study of CESAR, which has already demonstrated enormous potential.

The University of Science and Technology (“AGH”), Krakow, Poland has commenced mineralogy and geochemical studies on CESAR. AGH will use knowledge gleaned from KGHM’s world-renowned Kupferschiefer sediment-hosted copper-silver deposits in Poland as part of the academic study of CESAR.

“Ongoing exploration continues to build confidence in CESAR as a significant discovery of regional scale,” said Max’s CEO, Brett Matich. “The Company is working towards a 3D model to assess the potential size of the CESAR copper-silver project.”

Admittedly CESAR is early-stage, but it is also one of the few copper projects that is demonstrating the massive scale needed to interest a major – and it has, in 7 months.

Moreover, and this is really important, Max doesn’t have to drill it, not at this stage. The whole idea is to identify the mineralized horizons and the dips. So far, Max has managed to do this with rock chip sampling because rivers, streams and creeks cut across and expose the multiple horizons for a considerable depth.

Having a major copper company come in so early – just 7 months into an exploration program – validates Max’s exploration model…and the results.

I see this week’s news release as a critical milestone for developing CESAR and I can’t wait to see what the next stage of collaboration might bring.

Content sourced via Ahead of the Herd, written by Richard (Rick) Mills. Full disclaimer associated with this work can be found at AheadoftheHerd.com.

The Deep Dive, and it’s parent company Canacom Group, has not reviewed the above content and is hereby not responsible for statements made within. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The Deep Dive and it’s parent company Canacom Group holds no licenses.

FULL DISCLOSURE: Max Resource Corp is a client of Canacom Group, the parent company of The Deep Dive. The author has been compensated to cover Max Resource Corp on The Deep Dive, with The Deep Dive having full editorial control. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security.