TD Bank Group (TSX: TD) has reported a turbulent third quarter for 2024, marked by significant financial setbacks and growing regulatory scrutiny in the United States. The bank’s recent earnings report reveals a rare quarterly net loss of $181 million, or 14 cents per share, a stark contrast to the $2.88 billion profit, or $1.53 per share, reported in the same period last year.

The decline is said to be driven by a substantial provision for anticipated fines related to ongoing investigations into its anti-money laundering (AML) practices. On an adjusted basis, the bank earned $2.05 per share, falling just short of analysts’ expectations of $2.07 per share, according to data from LSEG.

The most significant factor contributing to this loss was the bank’s decision to set aside an additional $3.45 billion as a provision to cover potential fines and penalties related to its U.S. AML compliance issues. This latest provision brings the total amount set aside for these potential fines to US$3 billion.

🚨BREAKING: TD BANK TAKES FURTHER PROVISION OF $2.6B ON US LAUNDERING PROBE $TD.CN pic.twitter.com/q8OsAxNEFC

— Smartkarma (@smartkarma) August 21, 2024

$TD $SCHW

— Jane Ellen Radabaugh (@JaneElle90) August 21, 2024

WHAT? It seems like criminal activity in the U.S. is influencing its northern neighbor:

TD Bank takes an additional $2.6B provision in Q3 to account for estimated fines.

TD Bank Group (TD) announced that it is actively pursuing a global resolution of the civil and…

TD CEO Bharat Masrani acknowledged the severity of the situation, stating, “We are fully committed to resolving these regulatory issues and enhancing our compliance infrastructure. The steps we are taking now are necessary to address the challenges we face in the U.S. market.”

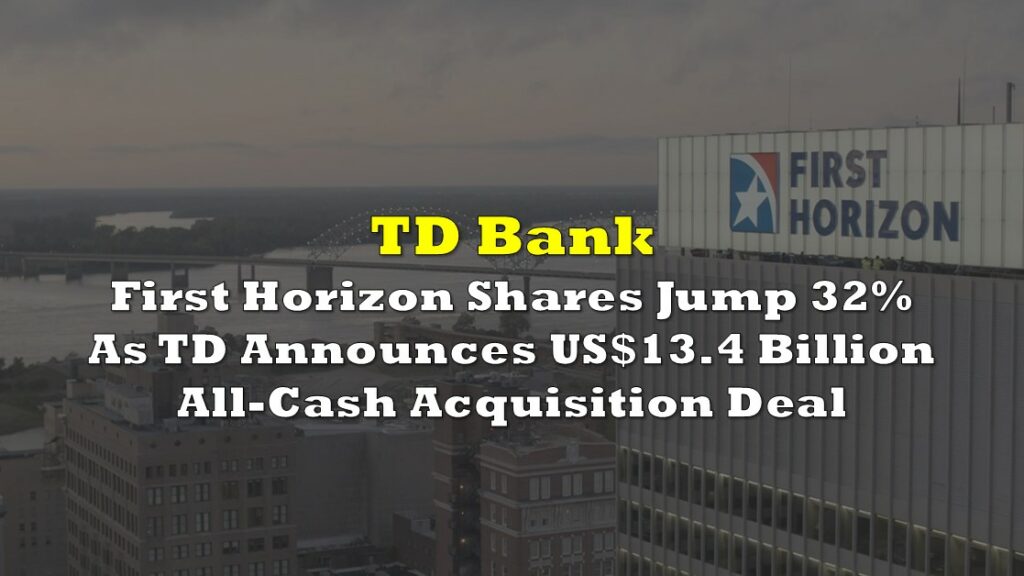

The bank has been under investigation by several U.S. regulators, including the U.S. Department of Justice (DOJ) and the Financial Crimes Enforcement Network (FinCEN), for alleged lapses in its AML program. The probes, which have been ongoing since last year, were a significant factor in the bank’s decision to terminate its US$13.4 billion acquisition of First Horizon Corporation, a deal that would have expanded its footprint in the southeastern United States by adding approximately 400 branches.

The potential penalties facing TD are not limited to fines. Analysts, including Gabriel Dechaine from National Bank, have raised concerns about possible non-monetary penalties, such as an asset cap, which could significantly restrict TD’s ability to grow its loan book in the U.S. “If growth is restricted, TD could deliver sub-par earnings growth relative to peers over the next several years,” Dechaine wrote.

The bank has been actively working on remediating its AML compliance program, including significant investments in risk management and control infrastructure. “We are making substantial improvements in our processes, and we are confident that these efforts will strengthen our position in the U.S. market,” said Masrani.

TD’s U.S. operations, which account for about a quarter of its overall profit, have been a critical growth area for the bank over the past two decades. Through a series of acquisitions, TD has built a network of over 1,100 branches across the eastern United States, more than its total number of branches in Canada.

However, the third quarter saw a 5.6% decline in net income from the U.S. business, primarily due to lower deposit volumes and tightening loan margins. The provision for credit losses also rose to $1.07 billion, compared to $766 million in the same quarter last year, reflecting a more challenging economic environment and higher expected loan losses.

TD Bank’s total loans net of allowance for loan losses increased to $938.3 billion as of July 31, 2024, up from $867.8 billion a year earlier.

Despite these challenges, the U.S. retail segment showed some resilience. TD Bank continued to grow its loan portfolio, particularly in the commercial banking sector, where middle-market loan balances and lending fees increased by 18% and 9%, respectively, on a year-over-year basis.

In Canada, TD’s personal and commercial banking division delivered a strong performance, with net income rising by 13% to $1.87 billion. This growth was driven by a combination of new account openings, volume growth, and margin expansion. The bank also reported a milestone of over 8 million active credit card accounts in Canada, further cementing its leading position in the Canadian market.

However, not all segments performed as well. TD’s wealth management and insurance division reported flat earnings despite recording its highest-ever quarterly revenue of $3.35 billion. The division was negatively impacted by severe weather events in Canada, including wildfires in Alberta and storms in the Greater Toronto Area, which led to higher insurance claims costs.

The bank’s stock has fallen by 5% so far this year, underperforming the broader S&P/TSX Composite Index, which has seen a rise of 8.6% in the same period. The ongoing regulatory uncertainty and the potential for further financial penalties have created a significant overhang on the stock.

In a move to bolster its capital position, TD also announced the sale of 40.5 million shares of Charles Schwab Corporation (NYSE: SCHW), reducing its ownership stake in the U.S. brokerage from 12.3% to 10.1%. This sale is expected to generate significant capital for TD but also signals the bank’s need to manage its financial flexibility amid ongoing challenges.

BREAKING: Charles Schwab falls -4.4% after news that TD Bank plans to sell 40.5M $SCHW shares https://t.co/aS0GoAomoI pic.twitter.com/en1PWENbAt

— Financelot (@FinanceLancelot) August 21, 2024

As TD works towards resolving its U.S. regulatory issues, the bank’s future growth will depend on its ability to navigate these challenges while continuing to invest in its core businesses.

“Looking ahead, TD is strong and well-positioned to navigate the macroeconomic environment, invest in both our AML remediation program and our business, and continue to deepen our relationships with our nearly 28 million customers and clients,” Masrani said, expressing cautious optimism about the bank’s ability to overcome its current difficulties.

TD last traded at $81.29 on the TSX.

Information for this briefing was found via Sedar, Reuters, and the sources mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.