In May of 2020, short seller Muddy Waters had done the dilligence to show that GSX Techedu Inc. (NYSE:GSX), a Chinese online learning platform, was a literal fraud. In one of the more complete, high-detail dissertations we’ve ever seen from an equities researcher, the firm laid out a case that GSX Techedu students were mostly bots.

It’s compelling, and it comes with the backing data, methodology, and clarity of structure that one might expect out of a paper being submitted to the New England Journal of Equities Research for peer review. The veteran researchers were aware that extraordinary claims require extraordinary evidence, and they delivered. A cottage industry of righteous short sellers, who live for this type of thing, jumped on the trade like catnip.

Domiciled in China, GSX lists American Depository Receipts (ADRs) on the NYSE, which trade at a valuation between 100 and 300 times the company’s reported revenue, which has yet to be subjected to a proper audit.

Following Muddy Waters’ initial report, the GSX Techedu short story took on the predictability of an episode of a syndicated TV show. GSX denied the fraud, the shorts doubled down, the Enterprise got locked into a standoff with a Romulan Bird of Prey that couldn’t explain why it was conducting exercises in the Neutral Zone, but wouldn’t leave, either.

By January of 2021, with the price down to $45 and volume drying up, it looked like the shorts might have finally earned some capitulation. Then, out of nowhere, GSX took off like a rocket, running from $45 to $105 in 12 trading days, peaking at a high of $142.50 on no news, the apparent subject of a short squeeze.

This past Friday and Monday, more than 150 million shares of GSX Techedu hit the market like a ton of bricks as the holdings of family office Archegos Capital management was liquidated by its banking partners to cover margin calls, bringing GSX back down to levels not seen since Muddy Waters began calling it an enormous fraud. The company issued a press release Tuesday saying founder and CEO Larry Xiangdong Chen would be buying stock out of the market, which seems to have put a floor under it for now, but its outlook isn’t as interesting as its potential role as an Archegos Capital portfolio component.

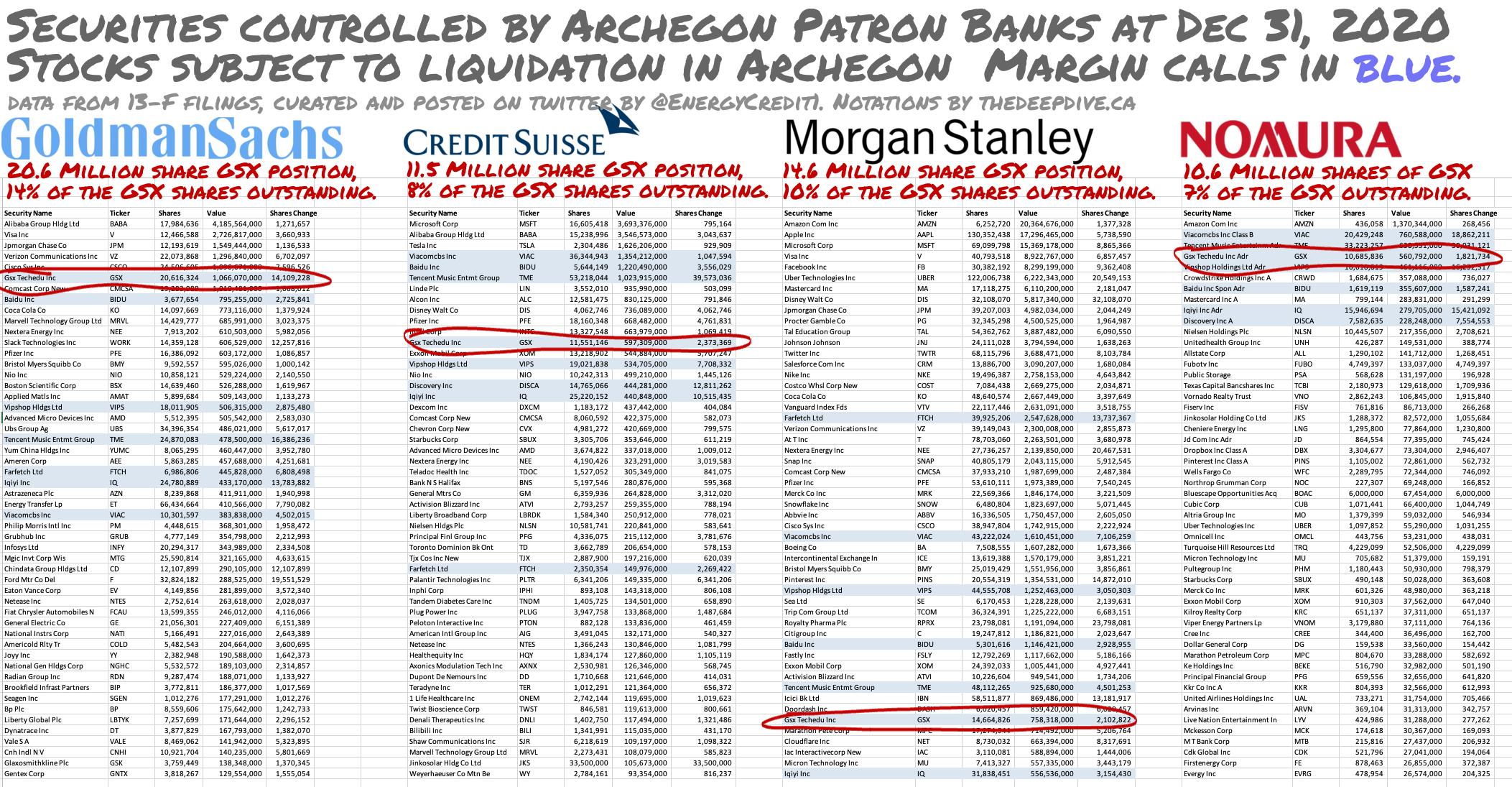

Mid-week, The Deep Dive brought readers an exclusive report on the sum-total of public information available on the liquidation-heard-around-the-world which was, and still is, next to nothing. Piecing together what Bill Hwang’s global network of leverage was holding when it fell apart is a breadcrumbs job, and the trail starts with the assets of the banks that were taken to the cleaners.

An investment bank’s 13-F is bound to have nearly every name in the index, but the particular 13-Fs filed by Nomura, Mogan Stanley, Goldman Sachs and Credit Suisse on the last day of 2020 are notable for the weight carried in GSX Techedu, a $6 billion Chinese correspondence school that’s never seen an audit. Goldman’s 20 million share position represented 13% of the outstanding issue.

“How could they!?”

The response to the Archegos blow up we’re seeing from the friendly set of professional asset managers who have earnest, accessible, public-facing pop-finance profiles has often included puzzlement. Why would anyone play fast and loose with that much money!? Furthermore, how did Masters of the Universe I-banks extend this much credit to a guy like that!? Hwang was sanctioned for market manipulation in 2012 – front running secondary offerings from foreign issuers. The banks knew that he was all about making money stacking the deck. What could they have been thinking!?

The what isn’t all that interesting. Clearly, they were thinking about the fees and interest they could collect writing swaps to a guy pushing that kind of money around on leverage. But the “why” is quite the question. Banks don’t extend billions in credit to just anyone, but they might give a large marker to a player who knows how to create a sure thing.

In a vacuum, making a market jump like it’s on puppet strings is a matter of scale. In much the same way the terminal jockeys on Wall Street Bets used derivatives to create upward pressure on GameStop (NYSE: GME) and AMC Entertainment (NYSE: AMC) that exceeded the weight of their collective capital, a fund that can buy a total return swap from a fee-thirsty bank can conceivably push enough weight around the market to treat a stock like GSX like it’s a pink sheets listing. A high-profile short story, popular with the heads and living on borrowed time, would be a prime target for an operator that generates alpha by using leverage to orchestrate sure things.

Bloomberg cites the ever-chatty “people with direct knowledge,” at Goldman Sachs in a report that Goldman’s compliance department initially killed the idea of taking Hwang on as a client, but changed its mind at some point in the last two years, presumably over-ruled by someone tired of seeing tens of millions in swap fees going to the competition.

“Like boots or hearts, when it starts, it really falls apart.”

The unwinding that shook the banking world played like a sort of vindication for the short sellers who got beat up betting against GSX. The foreign issuer reported record 2020 revenue on March 4th, without going through the trouble of a year-end audit. A year ago, when the company filed its 2019 year end, GSX commissioned an audit opinion letter from Deloitte, the scope of which explicitly excluded internal controls over revenue.

The notion that such an obvious and demonstrable grift could be listed on the NYSE offends the sensibilities of people who believe in capital markets as arenas of price discovery that facilitate investment in businesses, and those people put everyone involved on blast, making sure that anyone who cared to look knew that the natural value of GSX is zero. A bet that it will end up there is a bet that capital markets will eventually settle into a natural order.

But Muddy Waters and its peers may be the last capital markets purists who are interested in order. The NYSE allows for the listing of foreign ADRs without audit. The SEC allows for them to be traded, and the largest banks in the world sponsor the listings, and extend credit to the Archegos of the world so that they can be pushed around. Not only are they not a reflection of the business that issued them, they were never meant to be. They’re the raw material. A medium that capital uses to turn other capital into returns.

Information for this briefing was found via Twitter, the sources mentioned, and the companies mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.