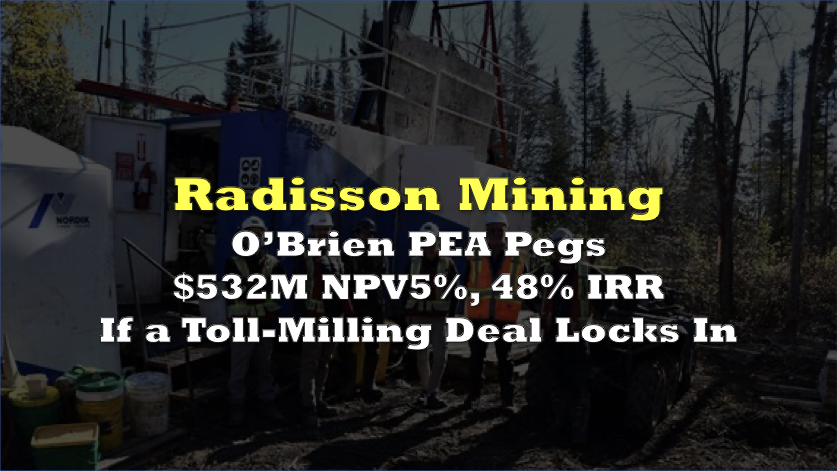

Radisson Mining (TSXV: RDS) has released a preliminary economic assessment that pegs the O’Brien Gold Project at an after-tax NPV5% of $532 million and an IRR of 48% at a gold price of US$2,550 per ounce.

The study leans hard on a toll-milling scenario at IAMGOLD’s nearby Doyon facility, a move that trims onsite costs but leaves Radisson hostage to a “to-be-negotiated” processing contract.

“The result is a low-cost and high-value project should a beneficial milling arrangement be secured,” CEO Matt Manson said. That qualifier is doing heavy lifting.

The mine design calls for an 11-year underground operation, planning to extract 4.57 million tonnes grading 5.0 g/t gold, yielding 740,000 contained ounces. Metallurgical recovery of 87% would send 647,000 ounces of doré to market. Once the ramp-up year is out of the way, annual throughput stabilises at about 1,160 tonnes per day and gold output averages 70,000 ounces. Management pegs after-tax free cash flow in years 2 through 8 at roughly $97 million a year.

Initial capital of $175 million is light by underground standards because the company will truck ore to Doyon instead of building its own plant. Even after adding $173 million in sustaining capital, total life-of-mine capex comes in at $350 million, or $172 for every ounce milled.

Radisson says that upfront spend delivers an NPV-to-capex ratio of 3.0 at the base-case gold price and 5.0 at today’s spot price of roughly US$3,300 an ounce. Life-of-mine EBITDA is estimated at $1.5 billion on $2.26 billion in revenue, giving a 66% margin. After-tax free cash flow over the mine’s life totals $803 million, and the project turns cash-flow positive at a gold price above US$1,260 an ounce.

Operating metrics look competitive: cash costs of US$861 an ounce and AISC of US$1,059 per ounce are achievable only if IAMGOLD’s mill charges remain at the conceptual 30% margin Radisson has inserted into the model. Strip that margin to zero and the after-tax NPV actually rises to $578 million with a 52% IRR, but a 60% margin drags NPV down to $487 million and IRR to 44%.

Radisson’s resource base has swollen thanks to a much lower cut-off grade. The company re-blocked its 2023 model—originally built on a 4.5 g/t cut-off and a US$1,600 gold price—to a 2.2 g/t threshold tied to US$2,000 gold. Indicated tonnes jump 45% to 2.2 million, yet the average indicated grade slips 20% to 8.2 g/t, down from the previous 10.26 g/t. Inferred tonnes explode 317% to 6.67 million, but average grade is nearly halved to 4.4 g/t compared with the old 8.66 g/t figure.

Contained ounces still rise: indicated ounces increase 16% to 582,000 while inferred ounces more than double to 932,000. Roughly 58% of the production schedule relies on that inferred material, making resource conversion a front-burner issue.

The mine plan also depends on exploration success. Radisson has another 50-to-60-kilometre drill program funded through 2026. Management argues that the orebody continues to grow at depth and along strike, but every new drill hole must beat roughly 5 g/t to keep the economics intact.

Radisson Mining last traded at $0.38 on the TSX Venture.

Information for this briefing was found via Sedar and the companies mentioned. The author has no securities or affiliations related to the organizations discussed. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.