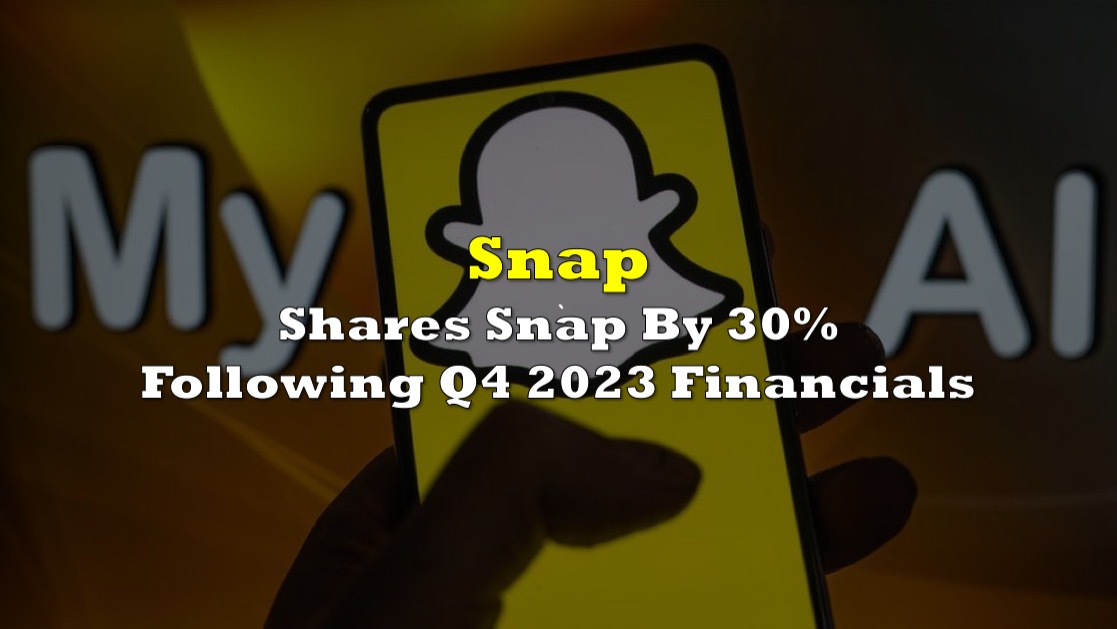

Snap Inc. (NYSE: SNAP), the parent company of popular social media platform Snapchat, faced a significant setback as its shares plummeted by up to 30% in after-hours trading following the release of its fourth-quarter financial results. The company’s performance, although meeting Wall Street analysts’ expectations, failed to appease investors, leading to a drastic decline in its stock value.

Snapchat, $SNAP, is down 30% after earnings.

— unusual_whales (@unusual_whales) February 6, 2024

David Portnoy, before earnings, bought $SNAP $20 calls and sold $15 puts for March.

Both positions will be underwater significantly if $SNAP stays here. pic.twitter.com/JhcdolYmRs

Despite posting adjusted earnings of 8 cents per share, surpassing forecasts of 6 cents, and generating revenue of $1.36 billion, slightly below the consensus of $1.38 billion, Snap Inc. witnessed a sharp decline in its share price. The modest financial gains coupled with a 10% year-over-year increase in daily active users to 414 million were overshadowed by concerns raised by Meta Platforms’ outstanding quarterly performance, which includes Facebook and Instagram.

Snapchat’s shares experienced a similar downward trend in recent quarters, with the stock often dropping immediately after the release of earnings reports. Prior to the after-hours plunge, Snap’s stock had been showing signs of recovery, rising by 4% before settling at $17.46 per share, its highest level in almost two years.

In its earnings release, Snap Inc. projected reaching 420 million daily active users by the end of the current quarter, aiming for continued user growth. Additionally, the company anticipates a first-quarter revenue increase of 11% to 15% compared to the same period last year, expecting revenue to range between $1.095 billion and $1.135 billion.

The broader social media landscape is currently undergoing scrutiny amidst significant disruptions in digital advertising and regulatory concerns. The rise of platforms like TikTok has intensified competition in the industry, affecting established players like Snapchat and Twitter. Notably, Twitter’s trajectory shifted dramatically following Elon Musk’s acquisition in 2022, further adding to the volatility within the sector.

Snap Inc. has been striving to reassure investors by implementing cost-cutting measures, including plans to lay off approximately 10% of its global workforce, equivalent to around 500 employees.

Despite these efforts, Snap’s fourth-quarter revenue fell short of expectations, leading to a wider-than-anticipated net loss. The company reported a net loss of $248 million, or a loss of 15 cents per share, on revenue of $1.361 billion, marking a 5% year-over-year increase. Analysts had anticipated a net loss of 6 cents per share on revenue of $1.38 billion.

Lupton Capital CEO Jonah Lupton criticizes Snap Inc., labeling it as a “complete disaster” due to its poor performance and excessive stock-based compensation practices, which amounted to $1.3 billion in 2023. They express dismay at what they perceive as the company’s misuse of the compensation, considering it one of the worst instances they’ve witnessed.

“I’d ask ‘why aren’t there activist investors circling this dumpster fire’ but I’m guessing the founders have too much control and any activist could not force/motivate change, cost cutting, new management, new board, etc,” he said.

Not only is $SNAP a complete disaster but they somehow found a way to give out another $1.35 billion of stock based comp in 2023.

— Jonah Lupton (@JonahLupton) February 6, 2024

This is probably the worst abuse of SBC that I have ever seen.

I'd ask "why aren't there activist investors circling this dumpster fire" but I'm… https://t.co/sDSdhyiitC pic.twitter.com/ohAIVWCjYl

According to Snap’s letter to shareholders, geopolitical tensions, particularly the conflict in the Middle East between Israel and Hamas, adversely impacted revenue growth by approximately 2 percentage points during the fourth quarter.

Looking ahead, Snap Inc. remains optimistic about its growth prospects, with CEO Evan Spiegel emphasizing the company’s focus on enhancing its advertising platform and expanding its global community. Spiegel highlighted Snapchat’s unique value proposition in fostering relationships and expressed confidence in the platform’s long-term growth potential.

In addition to user growth, Snap Inc. unveiled promising metrics for its subscription service, Snapchat+, which surpassed 7 million paying subscribers in the fourth quarter. The company also announced a new partnership with Spotify to feature highlights from Spotify’s podcasts on Snapchat Spotlight and Stories.

Information for this briefing was found via Yahoo! and the sources mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.