Credit Suisse contributor Zoltan Pozsar has continued his ongoing series about Bretton Woods III where commodities will dictate the new world order. For his last dispatch of the year, he described how the world is now shifting to a multipolar order “being built not by G7 heads of state but by the ‘G7 of the East’ (the BRICS heads of state).”

BRICS stands for the group of five nations: Brazil, Russia, India, China, and South Africa. But Pozsar said that with the poised expansion via rumored applications for Saudi Arabia, Turkey, or Egypt, he took the liberty to round up the current “G5.”

The author focused on Chinese President Xi Jinping’s speech at the recent summit in the Arab states, which for Pozsar is very telling on how Beijing plans to outmaneuver the West in global economy.

READ: This Week In China: Easing COVID Policies, Boosting Property Market, Visiting Saudi Oil

“Fixed income investors should care – not just because the invoicing of oil in renminbi will hurt the dollar’s might, but also because commodity encumbrance means more inflation for the West,” Pozsar said.

In the next three to five years, China is ready to work with GCC [Gulf Cooperation Council] countries in the following priority areas: first, setting up a new paradigm of all-dimensional energy cooperation, where China will continue to import large quantities of crude oil on a long-term basis from GCC countries, and purchase more LNG. We will strengthen our cooperation in the upstream sector, engineering services, as well as [downstream] storage, transportation, and refinery. The Shanghai Petroleum and Natural Gas Exchange platform will be fully utilized for RMB settlement in oil and gas trade, […] and we could start currency swap cooperation and advance the m-CBDC Bridge project.

Pozsar quoted Xi’s speech

In dissecting Xi’s timeline of “three to five years,” Pozsar explained that in market terms, this means that five-year forward five-year inflation breakevens should discount a world in which oil and gas are invoiced not only in dollars but also in renminbi, and in which some oil and gas are not available at low prices (and in dollars) for the West because they have been encumbered by the East.

“My sense is that the market is starting to realize that the world is going from unipolar to multipolar politically, but the market has yet to make the leap that in the emerging multipolar world order, cross-currency bases will be smaller, commodity bases will be greater, and inflation rates in the West will be higher,” the author explained.

He added that inflation traders “should be paranoid, not complacent,” saying that “inflation breakevens do not seem to price any geopolitical risk.”

The dusk of petrodollar, the dawn of petroyuan

Striking a major comparison between Xi’s approach and then-president Franklin Roosevelt with King Abdul Aziz Ibn Saud, Pozsar highlighted that United States was at the time dealing “with a Middle East that had just started to develop.” The West was essentially securing oil flow from the Arab states in exchange for security through arms and revenue stability.

But now, US-Saudi Arabia relations are strained, America is now less reliant on oil from the Middle East owing to the shale revolution, and China ended up being the largest importer of oil.

“Back then, ‘liquidity and security’ were more important for an emerging region; today ‘equity and respect’ are more important for what has become an eminent region,” he described. China, he added, is now offering the latter through what Xi described as “a new paradigm of all-dimensional energy cooperation.”

The synergy put forth as a proposal by the Chinese leader “means not just taking oil for cash and arms but investing in the region in the ‘downstream sector’ and leveraging the regional know-how for cooperation in the ‘upstream sector’.”

“Put differently, ‘oil for development’ (plants and jobs) crowded out ‘oil for arms’ – the Belt and Road Initiative met Saudi Arabia’s Vision 2030 in a big win-win,” Pozsar concluded.

The icing on the proverbial cake? All these will be renminbi exclusive, starting with Xi’s promise that “the Shanghai Petroleum and Natural Gas Exchange platform will be fully utilized for RMB settlement in oil and gas trade.”

“China, already the largest buyer of oil and gas from GCC countries, will buy even more in the future, and wants to pay for all of it in renminbi over the next three to five years.” Pozsar also noted that the Chinese leader communicated this “not during the first day of his visit – when he met only the Saudi leadership – but during the second day of his visit – when he met the leadership of all the GCC countries.”

“GCC oil flowing East + renminbi invoicing = the dawn of the petroyuan,” he summed up.

Renminbi perks: projects, gold, CBDC

There will be numerous opportunities for GCC countries to decumulate the renminbi earned from selling oil and gas to China. Referring to Xi’s remarks, these could range from “the sale of clean energy infrastructure, big data and cloud computing centers, 5G and 6G projects, and cooperation in smart manufacturing and space exploration.”

“Cooperation in the upstream sector” could potentially also include “the joint exploration of oil in the South China Sea.”

Pozsar also noted that the People’s Bank of China (PBoC) reported an increase in its gold reserves for the first time in more than three years.

“Why do China’s gold purchases matter in the context of renminbi settlement? Because at the 2018 BRICS Summit, China launched a renminbi-denominated oil futures contract on the Shanghai International Energy Exchange, and since 2016 and 2017, the renminbi has been convertible to gold on the Shanghai and Hong Kong Gold Exchanges, respectively,” Pozsar explained.

He added: “Money is as money does, and convertibility to gold beats convertibility to dollars.”

READ: Zoltan Pozsar: Gold At $3,600 Is Not Improbable If US Refill Reserves With Russian Oil

Xi also referred specifically to the m-CBDC Bridge project in his speech. The central bank digital currency project, “enables real-time, peer-to-peer, cross-border, and foreign exchange transactions,” and is being undertaken by the central banks of China, Thailand, Hong Kong, and United Arab Emirates. This would conduct exchanges “without involving the US dollar or the network of Western correspondent banks that the U.S. dollar system runs on.”

“In a very Uncle Sam-like fashion, China wants more of the GCC’s oil, wants to pay for it with renminbi, and wants the GCC to accept e-renminbi on the m-CBDC Bridge platform, so don’t hesitate – join the mBridge fast train,” said Pozsar.

To make things sweeter for the GCC, Xi also highlighted starting “currency swap cooperation,” facilitating an easier way for the countries to buy the stuff it needs with China extending loans in renminbi. This can be repaid via the swap lines when China buys oil for renminbi.

“Do take a step back and consider… that since the beginning of this year, 2022, Russia has been selling oil to China for renminbi, and to India for UAE dirhams; India and the UAE are working on settling oil and gas trades in dirhams by 2023; and China is asking the GCC to ‘fully’ utilize Shanghai’s exchanges to settle all oil and gas sales to China in renminbi by 2025,” Pozsar wrote. “That’s dusk for the petrodollar… and dawn for the petroyuan.”

China and the OPEC+

The ascension of petroyuan is not something that is just about to start, it has already been set in motion. Among the OPEC+ countries, Russia and Venezuela are already accepting payments for oil in renminbi at steep discounts.

China also inked the Comprehensive Strategic Partnership with Iran – “a 25-year ‘deal’ under which China committed to invest $400 billion into Iran’s economy in exchange for a steady supply of Iranian oil at a steep discount.” It stipulates $280 billion toward developing downstream petrochemical sectors (refining and plastics) and $120 billion toward Iran’s transportation and manufacturing infrastructure in exchange for energy exports at a minimum guaranteed discount of 12% to the six-month rolling mean price.

The China-Iran agreement has the same spirit to what Xi’s speech is saying at the summit with GCC: “investments in downstream petrochemical projects, manufacturing, and infrastructure… [in exchange for] renminbi settlement.”

“Russia, Iran, and Venezuela account for about 40 percent of the world’s proven oil reserves… the GCC countries account for 40 percent of proven oil reserves as well (with Saudi Arabia accounting for half)… and are being courted by China to accept renminbi for their oil in exchange for transformative investments,” Pozsar summed up.

“To underscore, the U.S. has sanctioned half of OPEC with 40 percent of the world’s oil reserves and lost them to China, while China is courting the other half of OPEC with an offer that’s hard to refuse,” he added.

READ: China Makes Historic Economic Partnership With Saudi Arabia

The remaining 20% of proven oil reserves are located in North and West Africa, as well as Indonesia. North Africa is currently dominated by Russia, West Africa by China, and Indonesia has its own agenda with battery metals, according to Pozsar.

READ: Indonesia: OPEC, But For Nickel; Australia, Canada Say No

Commodity encumbrance

In a nutshell, that is how China is softly imposing the use of yuan in the oil markets, in so-called “three to five years.”

“China will not only pay for more oil in renminbi (crowding out the U.S. dollar), but new investments in downstream petrochemical industries in Iran, Saudi Arabia, and the GCC more broadly mean that in the future, much more value-added will be captured locally at the expense of industries in the West,” Pozsar said.

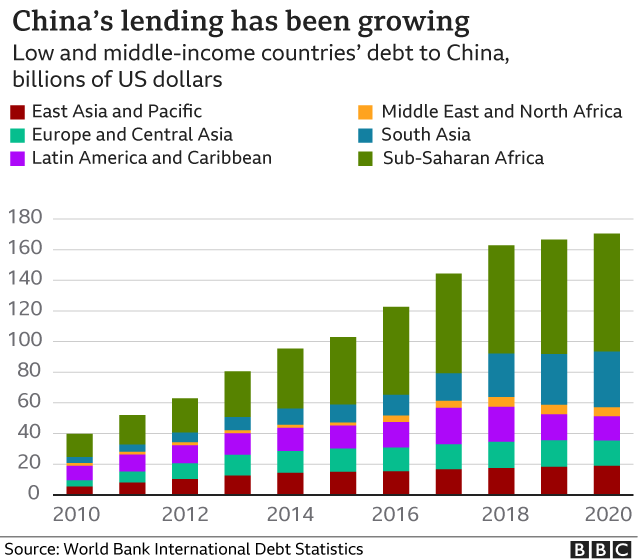

This has played well for China in other non-oil exporting countries. Called “debt trap diplomacy,” many nations are forced into allegiance or giving preference to mainland China in the geopolitical landscape after being unable to repay borrowed investments from Beijing to finance their respective countries’ development projects.

Forbes reported that 97 countries throughout the world are in debt to China, using World Bank data. Countries that owe China a lot of money are largely in Africa, although they can also be found in Central Asia, Southeast Asia, and the Pacific. Pakistan owes Beijing the most money: $77.3 billion, Angola $36.3 billion, Ethiopia $7.9 billion, Kenya $7.4 billion, and Sri Lanka $6.8 billion.

But, it has a different effect to what China is essentially offering the richer GCC nations: “emancipation,” as Pozsar puts it.

“Think of this as a ‘farm-to-table’ model: I used to sell my chicken and vegetables to you, and you sold soup for a markup in your five-star restaurant, but from now on, I’ll make the soup myself and you’ll get to import it in a can – my oil, my jobs, your spend, ‘our commodity, your problem’,” Pozsar explained.

Pozsar cites the first “casualty” of the commodity encumbrance tactic is the decision of the world’s largest chemicals group, BASF, to downsize “permanently” in Europe after it opened the first part of its new €10bn plastics engineering facility in China.

And like anything else, if it can be pledged to be encumbered, it can be rehypothecated.

Pozsar describes how rehypothecation will add value to the budding system: “heavily discounted oil and locally produced chemicals invoiced in renminbi mean encumbrance by the East, and the marginal re-export of oil and chemicals also for renminbi to the West means commodity rehypothecation for a profit.”

This has already started to manifest. For instance, China has suddenly become a big exporter of Russian LNG to Europe and India has become a big exporter of Russian oil and refined products such as diesel to Europe.

BRICS coin

But China is not the only party playing the commodity encumbrance game. On June 22, 2022, at the BRICS Business Forum, Russian President Vladimir Putin noted that “the creation of an international reserve currency based on a basket of currencies of our countries is being worked on.”

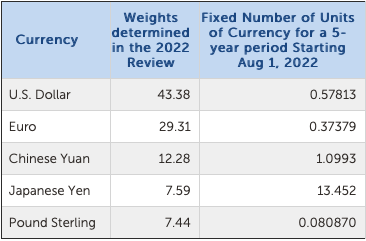

The project is poised to challenge the International Monetary Fund’s Special Drawing Rights (SDR)–an international reserve asset created in 1969 to supplement its member countries’ official reserves. In 2016, renminbi joined the US dollar, euro, yen, and British pound in the SDR basket.

Source: IMF

Pozsar cited the Minister-in-charge of Integration and Macroeconomics of the Eurasian Economic Commission, Sergei Glazyev, who’s also in charge of developing BRICS’s “international reserve currency,” in determining how the new asset would be measured.

“Should [a nation] reserve a portion of [its] natural resources for the backing of the new economic system, [its] respective weight in the currency basket of the new monetary unit would increase accordingly, providing that nation with larger currency reserves and credit capacity,” Pozsar quoted Glazyev. “In addition, bilateral swap lines with trading partner countries would provide them with adequate financing for co-investments and trade financing.”

The project is similar in spirit to Xi’s proposal to the GCC countries (and its debt trap diplomacy): currency swap and downstream development for renminbi settlement.

“The BRICS and other interested nations need to talk about setting up their own independent global financial system – whether it would be based on the Chinese currency or they will agree on something different. They need to debate this,” said Sergey Storchak, chief banker of Russian bank VEB.RF, in an interview at the BRICS summit.

Wide participation among global economies are expected once this project materializes as Saudi Arabia, Turkey, and Iran have all started their application to the BRICS. In addition, the Shanghai Cooperation Organization (SCO) granted dialogue partner status to Saudi Arabia and Qatar (which has half of GCC oil reserves) and began procedures to admit Iran as a member at the last summit in Samarkand.

“The China-GCC Summit is one thing, and China’s strategic partnership with Iran is another, but both Saudi Arabia and Iran applying to pillar institutions of the multipolar world order – BRICS+ and the SCO – at the same exact time, plus the idea of ‘BRICS coin’ as a commodity-weighted neutral reserve asset that encourages members to pledge their commodities to the BRICS ’cause’, should have G7 bond investors concerned, because these trends may keep inflation from slowing and interest rates from falling for the rest of this decade,” Pozsar concluded.

The new paradigm

“The ‘new paradigm’, as I see it, comes with a theme of ’emancipation’,” Pozsar explained. “Both sanctioned and non-sanctioned members of OPEC, with Chinese capital, are going to adopt the ‘farm-to-table’ model in which they will not just sell oil but will also refine more of it and process more of it into high value-added petrochemical products.”

He noted that all growth in global oil production came from US shale and other non-conventional sources such as Canadian tar sands. Saudi Arabia has already restricted boosting output by only one million barrels per day by 2025 while America’s biggest shale oil operator Pioneer Natural Resources recently said accelerating drilling would send investors fleeing and leave the sector “back at the bottom” of the stock market.

“It appears to me that unless the U.S. nationalizes shale oil fields and starts to drill for oil itself to boost production, over the next three to five years, we’re looking at an inelastic supply of oil and gas,” Pozsar noted.

This scenario opens the global oil market and makes it vulnerable for China to come in with its “emancipation” proposal.

READ: Joe Biden Prepares to Frantically Sell Oil From Reserves After Snubbed by OPEC

These supply constraints will lead, as Pozsar puts it, to a position where the “new paradigm” will likely be at the expense of refiners and petrochemical firms in the West, and also growth in the West–“much less domestic production and more inflation as steadily price-inflating alternatives are imported from the East.”

The author drew connection in that when one looks at the yield curve and think about the five-year section and then the forward five-year section, Xi may have accomplished his “next three- to five-year” goal of paying for China’s oil and gas imports exclusively in renminbi and may have advanced commodity encumbrance by developing downstream petrochemical industries in the Middle East “region” of Belt and Road and also the rollout of “BRICS coin” by the time the forward five-year section starts.

“I don’t think five-year forward five-year rates are pricing the future correctly: breakevens appear to be blind to geopolitical risks and the likelihood of the above,” said Pozsar. “Recognize two things: first, that inflation has been driven by non-linear shocks (a pandemic; stimulus; supply chain issues involving laptops, chips, and cars; post-pandemic labor shortages; and then the war in Ukraine), and second, that inflation forecasts treat geopolitics in the rearview mirror.”

Pozsar also said that central banks should think about inflation with geopolitics, resource nationalism, and “BRICS coin” in mind as the next set of non-linear shocks “that will keep inflation above target, forcing central banks to hike interest rates above 5%.”

In April, China will host the fourth Belt and Road Forum after it was postponed in 2021 due to the COVID-19 pandemic.

Information for this briefing was found via Credit Suisse. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.

2 Responses

Not only a superb summary of Pozsar but the first…beating many of the established commentators. Well done, Velasco.

Pozsar is in a league of his own — his insights derive in part from actually reading the transcripts of Xi’s speech (this is never done by the likes of the Financial Times). Now wait to see all the pundits recycling Pozsar’s brilliant thoughts as “their own”. This happened with all of ZP’s prior 2022 notes, each of which deserves wide distribution widely (not just to Credit Suisse clients). At the very least, you can see all the plagiarization that the main stream economic analysts do.

excellent summary off pozsar. he needs to be put in charge