This obscenely overvalued stock market is especially noisy. The information trying to move it flies in from all angles, at as high a volume as it can manage, trying to find a large enough echo to become relevant in the hive mind and create some momentum. The only way to reliably find signal in this chaos of a noisescape is to step back and look at the broader concepts.

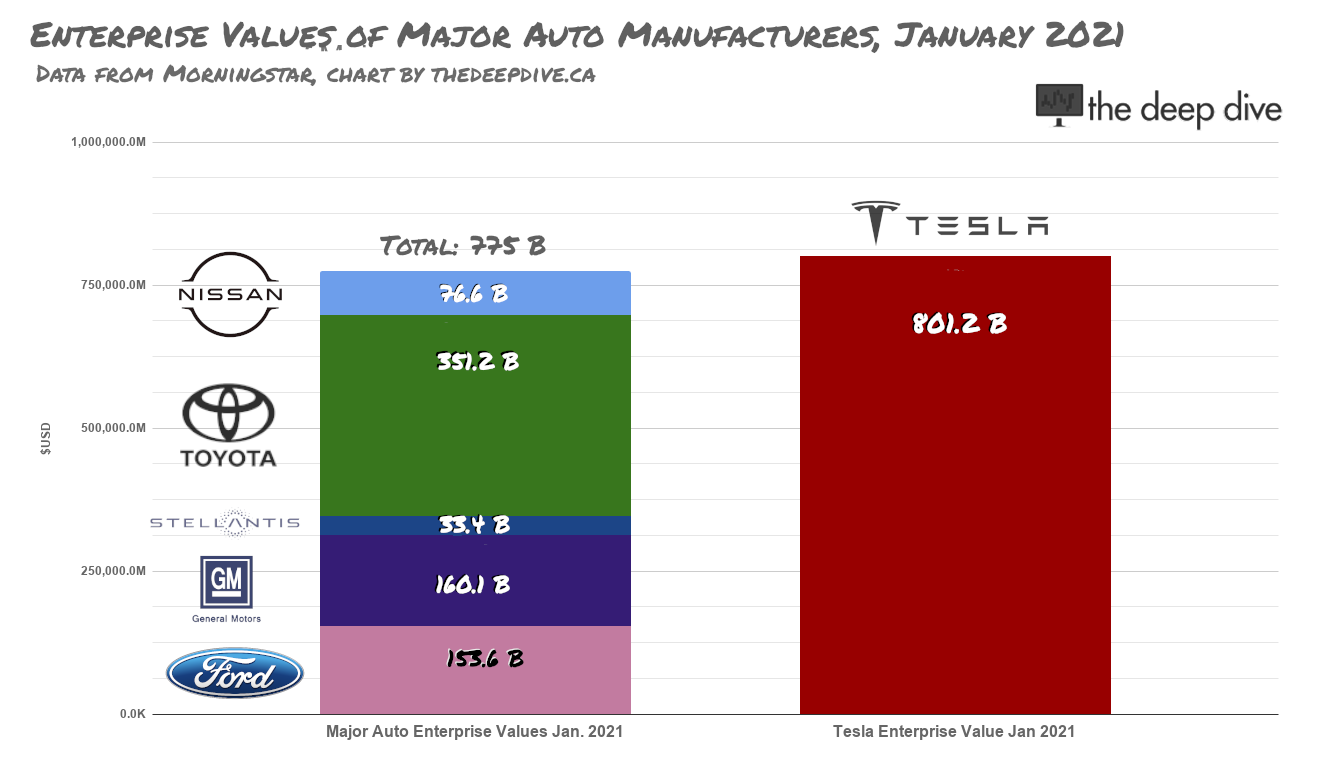

In “It’s Almost 2021, Where’s My Flying Electric Car?“, we posted that Tesla Inc. (NASDAQ: TSLA) had become the most valuable auto company in the world despite the fact that it sells the fewest cars, because the market is a forward-looking instrument. Tesla sells a comparatively negligible amount of cars compared to its peers, but is the number one seller of electric cars.

Since we published that post, TSLA has gone from being worth more than all the other car companies to being worth more than all of the other car companies put together.

It’s an electric future because the government SAYS SO.

The valuation being a product of an unprecedented promotional efficiency is notable, but Tesla being good at marketing itself isn’t actionable information. The relevance in Tesla’s dominance is the fact that the company manages its profitability by selling tax credits to its peers, who don’t sell enough electric vehicles in relation to the petroleum-fueled vehicles they sell to avoid tax obligations designed to change their product mix.

The market is telling us, in its own melodramatic way, that Tesla is the company best adapted to the auto market of the future, which is electric by mandate. The trend is for more laws that force electric adoption, not less, and the securities business is responding by giving the people what they want: a charging SPAC.

Plugs need Outlets

ChargePoint Inc. is in the late stages of a go-public deal that will see it merging with SPAC Switchback Energy (NYSE: SBE) to consummate a deal announced September 24th. The shareholders meeting to approve the merger is February 11th.

The company has done good work establishing itself in investors’ imaginations as a vital component of the coming EV infrastructure landscape. Despite low margins and no operating profit, the market has ascribed a $6.5 billion valuation to the future ChargePoint, based on the SBE stock’s $41.32 closing price on Tuesday.

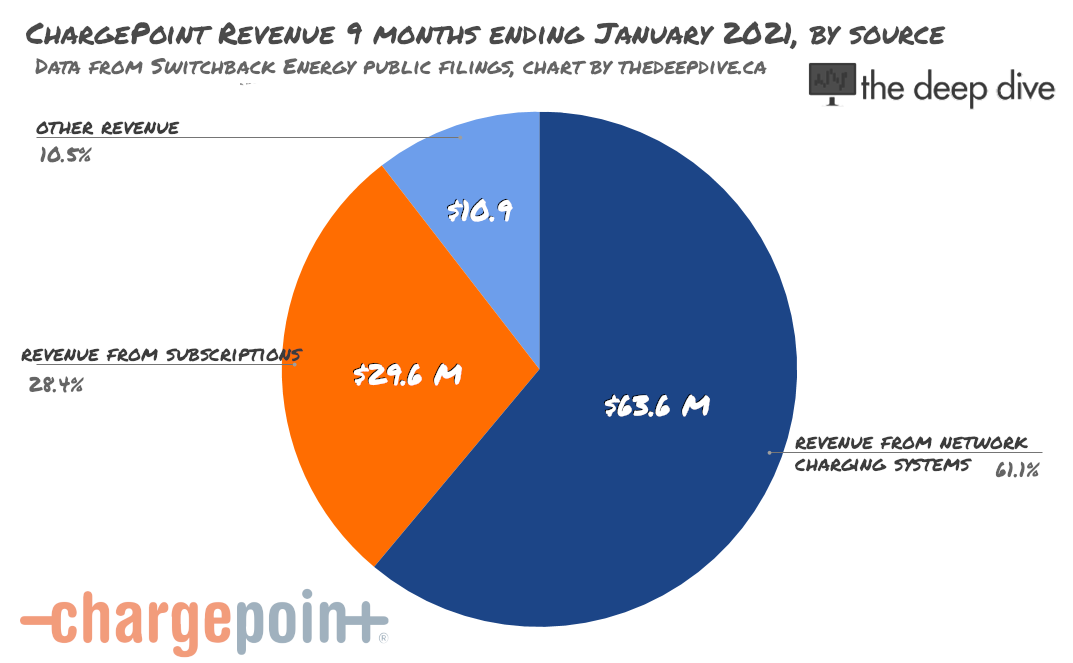

ChargePoint builds and installs EV charging systems, and makes and maintains the software that runs them, and the stations themselves. ChargePoint also owns and operates some charging stations of its own, but it’s a small portion of the total business.

Primarily, the company sells charging apparatus and infrastructure to entities interested in selling charging services to the electric vehicles of the present and future. Once the hardware is installed, ChargePoint sells its new owners two basic services by subscription: “Cloud,” a software that manages the stations by handling the cue, filling the wait lists, managing payments and all other tasks that can be handled by software, and “Assure,” a service that handles the physical maintenance of the stations and the hardware that makes them up. These services are often bundled as “CPaaS.”

The service-based model allows the package to be white-labeled by any entity that wishes to own its own means of charging its fleet, sell electricity to drivers at a markup, draw them in to walk through a retail space, or a combination of those things. ChargePoint’s current subscribers include 7-11 stores, LinkedIn, and The City of Vancouver.

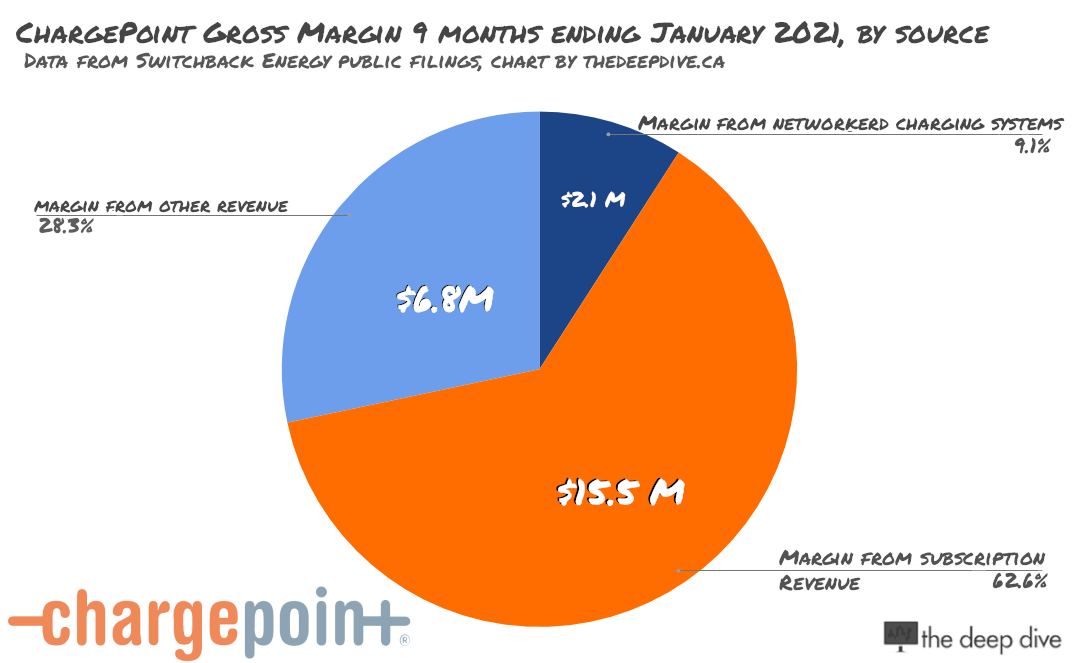

The subscription service is the second largest grossing vertical, produces the most margin, and is forecast to undergo the highest growth.

A decline in revenue in 2020 was explained as COVID-19 related, and ChargePoint is forecasting a continued decline in its revenue for the duration of the pandemic, presumably because of fewer vehicles on the roads, fewer miles driven, etc. Incredibly, it doesn’t appear to have slowed investor interest.

Near term recessions in revenue and language about “gross margin variability,” aren’t generally what the market wants to hear out of growth stories, but this play has created tunnel vision for the total addressable market in an as-yet notional electrified transportation system. The deck forecasts a six year horizon in which this company grows its revenue 15x.

Tesla’s detractors have been saying for years now that the competition would eventually come around with better cars built to higher standards. It hasn’t happened yet, but it may soon. Whether it happens and Tesla is forced to wake up from its dream, or it doesn’t and Tesla’s products grow into the space its marketing has made for them, there are going to be cars that need charging. ChargePoint is making a case that its model and market lead put it in a position to be an instrumental part of their being charged.

Information for this briefing was found via Sedar and the companies mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.