On the last episode, we learned about how a 3.4% move in interest rates caused a 20% fluctuation in the value of Silicon Valley Bank’s available-for-sale securities, and how that fluctuation led to its sudden change into The FDIC-Operated Bridge Bank Formerly Known as Silicon Valley.

We also looked at the fact that the Federal Reserve – the central bank that set the aforementioned interest rates, in an effort to tighten the money supply and combat inflation – also sets the amount of reserves that banks are required to hold, and set the US Bank reserve requirement at zero in March of 2020 in an effort to loosen the money supply, where it now remains, amid the rampant inflation that it is fighting with higher interest rates.

In part 2 we’re going to take a closer look at the one thing a bank really needs: capital.

Capital Requirements

In addition to setting reserve requirements (presently at zero), the Federal Reserve also sets CAPITAL REQUIREMENTS for American banks.

The idea is that, for an American bank to operate as a bank, it needs to have an adequate amount of capital, relative to its assets.

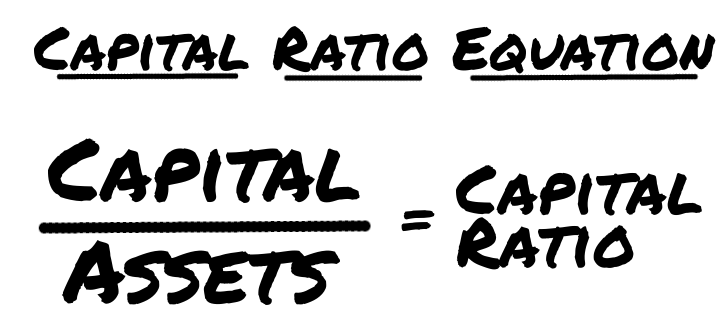

Capital requirements are a little bit different from bank to bank, depending on their institutional class, but they’re always calculated and expressed as a ratio of a bank’s capital to its risk-weighted assets, and/or its total assets. Let’s take those terms on in reverse order.

Total Assets

Just what it sounds like. All of the bank’s worldly possessions. Typically, most of a bank’s assets are loans it has made.

Risk-weighted assets

The loans are given weightings based on the risk of the borrower defaulting.

Treasury paper is money the bank has loaned to the US Government. It carries virtually no risk of default, so it has a risk weighting of 0.

The weighting on mortgage assets depends on the conditions of the mortgage.

Where the bank has first position on the title to the borrower’s house, the amount of the loan is a reasonable percentage of the appraised value of the property, the payments aren’t > 90 days past due, and the mortgage hasn’t been re-structured or modified… the banks can weight them at 50% of their value.

Other mortgage assets are weighted at 100% of their value.

Corporate debt, like the loans to VCs that made up half of Silicon Valley Bank’s balance sheet, are weighted at 100% of their outstanding value. At least.

The riskier assets are given more weight, because assets are the denominator in the capital ratio equation.

A bank with nothing but well-considered residential mortgages and treasury paper would need less capital to maintain its ratio of capital to risk-weighted assets than a bank of the same size whose loans were mostly corporate debt.

Capital

The capital in question is the capitalized equity of the banking business itself. To understand that, we first need to have a chat about accounting.

Equity

The equity in a business (not necessarily a banking business, it could be any business) is calculated by deducting its liabilities from its assets at the end of any given period.

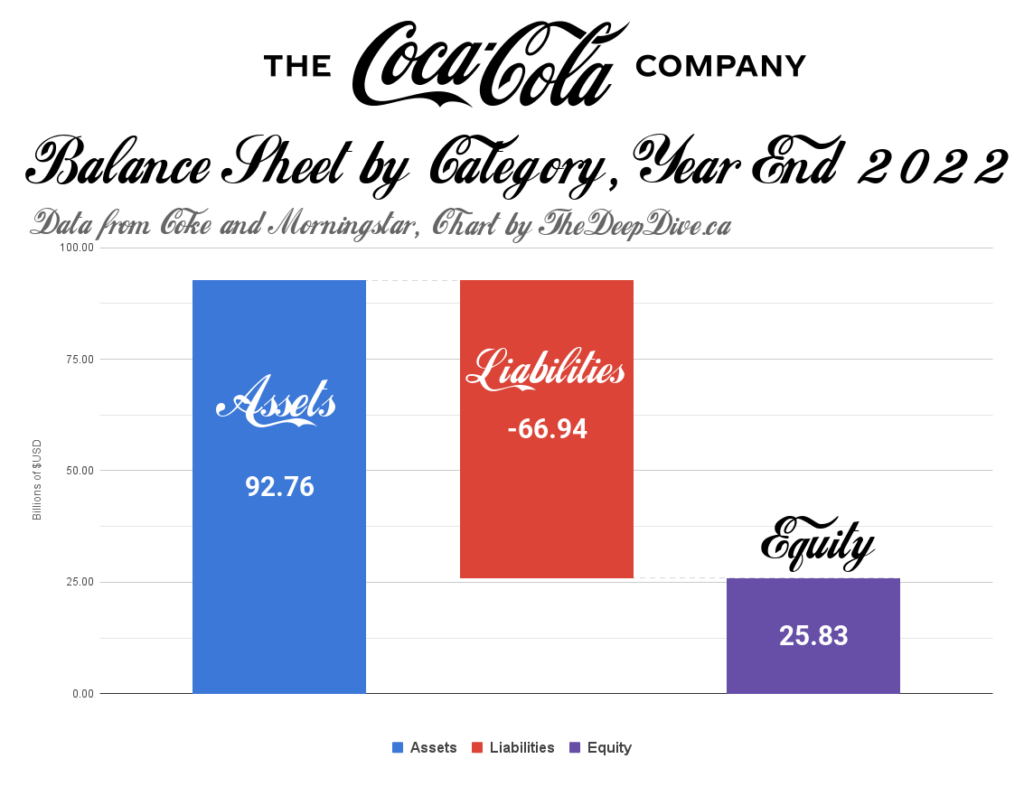

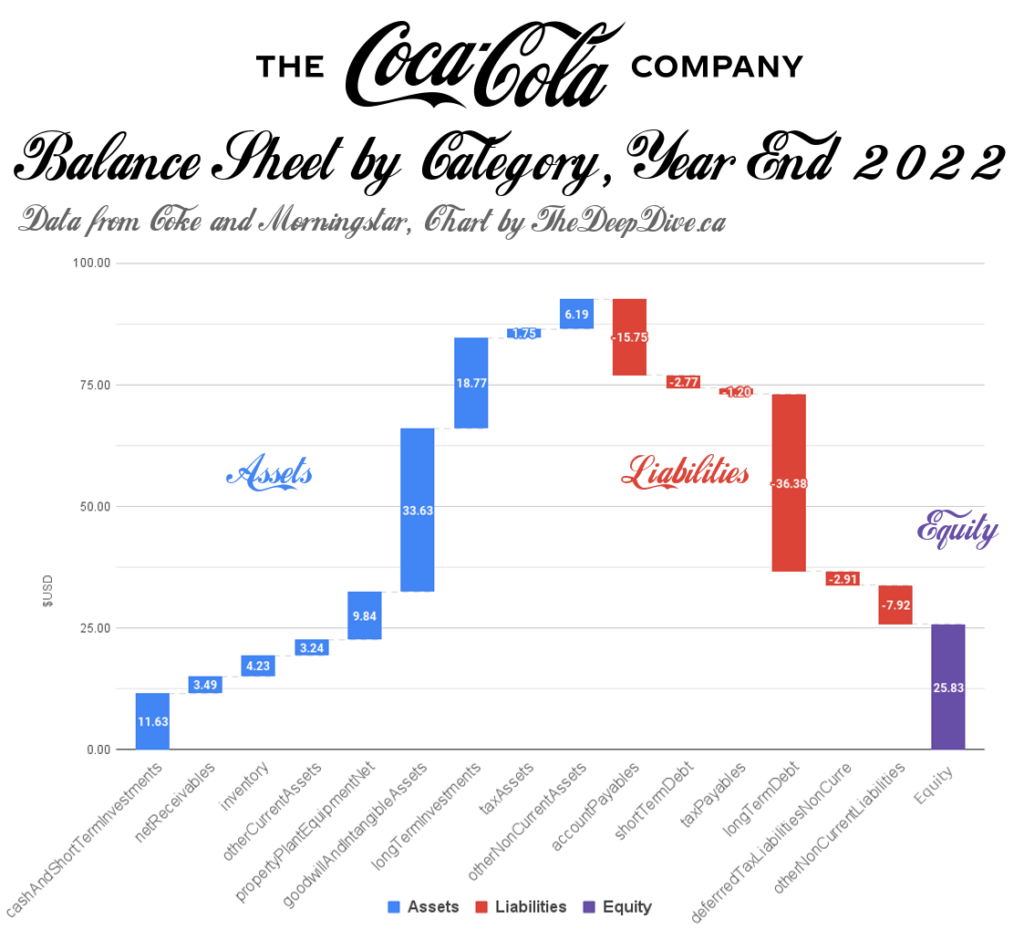

This is the assets, liability and equity of The Coca-Cola Company (NYSE: KO) at the end of 2022. Coke isn’t a bank, but this sub-tangent is about capitalized equity.

$92.7 billion in assets, less $66.9 billion in liabilities makes $25.8 billion in equity on Coke’s balance sheet at the end of 2022.

The balance sheet is the state of a business at a moment in time. We’ve broken it into categories to try and make it less abstract. The cash that it has in the bank, its inventories, its factories, its relationships with its customers, are all accounted for and totaled as the company’s assets.

The money it owes in the near term and long term, commitments it’s made to rent or lease things, or to pay into its employees’ pension plan, the taxes that it expects to have to pay, etc. are then deducted from the asset total as liabilities.

The difference left over is the equity in the business, and it is through the sale of interests in that equity that a company manages its capital, most often through the sale of capital stock.

This seems basic because it is basic. It’s important to understand how balance sheet equity is accounted for if we’re to understand it as an instrument of capital.

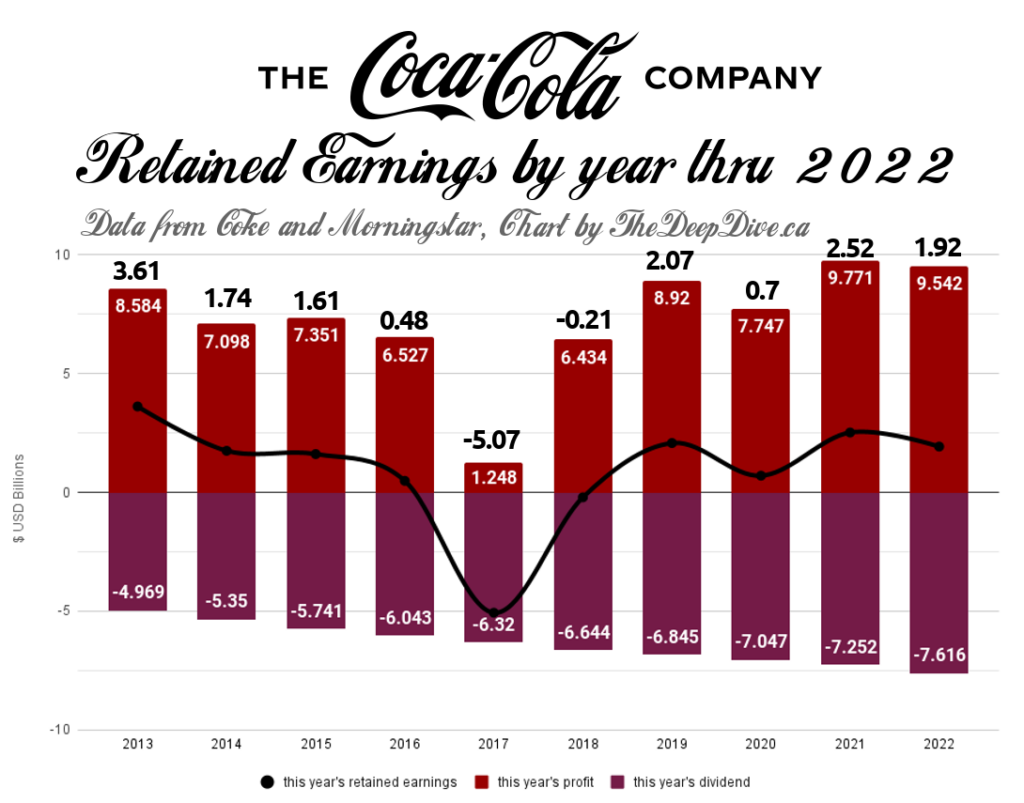

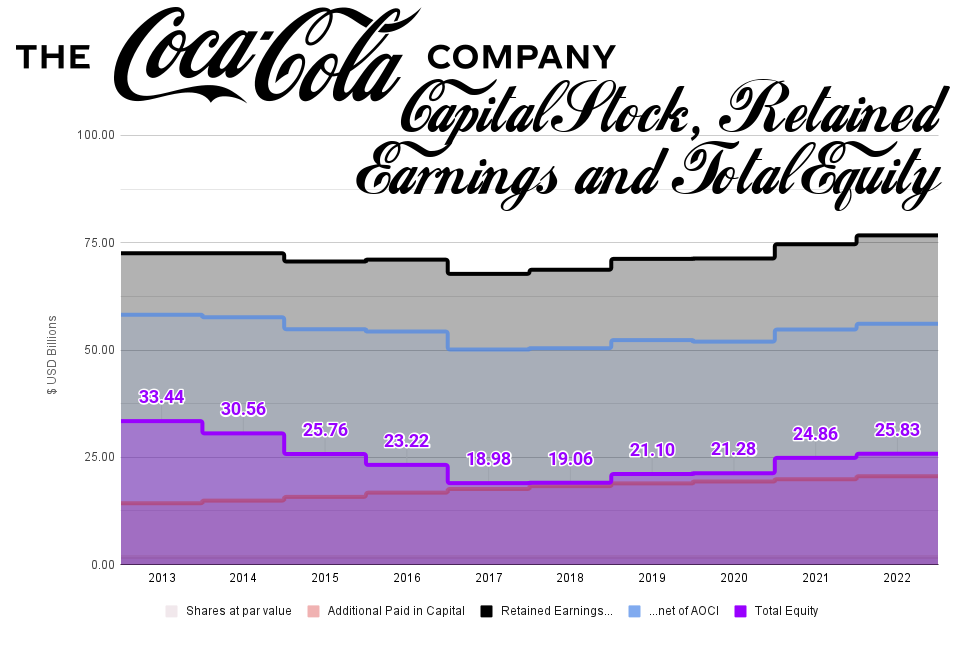

As a business makes and loses money, the annual gains and losses that make their way back into the business are kept track of in a running total called “retained earnings,” or “reinvested earnings.” This is the capital momentum that a business generates through its operations.

This chart is Coke’s earnings, dividends, and retained earnings in each of these years (non cumulative).

Retained Earnings has a sort of cousin called “Accumulated Other Comprehensive Income (Loss)”, often abbreviated “AOCI”. These are paper gains and losses that a company is carrying at the time of the statement, but may or may not have to take, case depending. The bonds SVB was carrying after the rates moved, but before it was forced to sell, are a prime example. AOCI can also be the value of real-estate that has gone up in value, or inventory that will have to be written down if it doesn’t sell.

Once an Accumulated Other Comprehensive Incomes (or Loss) is locked in, it leaves AOCI and becomes part of that year’s earnings. It is then either paid out to shareholders (dividend) or makes its way back into the business (retained earnings), but when it’s just an underperforming (or over-performing) asset hanging around on the balance sheet, the gain (or loss) isn’t yet real.

AOCI is an annual count of the gains and losses that the company knows it might have to take. It gives the reader a way to avoid surprises.

The chart above shows rolling totals of Coke’s retained earnings, AOCI, and the net total.

All the capital on this chart was generated by Coke itself. It is the momentum of the company under its own locomotion. But if everyone was happy getting places under their own power, nobody would have ever invented the El Camino.

To access capital in excess of the capital they generate, businesses issue stock from their treasuries. Capital stock is issued under all sorts of different terms. It can be preferred stock that pays a guaranteed dividend, subordinate stock that doesn’t get a vote… and it’s issued for different purposes; sometimes it’s a bonus to employees or management, or as payment for the stock of other companies as part of a merger acquisition. No matter the terms of the stock or the reason it’s issued, it all has to be accounted for on the statement of equity.

I remember when a share of Coke used to cost a quarter!

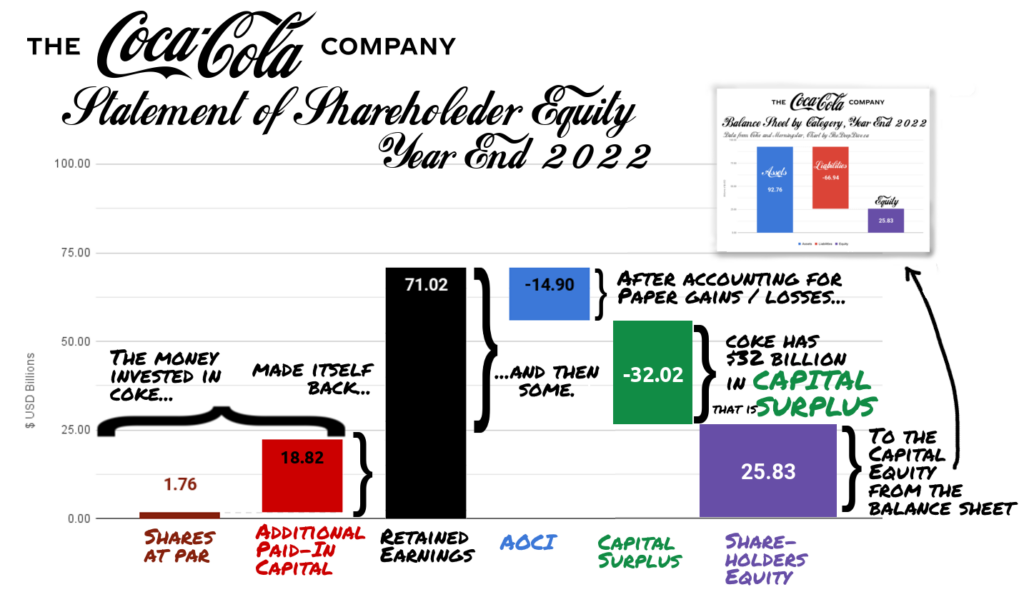

In 2022, there were 4.328 billion shares of Coke outstanding. That stock is accounted for at “par” value which, for Coke, is $0.25.

Par is often some nominal value like $0.001. Don’t get hung up on par value; it’s basically just a place to start counting.

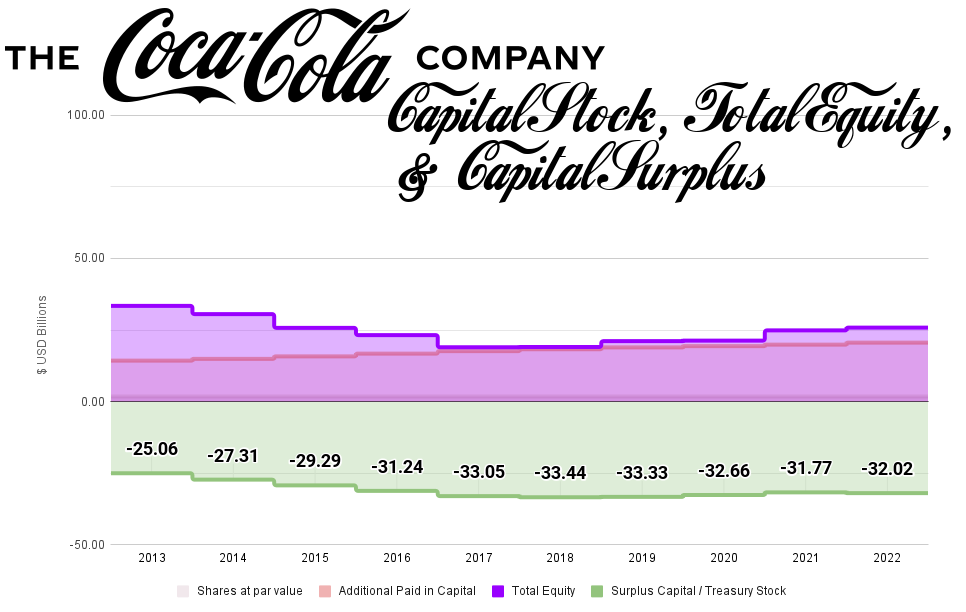

Issuing shares might only cost Coke’s treasury a quarter, but everyone else pays market rate. The money investors have contributed to Coke’s treasury in-excess of the stock’s par value is Coke’s Additional Paid-in Capital. In 2022, the cumulative total was $18.82 billion.

Next comes Retained Earnings.

Any portion of the profit that didn’t get paid out to the investors is the money that got put back into the business. It doesn’t matter if Coke used those earnings to buy new trucks, or to pay down debt, or to teach the world to sing; any profit that wasn’t distributed as dividends is retained earnings. It is plotted here net of AOCI.

Between the capital raised from investors, and the retained earnings, there’s WAY more value here than there is equity on Coke’s balance sheet.

So Coke accounts for the difference as surplus capital available in its treasury.

A cap table is sort of a geological record of what was invested in the business, and what the business has made, so far… expressed in terms of the equity owned by the shareholders.

Coke could sell more stock out of its treasury to raise capital, but that won’t get it anywhere. So Coke accounts for the difference as a surplus, and carries on making soda.

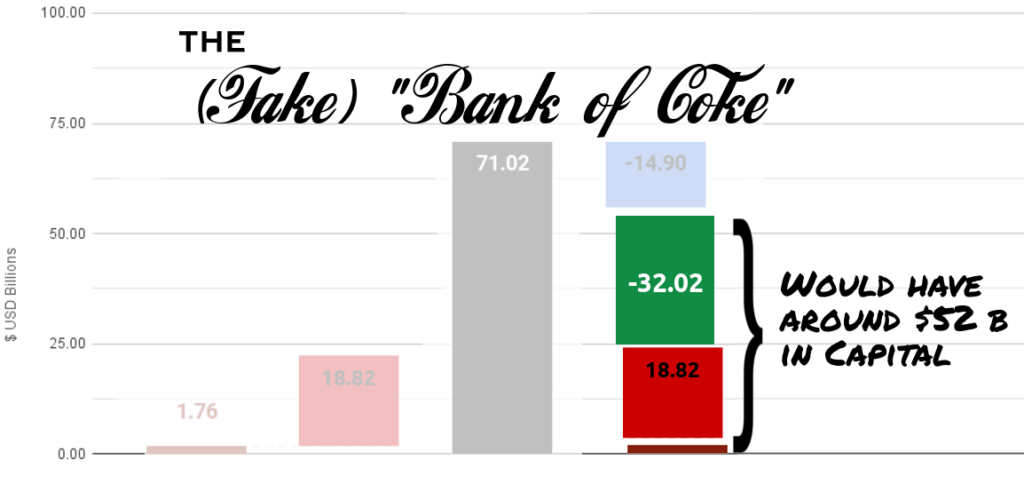

Nobody really cares about Coke’s cap table, because Coke isn’t a bank.

But if it were, it would have roughly $52 billion in capital, against which regulators would weigh its risk-weighted and total assets to come up with the Bank of Coke’s capital ratios, and assess whether or not it were well capitalized.

Another way of thinking about that is: between the money investors have put into the business, and the money the business generated itself, there is $52 billion dollars worth of confidence in Coke’s ability to not fall apart.

But the only thing liquid about this capital equity is the fact that it belongs to a soft-drink company. It hasn’t been cash since it was invested by investors or collected from 7/11. This money is now an active part of the business: capitalized equity.

(We’re going to skip capital tiers to keep this simple. The important thing to remember is that “capital,” in a banking context, is always some kind of stock that has been sold to investors under terms that somehow restrict the stockholders’ rights to receive dividends at the expense of the bank’s solvency. If the bank incurs losses, the losses have to come out of surplus & dividend before the loss affects the banking business. If you’re twisted enough to want the details on tiers, start with the FDIC Safety Manual, Section 2.1: Capital.)

The Capital Ratio

The requirements change slightly between classes of banks, and how they’re designated within those classes, but the minimum capital requirements for all banking institutions is governed by the generally applicable capital rule.

Without:

- A Common Equity Tier 1 Capital to total risk weighted assets ratio of 4.5%,

- A Tier 1 capital to total risk-weighted assets ratio of 6%,

- A Total capital to total risk-weighted assets ratio of 8%, and

- A Tier 1 capital to average total assets ratio of 4%…

…the Fed won’t let a bank be a bank anymore.

Meanwhile, in Santa Clara…

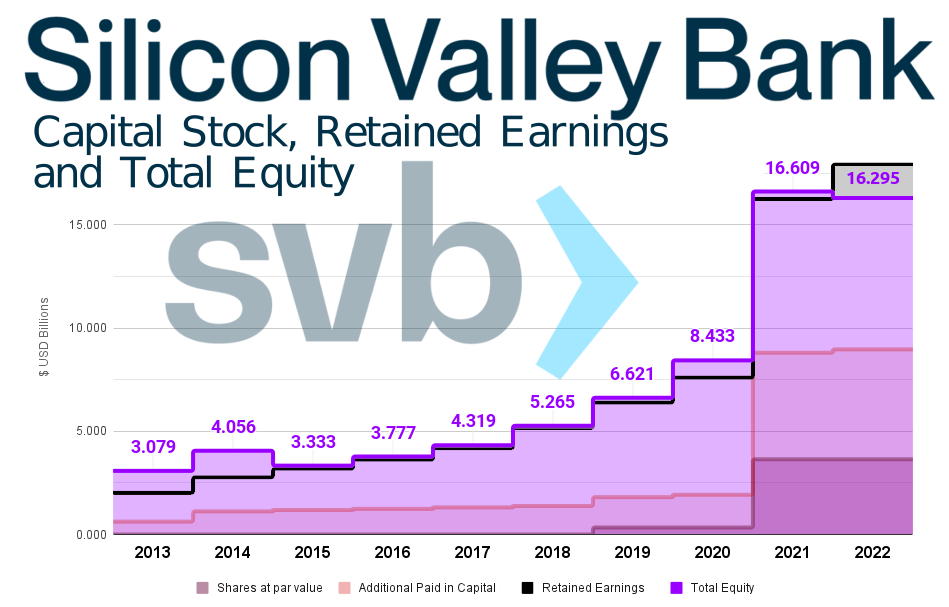

At the end of 2022, Silicon Valley Bank Financial Corporation had $211.7 billion in total assets. Deduct the $195.49 billion in liabilities, and we end up with $16.29 billion worth of equity.

SVB’s common shares have no par value. The treasury value of the preferred stock issued over the past four years adds up to $3.64 billion. That has to do with its classification as depository receipts, but never mind why, let’s keep this moving.

Silicon Valley collected another $5.3 billion in total for the direct sale of its treasury stock.

Around $40 million of that looks like it was raised from management and employees who exercised stock options over the past 3 years. This is as good a time as any to point out that SVB and Coca-Cola’s capital stocks are (or were) widely traded on secondary markets, the NASDAQ and the NYSE, respectively.

Everybody knows this. The stock market is how we’re all first cursed with an exposure to the concept of a company having “stock,” and that stock having some kind of value vis-a-vis the price it trades for on a market.

SVB’s various common and preferred equity stock issuances had a rough few days before they were halted March 7th, but the employees and executives who paid an aggregate $40 million for 1.34 million shares issued out of treasury since 2020 got a bargain.

The market value of the stock doesn’t figure in to the calculation of a bank’s capital equity for the purpose of capital ratios, so ignore it for a while longer.

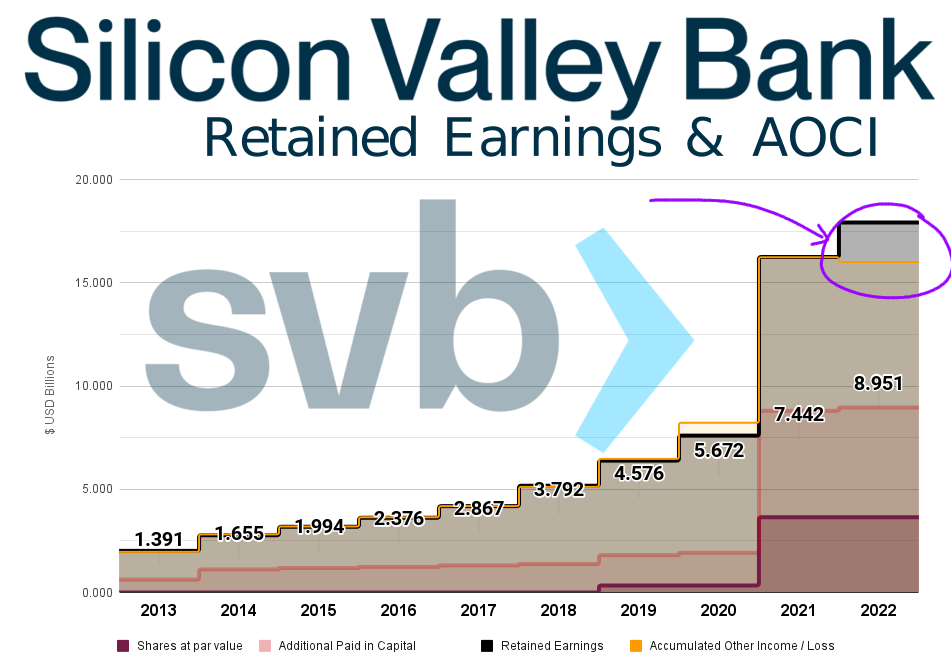

$8.951 billion in retained earnings for SVB. We’ve plotted the AOCI next to the retained earnings, but have not netted it out like we did with Coke, and there’s a good reason for that.

Institutions with less than $250 billion in assets have the option of leaving the AOCI unrealized gains and losses from the calculation of their capital for ratio-determining purposes.

Everything on this chart is a component of a bank’s Tier 1 equity, for the purpose of calculating its capital ratio. The notion is: between the capital investors have put up for their share in the enterprise, and the capital this bank has re-invested in itself, there ought to be plenty around to take care of withdrawal requests.

Silicon Valley took advantage of that AOCI exception and, when it was tallied up with $3 billion in treasury stock, $5 billion in additional paid in capital, and $8.95 billion in retained earnings, as far as the US Federal Reserve was concerned, Silicon Valley bank had $17 billion in Tier 1 equity capital at the end of 2022.

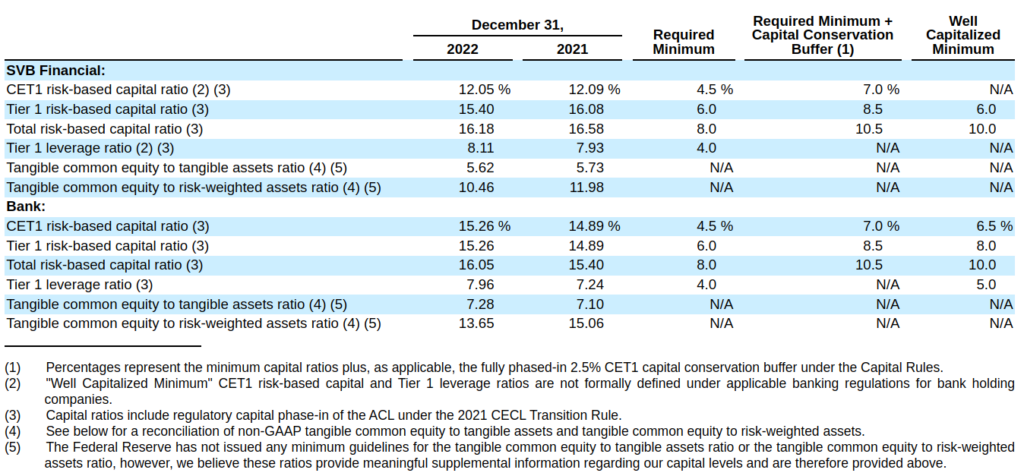

After making the required adjustments for goodwill and intangibles, the bank had between $113 billion and $111 billion in risk-weighted assets, depending how it’s counted, so the Tier 1 capital ratio was between 10.46% and 13.65%, well above the 6% that is considered well-capitalized!

..and we all know how that turned out.

If you asked any adult what it takes to get a banking charter, one of the things they’d say is that you have to post some capital. Probably in some kind of proportion to the deposits the bank was going to take… so that there’s enough around to cover withdrawals. They’d be right, semantically, but it wouldn’t mean what they think it does.

The capital does have to be put up, or generated by the banking business itself, but it doesn’t really have to be kept anywhere in any specific kind of instrument or specie. It just needs to be capital that someone has risked on the fortunes of the banking business. Its only proportional relationship to the deposits the bank takes is indirect: the rules govern how much capital the bank has to have in relation to its assets – the money it’s lent out – and it can generally lend money at the rate it takes deposits.

Silicon Valley Bank found out the hard way.

Selling the bonds was easy. It generated $21 billion and likely got them close to covering the cash demands from their depositors. But…

…remember that gap?

When SVB sold those bonds, the on-paper AOCI loss that it had opted to exclude from the calculation of its capital ratio became an actual loss that it could NOT exclude. The realized loss lowers the retained earnings, reduces the total capital, and comes right off of the numerator used to calculate the capital ratios.

Silicon Valley had available credit at the Federal Reserve, but the person who picked up the phone at the Fed likely informed an SVB executive (who was trying not to act panicked) that the previously arranged credit was only available to banks who meet the required capital ratios and, in light of recent developments, SVB’s capital would have to be topped up to meet the ratio.

SVB is no longer a bank because, when it went to the market to raise capital with its equity, there weren’t any takers. On the topic of SVB’s equity capital, the capital markets had spoken: there was not $2 billion worth of available confidence in the prospect that this bank, with this loan portfolio, wasn’t going to fall apart.

The market value of the bank’s outstanding capital equity was $24.5 billion as recently as the end of 2022… But markets are fickle. And the fact that the only way to know when that market has dried up is to try and do a stock issuing might be considered a fatal flaw in the practice of determining a bank’s fitness through its capital ratio.

If you asked a seven year old what it takes to own a bank, they might say something like: “You have to be really rich. Probably as rich as whoever owns Coke,” and they’d have a better handle on it than the adult.

BIG thanks to everyone who made it the whole way through!

Stay tuned for Part 3, where we’re going to use what we learned in Parts 1 and 2 to take a look at the capital situations of the stars and planets in the US banking galaxy, and look for potential implosions.

{kind=link}