There is great narrative power in being able to make complicated ideas simple and understandable. Any good, effective pitch makes the audience feel like they understand it so well, they could have come up with it themselves. Cathie Wood’s ARK Invest has it down to a science. She’s created a burgeoning solar system of ETFs under the ARK banner that all take advantage of ARK’s deep understanding of how to generate excitement, make them believe, and make the benefits of that belief overflow on to the portfolio companies.

ARK Invest deals mostly in managed ETFs; a relatively new type of investment product around which the firm has built an empire. Unlike passive ETFs, which adjust their components automatically according to pre-set parameters and are designed to offer exposure to specific indexes or sectors for low-fees, actively-managed ETFs have a product mix built and managed by portfolio manager, like a mutual fund, but are tradeable, exchange-listed products.

Unlike mutual funds, which have a mandate to beat the index of whichever sector the fund is offering exposure to, ARK’s funds are not benchmarked. The ARK solar system revolves around the ARK Innovation ETF (NYSEAMERICAN: ARKK), which professes to be a product made up of the companies who are developing the tech that will disrupt today’s most valuable industries and eat their lunch. Since it’s built for exposure to business innovation (as defined by ARK itself), it’s kind of its own benchmark.

Innovating the buy side with a sales component.

The fund was born in 2014, but really got moving in 2016, when it was pitched at an investing public well-primed to hear about it. Google and Facebook had just got done making the print advertising and newspaper business obsolete, and Amazon was in the process of putting every department store in the country out of business. A diversified, managed fund product meant to harness the forces of tech disruption sold as well to futurist dreamers as it did to investors who didn’t want to take the chance that they might miss out or get caught on the wrong side of an industrial shift, financially.

It’s a dreamer class of investors, susceptible to the notion that they can get rich by staying ahead of the innovation curve. An intellectually curious bunch who are eager to stoke their own confirmation bias.

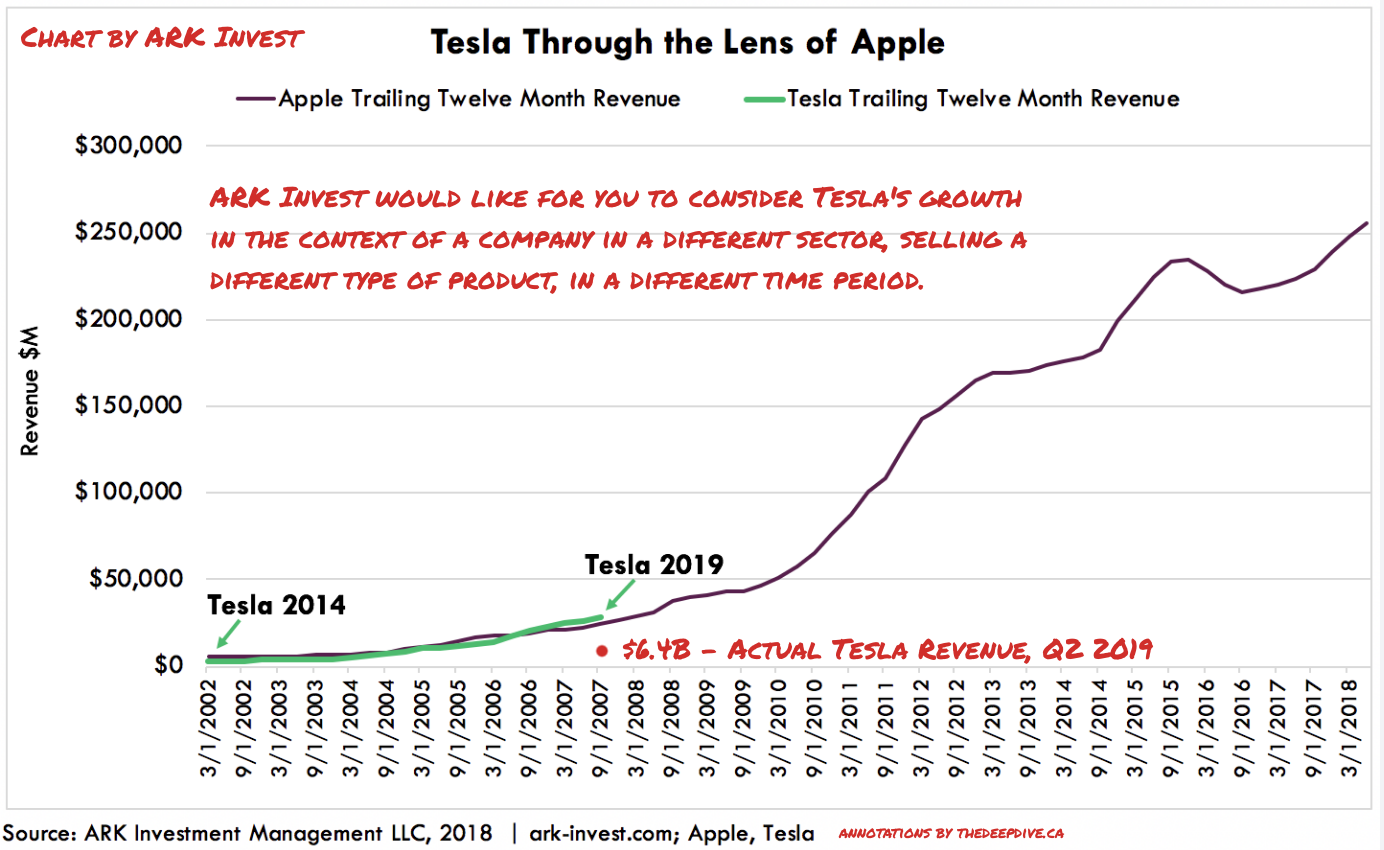

The ARK Innovation Fund went basically sideways through 2015 and 2016 before embarking in 2017 on the first leg of an epic tear that put it on the map. The run began right around the time ARK made its first investment in Tesla, but might have had more to do with some innovation at ARK itself.

ARK has taken a buy-side configuration – one that uses its internal talent and brainpower to build and execute strategies with open-market positions in liquid securities – and used it to create sell-side products. The approach tapped an entire generation of high earners with no time for the black box style of managed funds, or their fees, and didn’t have much patience for research papers written mostly as collateral to defend a trade. ARK’s research doesn’t waste much ink on defense.

The Walt Disney of finance: the only limit is your own imagination

To simplify stories, you have to take parts out, and ARK learned early on that the best part to skip is the part about how it might not work. Ark’s research staff maintains a very active publishing schedule. Blog posts, podcasts and white papers fly at pace, explaining key tenets of their investment thesis, in the simplest terms possible, without ever going on for too long, often with a portfolio company as a feature example.

You’ll never catch the researchers explaining the technical merits of an investment, or a company’s cap structure or its ability to raise money. It’s always an enormous, game-changing vision for a sector that the fund is bringing its holders exposure to through its ownership of a hyper-visionary company that just gets it, and is probably Tesla.

ARK did some poignant modeling of the potential demand that a fleet of autonomous taxis could have on the Arizona grid in November of 2018. They did so by framing the fantastic notion of a self-driving, self-charging autonomous transportation network as a foregone conclusion, doing seemingly prudent, grown-up analysis of its potential effect on the vital, very real and present constant that is the city grid.

The posts all have easy to follow graphics of pseudo-analysis built around specious associations and baseless connections. The blog frequently cites itself as a source, and can’t be taken seriously by any equities analyst who takes themselves seriously… but it doesn’t have to be. The target demographic is light years ahead of those stuffed shirt analyst types, who lack vision, and are no fun besides.

ARK’s research department serves as a content marketing platform for its ETFs, and the companies that populate them. As promotional investor content, it’s the best in the business. The foundational backdrop of name-brand letterhead certainly helps, because its founder has been relentless in her promotion of that brand. Telegenic, engaging and enthusiastic, Cathie Wood has never met a camera she didn’t like.

She can frequently be found on cable business shows making outlandish projections about the Tesla of the future (that they will take transportation over with autonomous taxis), and the Tesla of the present, (that its brand-new, untested chips put them years ahead of the competition on autonomous driving) with total, un-wavering confidence.

With ARK’s wagon hitched solidly to Tesla’s star, they kept new, fresh, hyper-consumable investor content coming and used the media to leverage its distribution and jam the channels. It never engages with Tesla’s numerous, very loud critics and only very rarely acknowledges them because, as any great promoter can confirm, that’s a waste of time. It can only serve to divert the story somewhere that doesn’t serve a purpose, or bog it down. Far better to stay on message, produce more research, and drown them out.

ARK’s first TESLA push having rounded up the starry-eyed dreamers, the stock was in a magnificent position to pick up a more risk adverse class of growth investors when it became apparent the company was able to turn a profit on tax credits sold to other auto manufacturers. The mainstream buy-in gave the dedicated base a reason to increase its position. Between that and the most violent short squeeze since Volkswagen, Tesla went into full melt-up, taking ARKK with it.

In the ultimate twist of the knife in Tesla bears, Cathie Wood is currently on a Tesla victory lap of sorts. Perhaps, the stock having carried her fund to where it is, she’s entitled. But the primary driver behind Tesla’s revenue was never contemplated by ARK or discussed in its research.

Tesla’ financial success is being objectively sustained by its sale of tax credits to other auto makers, effectively arbitraging a government mandate that legacy automakers ship emission free or emission-reduced cars. But the growth not coming from where Wood expected it might hardly matters. A win is a win. And the beauty of potential is that it’s unlimited. Tesla can still build a robo-taxi fleet that takes us all to Mars, and ARK can keep selling the value of that potential today.

Why wouldn’t it? Success is contagious and there’s plenty of “potential” in the portfolio for the success to rub off on. ARK separates its investments not into traditional sectors, but into areas of innovation. Robotics, genomics… all full of companies striving after impossible dreams. The idea that they might get some help from the government on their way there technically isn’t out of the question, but that’ll never sell. The prospect of gene editing becoming commercial is way more fun to talk about.

Information for this briefing was found via Edgar and the companies mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.

6 Responses

“Tesla’ financial success is being objectively sustained by its sale of tax credits to other auto makers”

Can you substantiate that? This feels like such a narrow view of the stock.

Thanks for reading, Serge.

Tesla had booked $140M in revenue from the sale of regulatory tax credits in the nine months ending Sep. 2020 at (obviously) no cost. That’s about 25% of its operating profit. In previous periods, it’s been the difference between a profit and a loss.

Thanks. It reminds me of when I was a kid, I had just finished reading a book about Spitfires vs Messerschmitts, and walked to my dad all excited parroting a line in the book that said that had plane X had an extra range of Y, the war would have gone differently. My dad, ex military pilot, kind of looked at me as if I were an idiot, stopped short of calling me one, and said something along the lines of “son, check your perspective / take a step back, shit’s more complicated than that”.

That’s how I feel about your analysis.

Also, was I traumatized by my dad? 😀

That said, thank you for replying to my Q!

I would suggest, Serge, that your statement to your dad referenced a much wider and more holistic success – the winning of a whole war – than my statement about Tesla, which referenced the financial success of the business. There is nothing complicated or nuanced about a bottom line: either a company made money or it did not. Without the money received from the sale of tax credits, Tesla does not make money.

Naturally, Tesla shareholders (including Wood and Musk) have done very well with respect to their investments in the company’s public equity. But the money made in that instance was not made by the company, which runs an automobile business, it was made in the stock market, by way of securities investment.

Thanks again for reading.

Braden

Thanks for reading, Billy.

I really enjoyed reading this article. is this your personal?