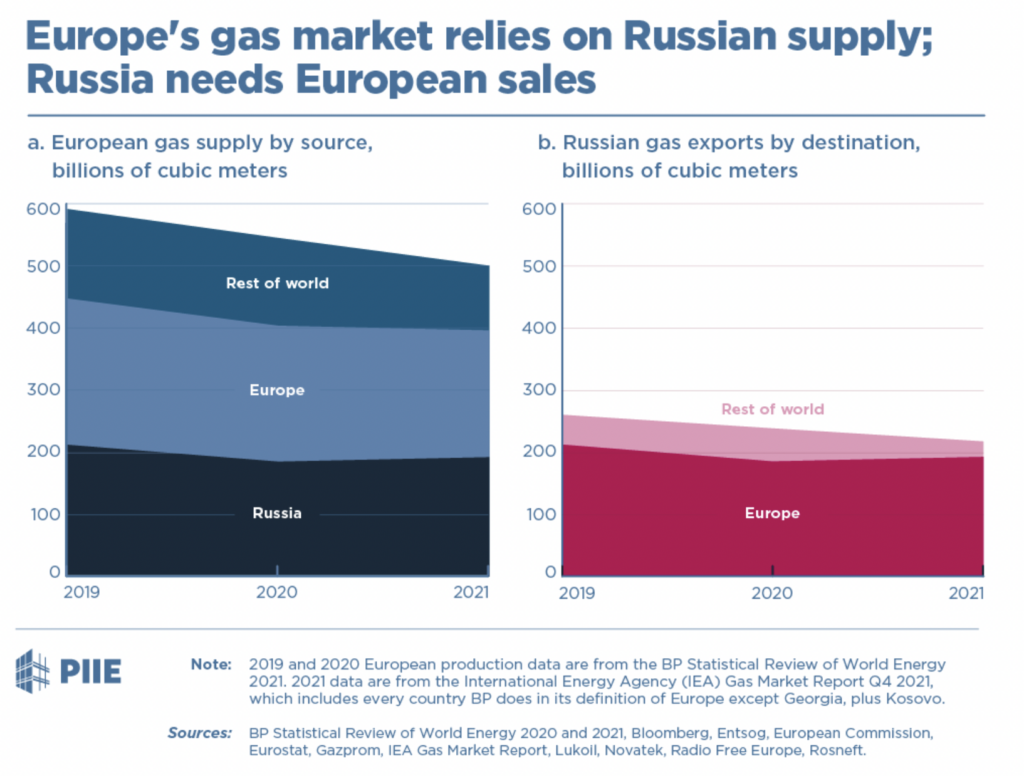

As 100,000 Russian troops continue to mass on Ukraine’s border, and news reports say many Ukraine citizens are resigned to the commencement of what would be Europe’s biggest land war in 75+ years, a critical issue for investors is Europe’s high-priced and what appears to be fragile energy markets. Specifically, Russia supplies a remarkable 40% of Europe’s natural gas; for Germany, that figure is more than 50%.

The key question is: if a war were to begin, how would Europe’s North American Treaty Organization (NATO) members react to the incursion?

To be clear, Ukraine, which has a democratic political system characterized by free elections, wants to join the organization, but it has not (yet) been admitted as a member. Still, in June 2020 it joined something called NATO’s enhanced opportunity partner interoperability program. If, say, France or other countries on the continent were to react to support Ukraine with money and military equipment (but almost certainly not with troops), Russia could, as a reprisal, simply turn off the gas flow in the middle of winter.

Cognizant of this risk, CNN and other news agencies report that the U.S. is trying to pressure liquefied natural gas (LNG) suppliers, including the key LNG exporting nation of Qatar, to commit to delivering more product to Europe as a precaution. While such supply would not fully offset the “switched-off” Russian gas, the incremental energy supply could theoretically provide some degree of buffer.

Clearly, an initiation of war by Russia could have other consequences, including boosting general inflationary fears and buffeting worldwide equity markets at least temporarily, but investors may want to consider owning shares in an LNG supplier as a partial “Russian” hedge.

A leading candidate for this role could be Cheniere Energy, Inc. (NYSE: LNG), a full-service LNG provider headquartered in Houston, Texas. Cheniere provides LNG liquefaction, transportation, and delivery services for clients located throughout Europe and Asia. Indeed, Bloomberg reports that company exported a daily record of 5.1 billion cubic feet of LNG from its Sabine Pass export terminal on both January 20 and January 21, 2022, reflecting a push to send cargoes to Europe.

Cheniere‘s liquefaction facilities are about 90% contracted over the next 15+ years. It has about US$6 billion of revenue fixed via annual fixed-fee or take-or-pay style agreements. Cheniere has delivered LNG cargoes to clients in 35 countries.

| (in millions of U.S. dollars, except for shares outstanding) | 3Q 2021 | 2Q 2021 | 1Q 2021 | 4Q 2020 | 3Q 2020 |

| Adjusted Operating Income | $765 | $146 | $1,064 | $276 | $72 |

| Adjusted EBITDA | $1,053 | $1,023 | $1,452 | $1,052 | $477 |

| Cash – Period End | $2,023 | $1,806 | $1,667 | $1,628 | $2,091 |

| Debt – Period End | $32,633 | $32,030 | $31,806 | $31,658 | $31,978 |

| Shares Outstanding (Millions) | 275.1 | 275.0 | 274.9 | 273.1 | 252.2 |

While Cheniere seems to be a natural choice for investors who want an LNG supplier as a hedge, an issue to consider is its reasonably full valuation. Cheniere trades at an enterprise value-to-estimated 2022 EBITDA ratio of nearly 10x. We do note, however, that the company raised its own EBITDA projection a number of times throughout 2021.

At this point, a Russian invasion of Ukraine has to be discounted to at least some degree by the stock market. Nevertheless, when and if shots are fired, short-term traders seem likely to allocate significant dollars toward companies which may benefit from the conflict. Investors may want to be positioned in such a name, Cheniere, before the conflict begins.

Cheniere Energy, Inc. last traded at US$113.00 on the NYSE.

Information for this briefing was found via Edgar and the companies mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.