Controversial medical devices company Penumbra (NYSE: PEN) recalled a defective catheter last week in the latest chapter of a prolonged fight with a short selling syndicate who have practically gone through the company’s garbage, and come up with more than enough to cause concern. The shorts have promised more to come, making it likely that this will remain the most entertaining show in the market for a while longer, so it’s as good a time as any to examine Penumbra as a business.

A series of tubes

Penumbra makes systems used to perform neuro and vasuclar thrombectomies. Put simply, when a clot is obstructing blood flow, a doctor performs a thrombectomy by sticking a long, thin tube called a catheter up through the circulatory system to either remove the clot or break it apart. Penumbra manufactures and sells the various sophisticated catheters and associated equipment that doctors use to perform those thrombectomies. The Penumbra product division that is used to treat clots in the vessels that service the brain is called Neuro, and the division of products used to thrombectomize everything else is called Vascular.

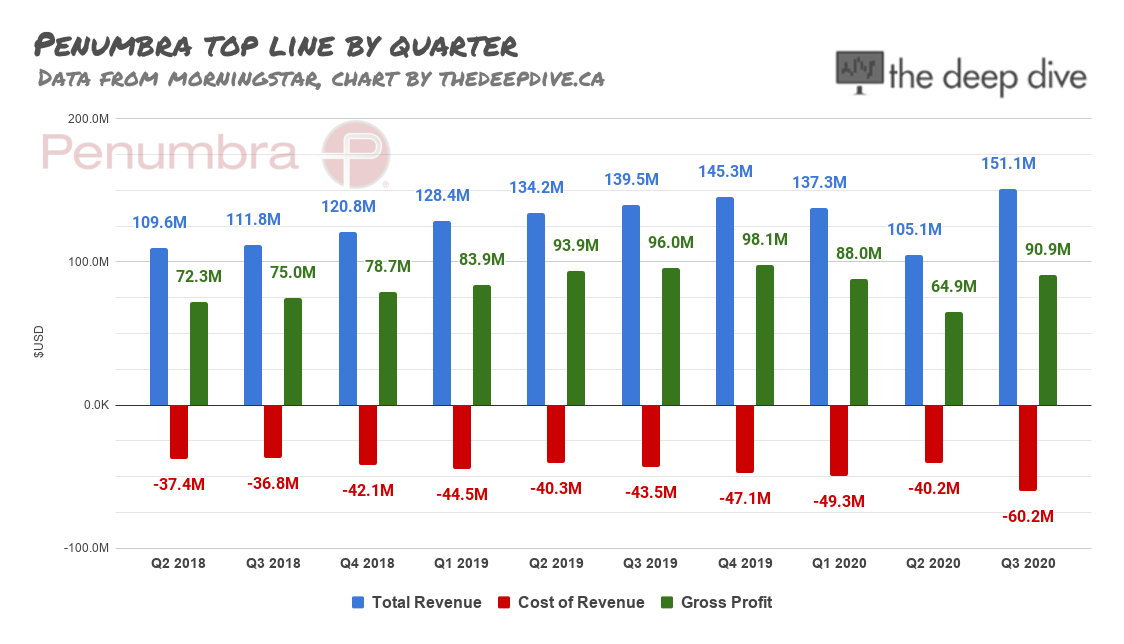

Top-Line

We start, as usual, with the top-line, which looks good and steady, but ran into a bit of a hiccup in Q2, 2020 (the period ending June 30, 2020), the same period the shorts allege problems with the now recalled Jet 7 with Xtra Flex catheter started showing up. The company attributes the sales dip, which included 27.8% less sales of neuro products, and 12% less sales of vascular products compared to Q2 2019, to the effects of the COVID-19 pandemic, but doesn’t say how the pandemic led to fewer emergency stroke procedures. Revenue recovered in Q3, but so did costs, specifically production costs, which included a $2.2 million inventory write down.

The Q3 quarterlies include language about reimbursement charges, decreased neuro sales, and a paused launch of a new stroke product in Japan, but do not mention the fatalities that presumably caused them.

Bottom Line

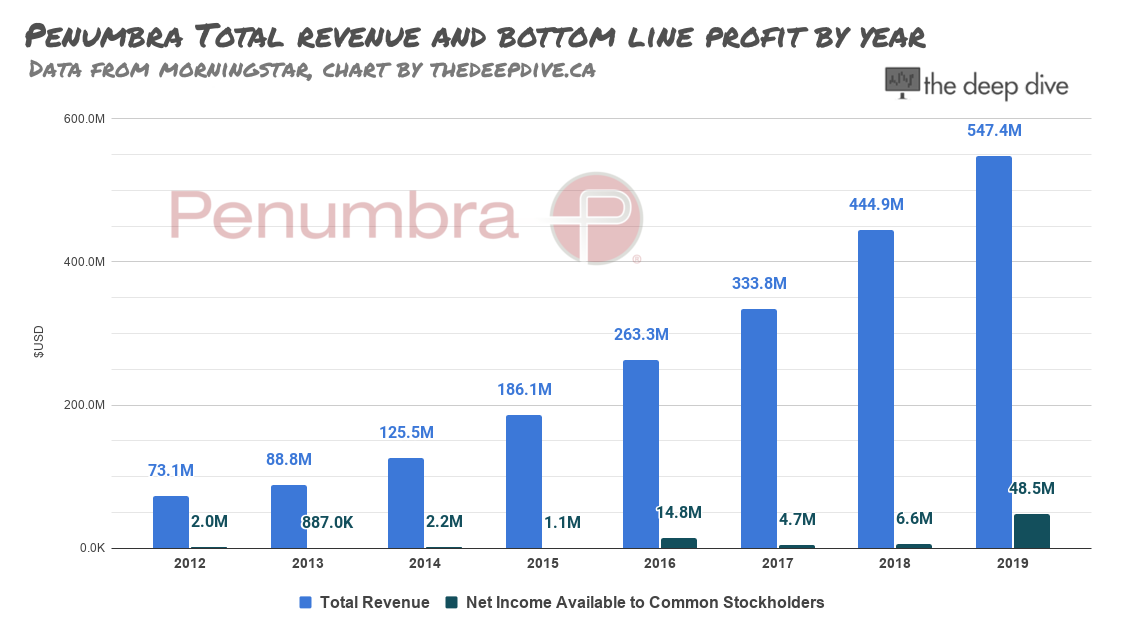

On an annual basis, Penumbra has a history of producing tremendous revenue growth while still generating a bottom-line profit. It had a banner 2019, printing $547.4 million in sales and $48.5 million in profit

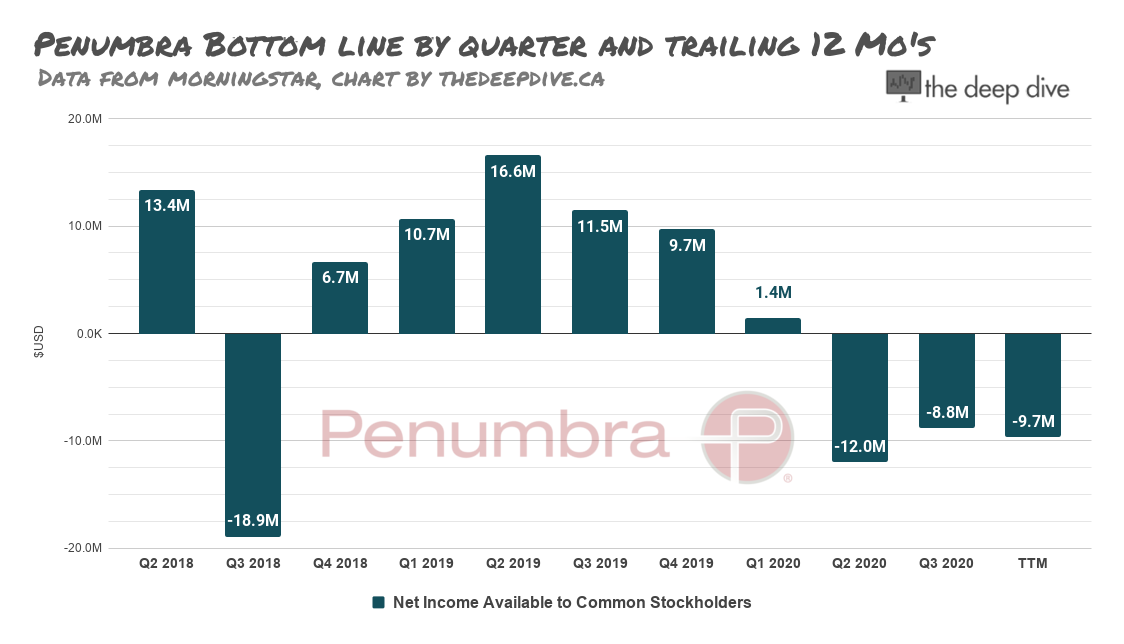

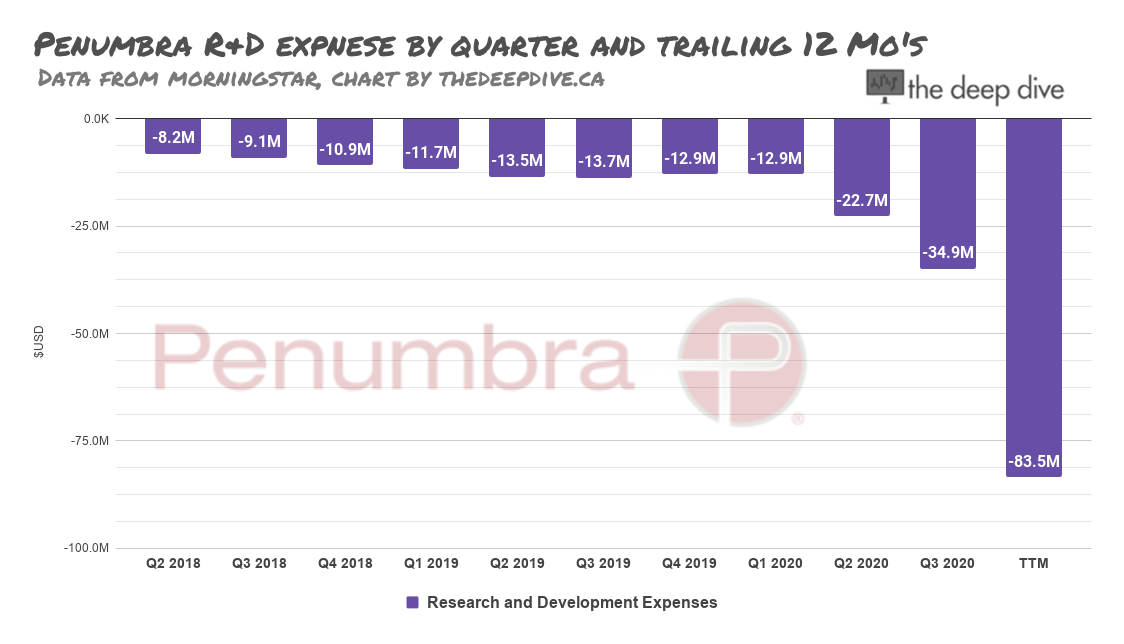

But the bottom line has been eratic in 2020, falling into the red right around the time the problems started to appear in Japan. It’s usually the SG&A line that swells when a company finds itself in the red, but in Penumbra’s case it’s R&D.

The company has already spent more through three quarters of 2020 than it had in any single year prior, thanks to ramp ups in Q2 and Q3. The expenditures track with CEO Adam Elsesser’s assertion on the December 14th recall call that the company is all set to deliver new products that will change the entire emergency stroke-care paradigm. (Elsesser didn’t say anything on the call about how thoroughly the new products would be tested.)

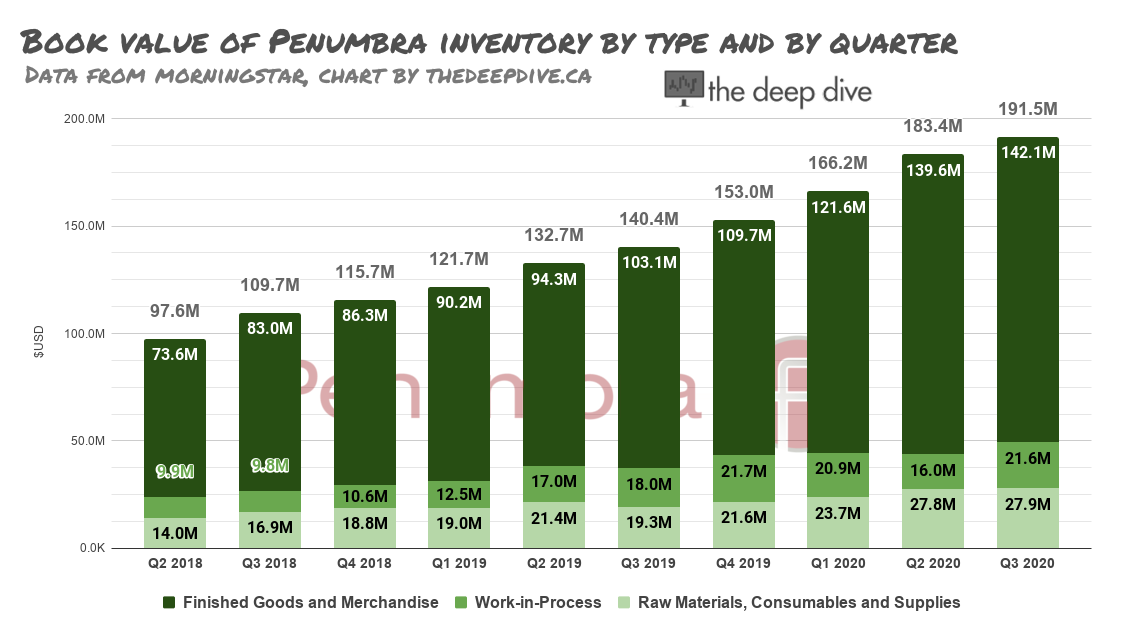

Inventory

The R&D ramp up is an interesting development in the context of Penumbra’s inventory profile, which was at an all-time high in terms of book value in Q3, and consisted of 74% finished goods. A warehouse full of inventory doesn’t scan like an advantage for a company aggressively developing new products meant to “change the paradigm” of the field in which they’re used, it scans like dead weight. Regular readers will know that the company forecast $20 million in product returns related to the recall, and wouldn’t speculate about the effect on inventory.

Balance Sheet

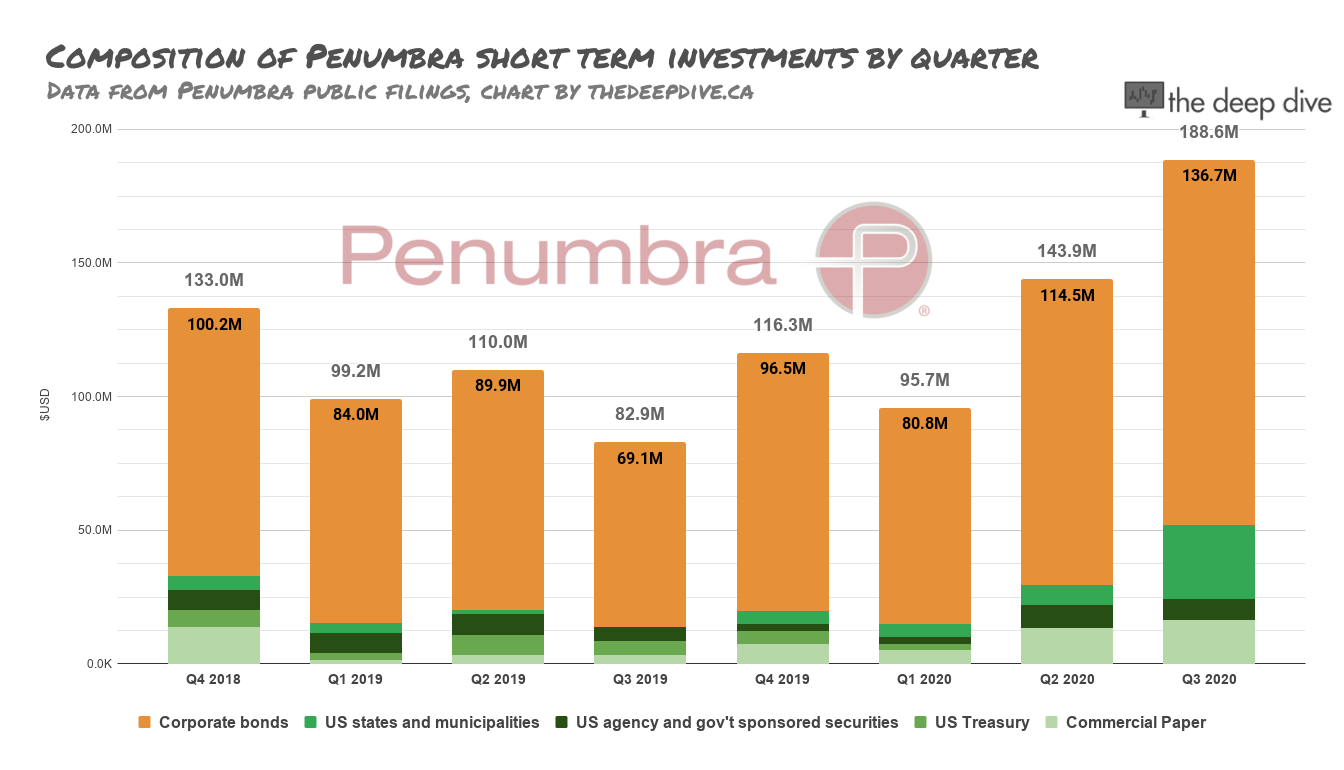

Here’s something you don’t see every day: Penumbra has no debt. The lack of leverage might be central to the reasons this company hasn’t fallen apart in the face of a vicious short attack whose doom prophecy is playing out like a nightmare come true. There’s enough a cash balance to carry an extended period of operating losses, but it could dry up quickly if the revenue wanes, and some of it may have to get set aside to defend or settle class actions or pay fines.

The composition of the cash is interesting, because the bulk of it is being kept in high-grade corporate debt instruments. Penumbra’s statements don’t say what the debt is composed of, only that it’s managed by an outside firm, and does not over expose to any single entity apart from the US government. Our calculations have Penumbra’s portfolio of bonds generating 1.1% of its total value in interest over the 12 months ending September 30, 2020.

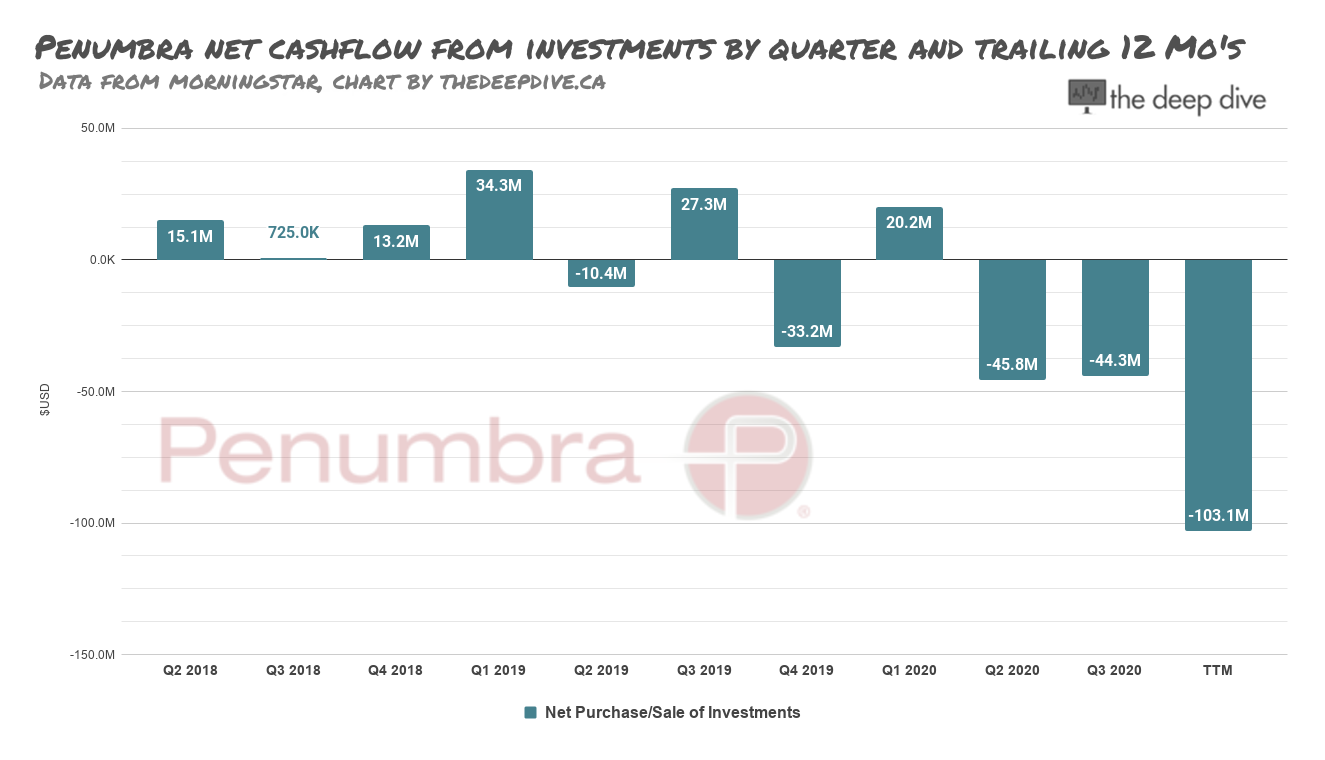

The final yield might turn out lower. Penumbra has generated around -$45 million in negative cash-flow from its investment portfolio in each of the past two quarters, and is down $103 million over the trailing 12 months.

… but as Deep Dive readers surely know: it isn’t technically a loss until the positions are all closed and it hits the P&L.

Conclusion

This is a business up against a perilous headwind, running right at it with full conviction. Its remarkable confidence likely comes, at least in part, from a deep war chest and a strong balance sheet. We’re going to take a look at what that might mean for its equity soon, so stay tuned.

Information for this briefing was found via Sedar and the companies mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.