Equity market jitters are palpable in the first week of March as the major indexes continued to falter, and the upward move in bond yields continues. The yield on the US 10 year Treasury note rose again to finish at 1.54% Thursday.

Among the largest beatings is the one being taken by the tech-heavy NASDAQ, which broke below 1,300 on the close Wednesday. The exchange had benefited from the risk-on, low-rate environment, doubling over the course of the now 12 month long pandemic, but is presently below its 200 day moving average for the first time in 2021, trying to decide which way it’s going to break. The weakness indicates that investors are wondering, at the moment, how much longer the market will continue to put a premium on growth.

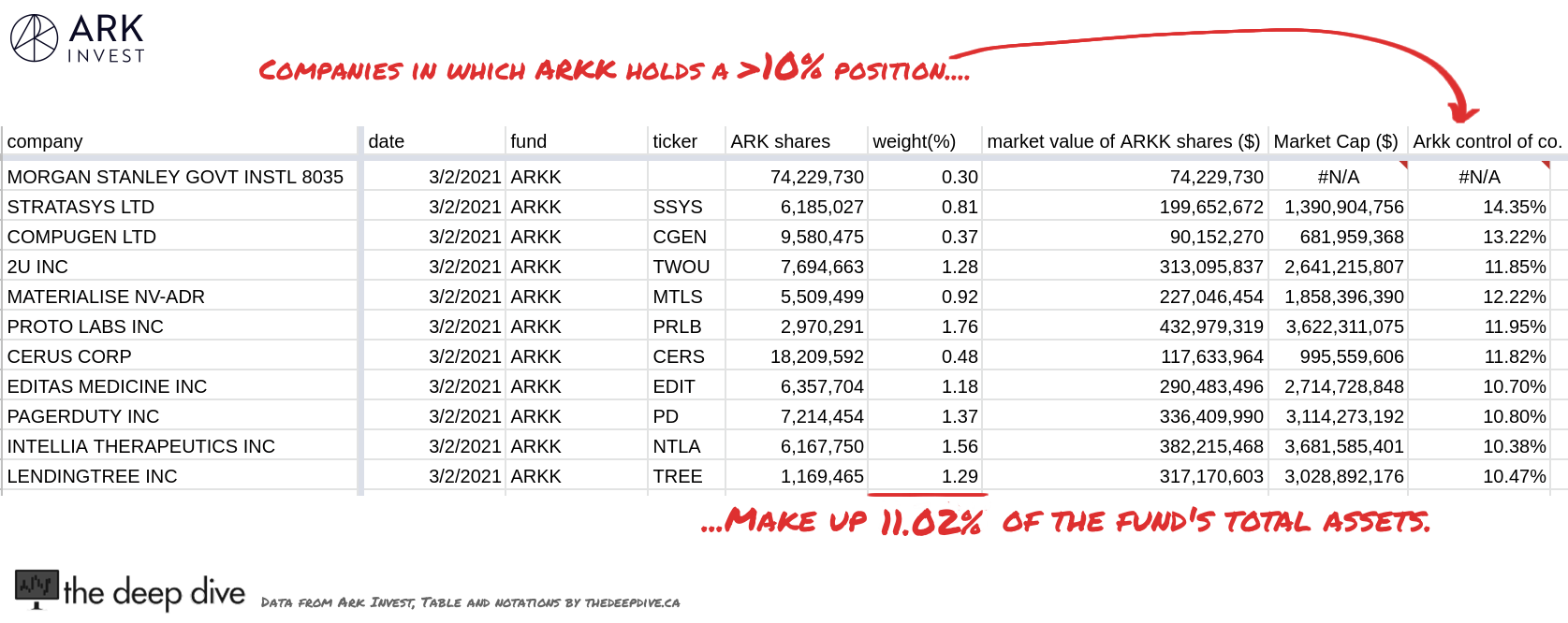

The correction in growth equities has been especially hard on the purpose-built ETFs of ARK Invest which, for the past 12 months, have arguably been the best performing custom equities products of all time.

To hear founder Cathie Wood tell it, Ark’s flagship “Innovation Fund” (NYSEARCA: ARKK) and its sister funds are built to give investors exposure to coming economic disruptions that will cause seismic shifts in the business landscape. The concept isn’t new. In fact, “disruption” loomed so large in the formative years of a whole generation of investors that it’s become a cliché and an easy punch line. But Wood is able to consistently use the term with a confidence that powers through any lingering cringe.

The finance veteran has a certain ability to make concepts that are often delivered in dreamy TED talks come off like foregone conclusions, by grounding them in their potential implications on the broader business landscape. The idea that, for example, the developing field of gene editing would have any kind of near term business application seems far-fetched, and its implications on the healthcare sector in the long-term impossible to predict. But Wood frames the portions of the healthcare sector that aren’t positioned to take advantage of advances in genomics as “black holes” in the global economy.

She describes the portions of the economy that are on the wrong side of the (theoretical, future) seismic shifts being caused by these technologies as the portions that will be saddled with the weight of coming deflation, as they’re out-competed by the companies who were ready. Wood’s conceptual jujitsu has made pure, unadulterated venture-stage growth stories seem like indispensable hedges in a way that even people who know better have to admit is pretty compelling.

Do bears sh*t on Cathie Wood?

Predictably, ARKK did poorly in the final week of February, and to hear Edwin Dorsey, editor of popular substack-based newsletter The Bear Cave tell it, the bears that the fund’s success has been tormenting for more than a year are licking their chops:

Dorsey has been mining Ark’s no-good, very bad week for a rich vein of content, with a thematic focus on the potential that the fund might develop liquidity issues.

Typically, open-end venture tech funds that trade in illiquid small-cap stocks like ARKK does are besieged during market slides with redemption requests, forcing them to sell holdings and contribute to the downward spiral in the equities that are their stock-in-trade. The Bear Cave went into detail on February 23rd about how such an unwinding might happen at Ark, wondering if a rush to the exits might ratchet up short-side pressure on both the portfolio components and the ETF itself. The “Special Edition” report invokes the 2015 unwinding of the Woodford Equity Income Fund, in which redemptions overwhelmed Neil Woodford’s namesake investment product.

Wood remains unconcerned with the threat of mass redemption. The Bear Cave excerpted a quote from one of Cathie’s videos March 4th in which she shrugs it all off without providing any specifics.

Wood has never been one to explain herself, but it would be a mistake to think she’s simplifying for the sake of obfuscation, rather than to keep her message clear. Unlike assets under management with traditional mutual funds, when an investor wants to liquidate their ETF they can sell the shares on the market to a willing buyer. The public issue puts another layer of liquidity between the component companies in Ark’s funds and Ark-proper. This affords Wood and her team an opportunity to get in front of the selling by doing what they do best: creating buying.

ETFs handle redemptions differently than traditional hedge funds, allowing for institutional desks to redeem the ETF units for shares of the underlying securities that make it up, in an effective negative image of the ETF creation process. It opens up the potential for institutional arbitrage when the fund’s NAV and share price don’t line up.

The bear thesis here is that predatory shorts in the individual portfolio names and on the fund itself could create a selling weight that Ark’s promotion can’t keep up with. Dorsey points out that some of the firm’s positions in smaller issues are more delicate, and that it needs to unload shares of its bigger, more established names like Tesla Inc. (NASDAQ: TSLA) and Square Inc. (NYSE: SQ) to rotate into companies to whom it already serves as a cornerstone backer.

For example, between the the Ark Innovation ETF and the Ark Genomic Revolution ETF, the funds are 7% holders of Teladoc Health Inc (NYSE: TDOC), a telemedicine platform company that (surprise!) is out to revolutionize healthcare. Growth has been strong for Teladoc, which saw a 98% year over year jump in revenue in 2020, a year in which it completed $26 billion in acquisitions.

Teledoc’s operations lost $506 million that year on $1 billion in revenue. Concerned as we always are with the adjustments made to adjusted EBITDA, we were fascinated to learn that TDOC’s $506 million 2020 operating deficit included $498 million in G&A expenses, an unknown portion of which were covered by $475 million in share based compensation.

A fresh round of Teladoc S-4s filed March 3rd showed execs unloading relatively small portions of positions accumulated mostly from restricted stock units and performance stock units. CEO Jason Gorevic, for example, ended up having sold a net 4,150 TDOC shares, and is still holding 536,319 shares. Management and bedrock backers being true believers isn’t just an important element of ventures that are able to weather a downturn in sentiment, it’s fundamentally the only element that matters. Companies that don’t make money will need more eventually, and they won’t have a prayer of a chance of raising any if they can’t lead by example to inspire some broader faith.

“Of course we’re sailing into the wind, what did you think this was all about?”

Dorsey’s criticism of Ark’s re-balancing out of some of the more mature ventures and into low liquidity, high-potential issues would be a fine criticism if Ark’s funds were portfolios meant to achieve any sort of balance, but they aren’t. ARKK and its sister funds are purpose built instruments. They’re managed funds, sure, but their labels don’t say they’re being managed to adapt to conditions.

They’re wide-open, risk-on trades meant to offer investors exposure to cutting edge innovation at full-steam-ahead, and damn the torpedoes. Rotating out of names that haven’t yet made their moves to create liquidity would be a tacit admission that the show is over. If a dream-merchant like Wood can’t convince everyone she’s ahead of the curve, then the bull run really is over.

What kind of captain would she be if she telegraphed that she wasn’t ready to go down with the ship?

Information for this briefing was found via Sedar and the companies mentioned. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.

2 Responses

I quite often like to save investment articles as this one, and then come back to again in a few years

It’s hard to make predictions, especially about the future, but one thing is for sure: no matter when you come back to check in on this post, that title card is still going to look RAD.

Thanks for reading.