It seems that when it comes to the Canadian cannabis sector, there always has to be some degree of drama occurring. With the recent closure of the Aurora Cannabis and Cannimed Therapeutics saga, Maricann Group Inc (CSE: MARI) has stepped up to the plate to provide the entertainment.

As you likely know, we have previously reported on the current saga that has embroiled Maricann. Our latest article, issued on the last day of February, addressed the amateur moves the company has made in the past. Furthermore, it also identified the current scandal involving the company. In the time since, Maricann CEO Ben Ward has been focused on damage control – with and without the approval of the board.

The latest instance suggests that a takeover may be looming for the firm after the recent failure of a financing. Ward even went as far as to suggest this in his off the cuff interview with Stockhouse, wherein he stated, “We are also of the opinion this may have also served another hidden agenda, which was to allow one of our competitors to engage in an attempted takeover bid for Maricann, thereby trying to acquire the company on the cheap.”

With that, what value does Maricann provide to a potential takeover target? And what firms would be interested in the embroiled organization?

Maricann: Evidence of a Looming Takeover

The evidence of a Maricann takeover

With respect to a looming takeover, there are three signs that point us to this being a very real possibility for Maricann. This is predicated on comments made by the CEO, Ben Ward, as well as information contained in recent Globe and Mail articles.

- In the first Globe and Mail article related to the current scenario, it was mentioned that in addition to the OSC investigating two directors of Maricann, Ben Ward himself was under investigation. However, Ward’s investigation is not material to the current situation. This investigation is in relation to his tenure as the chief executive officer of Canadian Cannabis Corp, a role he filled before his time at Maricann. The release of this information is arguably intentional slander to reduce investor confidence in the CEO.

- Ben Ward himself, as previously mentioned, directly stated this as a possibility in his interview with Stockhouse. Through the use of this information is he of the opinion that a takeover bid by an undisclosed third party may be at play.

- Clay Horner, counsel to the special committee of Maricann. Who is Clay Horner? Clay is regarded as one of the top ten merger and acquisition lawyers in the world, and is a retired partner of Osler, Hoskin & Harcourt LLP (“Osler”). A full biography on him can be found here.

Although all points listed above are highly relevant evidence for a potential takeover of Maricann, it’s the last point that drives this home. Based on our Deep Dive, we have concluded that McKesson Canada has utilized Osler in the past for it’s legal matters. The most recent documentation of this can be found in this Financial Post article, wherein it directly states that a team member of Osler was representing McKesson in a court case.

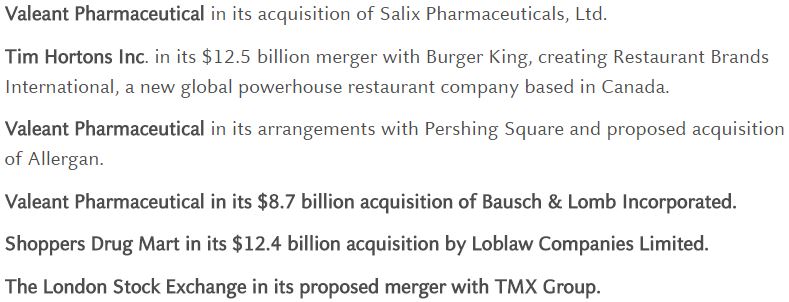

With Clay Horner being a former partner of the firm, it appears that he has stepped out of retirement to fill a role for a large client. Let’s make this clear. Lawyers of Horner’s caliber don’t typically bother with M&A cases involving CSE listed companies. Instead, he’s more accustomed to mergers ranging in the billions of dollars. Here’s a small screenshot of some of his recent cases.

The short of it is this. At Horner’s level, his services do not come cheap. A company of Mari’s size does not concern him, and such a transaction doesn’t even amount to a walk in the park. Instead, it is highly likely that he is involved at the request of McKesson Canada, after the turbulence Maricann has recently experienced. And with such money being spent, it’s unlikely that a merger or acquisition won’t happen.

The value Maricann provides to a potential takeover

Although Maricann has a relatively small market capitalization currently, a portion of this is a function of the trouble the company has seen lately. And that’s not to say it does not have desirable aspects. Maricann has solid assets, and perhaps the weakest link is the current management in place at the firm. Here’s what Maricann brings to the table.

- A facility currently producing 22,500 KG annually. This facility is also presently under expansion, and will be 942,000 square feet when fully built out. Production estimates are pegged at 95,000 KG of dried cannabis flower per year, at an average cost per gram of $0.60.

- A German facility, which is presently under retrofit. In all the facility can boast up to 820,000 square feet in grow rooms once fully built out. It also has surrounding land that will enable the production of hemp. This facility and it’s associated subsidiary is currently in the licensing process.

- NanoLeaf Technologies, a subsidiary with proprietary technology related to the bioavailability and solubility of cannabinoids in liquid. The flagship product, Vesisorb, is already in use in a number of products across diverse industries.

- Haxxon Ag, a Swiss based company focused on providing refined cannabis products. Their product line up includes cannabis cigarettes free of tobacco, and cannabis vape cartridges among others.

- Definitive agreement with McKesson Canada, a company whom controls 2,116 pharmacies (20.01% of pharmacies) across Canada, to jointly establish a pharmacy services program related to cannabis.

The true value in Maricann, as you likely already knew, lies in the deal it has established with McKesson Canada. This is largely what any firm jockeying for a takeover will desire in Maricann. Yes, it has a large facility under construction, and soon to be established European operations. However, the real asset is the role the company serves in the largest pharmacy chain in the country. Acquiring 20% of the market with one purchase is huge. And desirable.

Potential candidates for acquiring Maricann

With all that being said, whom is the ideal candidate for the acquisition of Maricann? Two prevailing theories have played out across social media. First, the big three have been eliminated from the equation: Aphria, Aurora Cannabis, and Canopy Growth. Aphria, due to their recent acquisition of Nuuvera. Aurora, due to their recent investment in The Green Organic Dutchman is out as a result of cash availability. As for Canopy Growth, there’s little to benefit from a Maricann acquisition.

What has been highlighted as a possibility however, is McKesson Canada itself, as well as The Hydropothecary.

- McKesson Canada

For some reason, many investors appear to believe that it is McKesson itself that is aiming to take over Maricann. As evidence, they point to the current involvement they already have in the company. There’s also the consideration of the bad press that Maricann has provided them in the past. Lastly,, many state that it might be a “quiet, background takeover.”

This is highly unrealistic. First, when it was announced that McKesson was in a deal with Maricann back in August, the news release had to be yanked almost immediately. As a result of McKesson’s U.S. operations, the firm cannot be openly associated with a cannabis organization. This is a result of the plant remaining a Schedule 1 drug in the country. As is, the release had to be re-issued citing an unnamed party. In the current political environment, there is no way in which such a takeover could occur. Furthermore, due to exchange requirements there is no such thing as a “quiet takeover,” filings are required to occur in these instances.

- The Hydropothecary (TSXV: THCX)

The most dominant theory, is that a takeover by The Hydropothecary will occur. There are a number of reasons this has been speculated by the masses. First and foremost, Ben Ward and The Hydropothecary have a history. When in the role of CEO for Canadian Cannabis Corp, Ben Ward had negotiated the acquisition of The Hydropothecary for a total of $21.3 million. However, the deal went sour and never occurred.

It should also be noted that John Esteireiro, head of equities at Eight Capital served under Ward as chief operating officer at Canadian Cannabis Corp during the time of this deal. Eight Capital is one of the recent underwriters of the $70 million bought deal that was cancelled. The Hydropothecary also utilizes Eight Capital as an underwriter, most notably in the recent $100 million raise conducted by the firm.

In terms of operational alignment, there are several key areas in which Maricann would benefit The Hydropothecary. Most dominantly of which, is it would expand THCX’s presence both within the country as well as globally. The firm is currently entirely focused within the province of Quebec, and management has gone on the record indicating that they are looking to expand their reach. A 95,000 KG per annum facility in Ontario, as well as a massive facility in Germany would fit that bill nicely.

The Hydropothecary prides itself on producing a premium product for its consumers. Through the licensing deals Maricann has signed with JuJu Royal, and Rare Dankness, this would be the perfect avenue to build upon that focus.

Lastly, the acquisition of Maricann would propel the Hydropothecary into becoming a major player within the industry. With the production capacity of over 200,000 KG per annum, as well as the European assets, it would be difficult to not consider the company a major competitor. Not to mention the proprietary products the company would have through their combined forces. Finally, the product distribution stream that would become available to THCX is invaluable. Let’s also not forget that Hydropothecary is cashed up as a result of a recent $100 million financing.

Closing Remarks

One final point to make, is that there are signs of a breakdown among the management team of Maricann. With Ben Ward’s recent interview with Stockhouse, and the resulting press release indicating that it was unauthorized, there’s events occurring behind closed doors. Whether this is a disagreement between members of management that want to sell and those that don’t, or just a ploy to settle investors in the wake of the bombshells dropped last month is anyone’s guess.

However, where there’s smoke, there’s likely fire. All evidence that has been presented to us thus far points to a takeover, hostile or not, occurring for Maricann. The likely involvement of McKesson Canada through the use of Clay Horner is the final indicator that undeniably drives this theory home.

In any event, with McKesson stepping in to take control of the situation, one thing is clear.

Amateur hour is over for Maricann. Dive Deep.

Information for this analysis was found via Sedar, The CSE, New Cannabis Ventures, The Financial Post, The Globe and Mail, Osler, Hoskin & Harcourt LLP, and Maricann Group Inc. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security.