Last week Meta Platforms (NASDAQ: FB) reported its first quarter financial results. The company saw its revenue grow 7% year over year to $27.9 billion, slightly below the analyst consensus. The company was not able to escape inflation, as total costs and expenses grew 31% to $19.38 billion as the company grew its headcount by 28% year over year.

This brought the company’s operating income to $8.5 billion, down 25% year over year while their operating margin fell from 43% to 31%. The company also saw both its net income and earnings per share drop by 18% and 21%, respectively.

The company reported family daily active people of 2.87 billion, and family monthly active people of 3.64 billion, both up 6% year over year. The company said it now has 1.96 billion daily active users on its platform, up 4% while its monthly active users grew slightly slower at 3% year over year to 2.94 billion.

Meta stated that its ad impressions increased by 15% while its average price per ad decreased by 8%. Additionally, the company said that they repurchased $9.39 billion of stock in the first quarter and still had $29.41 billion available in their current repurchase program.

Lastly, the company provided second quarter guidance. Meta Platforms expects to see total revenue between $28 and $30 billion, saying, “this outlook reflects a continuation of the trends impacting revenue growth in the first quarter, including softness in the back half of the first quarter that coincided with the war in Ukraine.” Additionally, they expect full-year 2022 total expenses to be between $87 and $92 billion, which is lower than their previous full-year guidance of $90 to $95 billion.

A number of analysts changed their 12-month price targets on Meta Platforms, bringing the average 12-month price target down to $303.87 from $324.22, which represents a roughly 50% upside to the current stock price. Meta has 63 analysts covering the stock, of which 17 analysts have strong buy ratings, 29 have buys, 16 have hold ratings and a single analyst has a sell rating on the stock. The street high price target sits at $553 which represents an almost 170% upside to the current stock price.

In Canaccord Genuity’s note on the results. they reiterate their buy rating but lower their 12-month price target on the stock to US$330 from US$360, saying that a combination of “expected and unforeseen factors contributed” to slowed sequential growth. Such as slowing spending from eCommerce advertisers, Apple’s privacy changes, and a challenging macro backdrop.

While the Russian invasion of Ukraine added to the companies advertising uncertainty in Europe, Canaccord says that “forward-thinking investments” in each of Meta’s segments are putting the company in a great position for sustained long-term growth despite the headwinds the stock and company is currently facing.

Canaccord is attributing those headwinds to the slowdown in growth as Q1 ad revenue grew roughly 6% year over year to $27 billion, which was slightly below their estimate. Though the company saw a lift in impressions, growing 15% year over year, the price per ad declined roughly 8% year over year.

Canaccord says that these results could be mainly attributed to the Russia-Ukraine war, in which Facebook was banned in Russia and the war slowed advertiser spending in Europe.

Though Canaccord remains bullish on some aspects of Meta’s products, as they report that Instagram Reels make up more than 20% of the screen time on Instagram, and Reels is currently not being monetized.

On Meta’s daily/monthly active users, Canaccord says that the results on this end were solid, even after factoring in the macro factors, with DAUs growing 4.4% and MAUs growing 2.9% year over year. Most notably, Meta saw sequential growth in all regions except Europe. Canaccord expects Meta to continue its investment in algorithms, which they believe the company will then leverage these improvements into all content verticals across it’s apps.

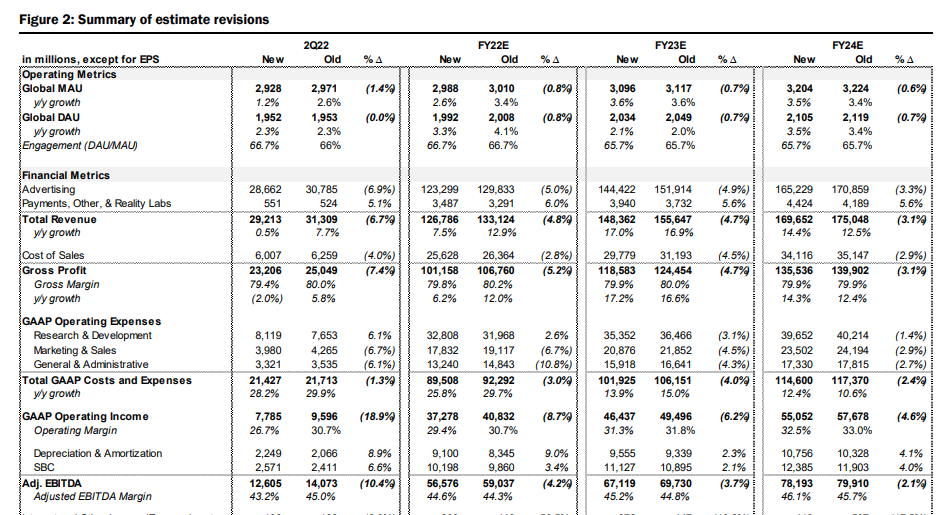

Below you can see Canaccord’s updated 2022 to 2024 estimates.

Information for this briefing was found via Sedar and Refinitiv. The author has no securities or affiliations related to this organization. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.