Originally published on the SmallCapSteve Substack.

Back in 2022, when most of the financial class was still pretending the world could be understood through CPI prints, Fed dot plots, and whatever nonsense was coming out of Jackson Hole, Zoltan Pozsar was talking about something far more important:

Protection.

Not in the ESG consultant sense. Not in the “buy some puts” sense. He meant actual protection. Navies. Pipelines. Sea lanes. Sanctions. The legal and military architecture that makes a barrel of oil, a ton of copper, or a cargo ship full of LNG worth anything in the first place.

At the time, this sounded a little dramatic. Today, it sounds obvious.

Pozsar’s real insight was not that inflation was going up, or that commodities mattered, or that the dollar might face some long-term challenges. Lots of people said some version of that. His insight was deeper: the global monetary system was no longer just pricing money. It was starting to price security.

That is a very different world.

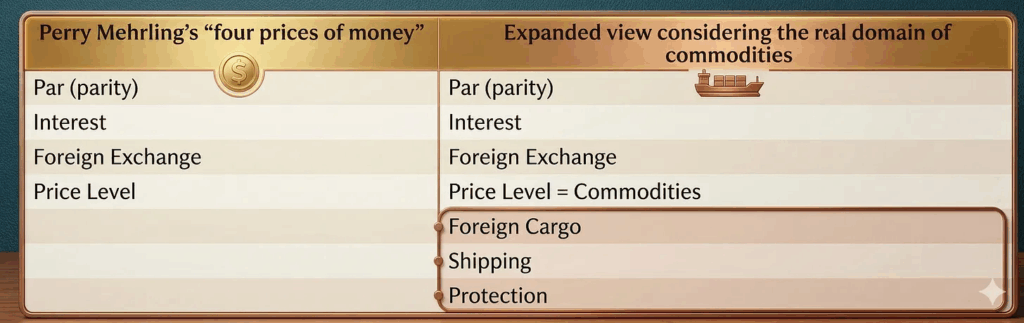

In one of his most important 2022 notes, Pozsar took Perry Mehrling’s classic framework of the “four prices of money” and expanded it. He added foreign cargo, shipping, and protection. In other words, the cost of money was no longer just about interest rates, foreign exchange, and the price level. It was also about whether the physical stuff behind the balance sheet could actually move, arrive, and be defended.

That sounded niche in March 2022. It does not sound niche anymore.

Because what has the last four years actually been about?

Not “higher for longer.” Not “soft landing.” Not “AI productivity.” Those are side quests.

The real story has been that the world discovered, in rapid succession, that reserve assets can be frozen, pipelines can be sabotaged, shipping routes can be choked, energy systems can be weaponized, and supply chains optimized for peace become liabilities in a geopolitical divorce.

That was Pozsar’s point. The system did not suddenly become short of money. It became short of trust.

And once trust breaks, the market starts repricing everything.

It reprices where countries store reserves.

It reprices who they buy energy from.

It reprices whether just-in-time inventory is actually efficient, or merely suicidal.

It reprices whether “cheap” imports are still cheap once you include political dependence.

It reprices gold.

And yes, it reprices protection.

The mainstream financial take in 2022 was that the freezing of Russia’s reserves was a one-off act of punishment. Pozsar saw something bigger. He argued that this was a regime change. If a G20 central bank could wake up and discover that a meaningful chunk of its reserves was not really money, but a conditional claim dependent on political alignment, then the definition of a safe asset had just changed.

That was the beginning of the Bretton Woods III argument.

People got hung up on the branding. They heard “Bretton Woods III” and imagined some clean, cinematic handover where the dollar gets wheeled out on a stretcher while a gold-backed BRICS supercurrency descends from the heavens like the monetary messiah.

That part was always a little too neat.

The dollar has not died. Not even close. IMF data published in March 2026 still show the U.S. dollar making up 56.8% of disclosed global foreign exchange reserves in the fourth quarter of 2025. The renminbi, despite all the breathless de-dollarization chatter, was still under 2%. And the dollar remained on one side of 89% of global FX transactions in 2025.

So if you want to say Pozsar was wrong because the dollar did not collapse, fine. But that is a lazy reading of what he was actually saying.

He was directionally right in the way that matters.

Look at gold.

Gold is not replacing the dollar tomorrow morning. But it is being rediscovered for what it has always been: an asset without counterparty risk, without a sanctions committee, and without a keyboard in Washington that can make it vanish.

Again: protection.

Or rather, protection from the absence of protection.

And that is where the Hormuz story matters.

For decades, the dollar system did not just rest on America having the deepest capital markets. It rested on a deeper assumption: that the United States, for all its flaws, would ultimately underwrite the arteries of global commerce. The reserve currency issuer was also the maritime backstop. That was the deal, whether anyone said it out loud or not.

Now imagine that assumption breaking.

Iran has shown that a regional power can still choke a waterway that carries roughly a fifth of global oil and gas flows. Some ships have been allowed through, especially those seen as less hostile or less directly tied to Washington’s war effort, while the broader message remains the same: passage is political now. And Trump’s own rhetoric has only reinforced the uncertainty, at times insisting the U.S. could reopen the strait, and at other times saying that securing it is “not for us” and that other countries should figure it out themselves.

That is a much bigger story than oil.

Because if Washington is no longer willing, or no longer able, to reliably guarantee the flow of trade through critical chokepoints, then protection itself stops being a background assumption and becomes an explicit cost.

The old world is gone.

The new one is messier. More regional. More paranoid. More redundant. More inflationary. More strategic.

And much more honest about what money actually depends on.

Because in the end, Pozsar’s great 2022 insight was not that money was becoming backed by gold, or oil, or wheat.

It was that money was becoming backed, once again, by power.

And power, unlike central-bank rhetoric, has a very real price.

Information for this story was found via the sources mentioned. The author has no securities or affiliations related to the organizations discussed. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.