On June 8, Dollarama Inc (TSX: DOL) reported its fiscal first-quarter financial results for 2023, for the period ended May 1, 2022. The company saw its revenues grow almost 13% to $1.073 billion, while its cost of sales grow roughly the same to $620.99 million. Though operating income grew almost 25% to $220 million.

The company also reported its EBITDA grew 21% to $300 million, for a margin of 28% of sales. While diluted earnings per share were up 33%. Comparable store sales grew 7.3% year over year.

The company ended the quarter with $71.57 million and $646.7 million in inventory. Dollarama announced that they purchased 1,444,803 shares during the first quarter for total consideration of roughly $107.3 million under their normal course issuer bid.

Dollarama currently has 15 analysts covering the stock with an average 12-month price target of C$78.71, or an upside of 10%. Out of the 15 analysts, 1 has a strong buy rating, 9 have buy ratings and 5 analysts have hold ratings on the stock. The street high price target comes in at C$82 from 3 analysts which represents an upside of about 13%.

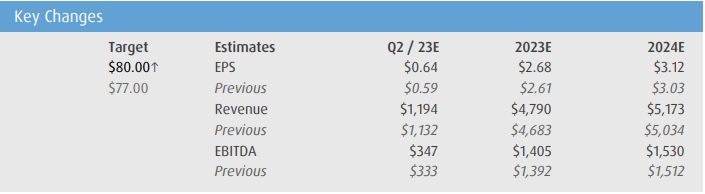

In BMO Capital Markets’ note on the results, they reiterate their outperform rating and raise their 12-month price target from C$77 to C$80, saying that this quarter was strong and highlighting “Dollarama as a value destination.”

On the results, Dollarama beat BMO’s earnings per share by $0.03 while they highlight that Dollarama’s same-store sales growth has been the highest growth, even compared to quarters during the pandemic. Of the 7.3% growth, it was compromised of 14.4% growth in traffic while a 6.2% decline in transaction baskets.

BMO writes, “This strength in traffic may be highlighting the draw of Dollarama’s compelling customer proposition as customers seek value in overall increasing cost-of-living inflation.”

They also highlight Dollarama’s gross margins of 42.1%, which was in line with their estimate of 42%. A 0.15% decline year over year, they note that this is surprisingly strong mainly due to management’s cautious guidance and positioning heading into the quarter.

Management noted that there was 20-30bps of margin expansion during the quarter primarily due to lower logistics costs as a result of shipment delays. Management also talked a lot about wage pressures during the earnings call, which they indicated were higher but noted that it’s regional in nature.

Lastly, BMO says that this quarter highlights the idea that Dollarama is resilient during times of high inflation and that the company is “relatively better positioned versus other retailers to navigate through a period of inflation due to its unique structure and capabilities.”

Below you can see BMO’s updated estimates.

Information for this briefing was found via Sedar and Refinitiv. The author has no securities or affiliations related to the organizations discussed. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.