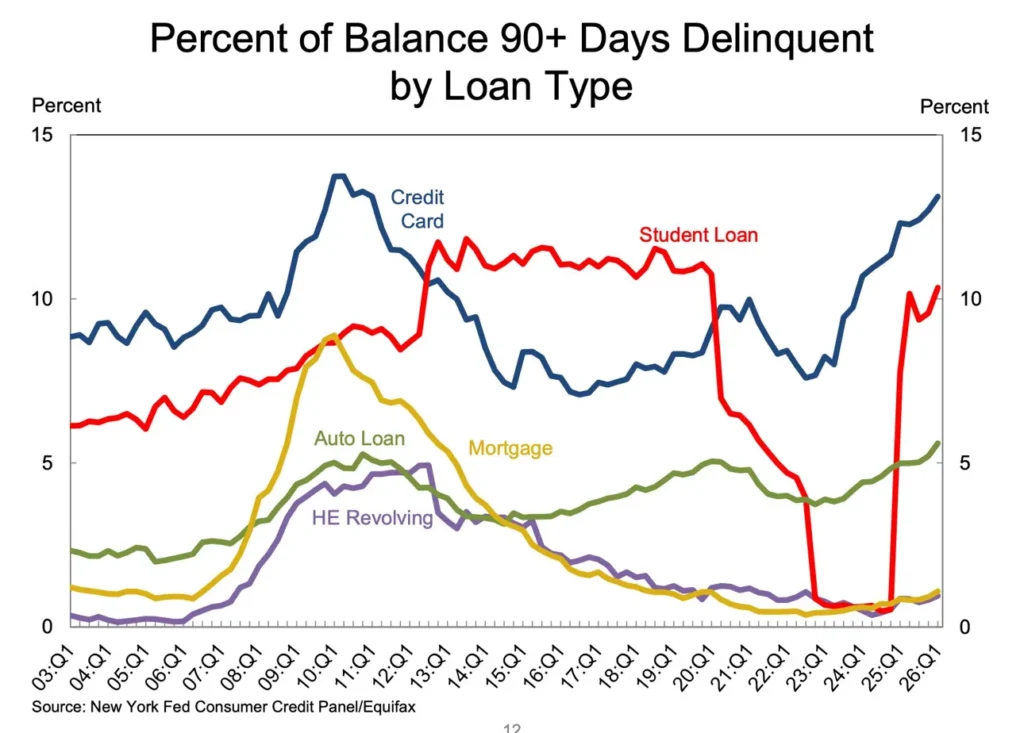

On the surface, the Federal Reserve Bank of New York’s Q1 2026 household debt report delivered good news on credit cards: balances fell $25 billion to $1.25 trillion, and the early delinquency rate ticked down from 8.7% to 8.6%. A seasonal paydown after holiday spending, delinquency trends are moving in the right direction.

The surface is misleading.

Credit card balances remain $70 billion above where they were a year ago — a 5.9% year-over-year increase — and average interest rates of 21% on all cards and 21.52% on cards carrying a balance mean that for millions of households, those balances are compounding faster than they can be paid down.

Related: US Household Debt Hits $18.8 Trillion as Student Loan Delinquencies Surge

The aggregate improvement in delinquency rates masks a widening split between two groups of borrowers living in fundamentally different credit economies.

“Americans are generally on pretty stable footing, overall, but we do see some weakness in lower-income households,” NY Fed researchers said on a press call Tuesday. “We do see some of this in our delinquency rates.”

Christian Floro, market strategist at Principal Asset Management, put it more directly: “A subset of consumers, primarily subprime borrowers, has driven most of the increase in delinquencies, while prime borrowers have experienced only a marginal deterioration in credit performance.”

That divergence — stable at the top, stressed at the bottom — is the defining feature of what economists are calling a K-shaped credit economy. Higher-income households maintained their level of spending in March even as lower-income families were forced to cut back on gas consumption and reported increased financial strain, according to a separate NY Fed consumer spending report released earlier this month.

The bifurcation has been building since 2021, when credit card balances bottomed out at $770 billion during the pandemic. They have since risen 66% — but the burden of that increase has not been distributed evenly.

The pressure point most likely to change the picture: gas prices. A gallon of regular gasoline averaged $4.50 nationally on Tuesday — up from $3.14 a year ago, a 43% increase driven almost entirely by the US blockade of Iranian ports following Operation Epic Fury in late February.

Floro warned that “the latest gasoline price shock could push delinquencies higher,” particularly among lower-income households where fuel costs represent a disproportionate share of monthly budgets. The April Consumer Price Index, released Tuesday, showed inflation rose for the second consecutive month to 3.8% — a three-year high — with energy and groceries as the primary drivers.

Read: U.S. Inflation Surges to 3.8% in April, Highest Since May 2023, as Energy Costs Soar

Against that backdrop, a CNN/SSRS poll found 70% of Americans disapprove of how Trump is handling the economy — the highest number the pollster has recorded across both of his terms. A PBS/NPR/Marist poll found 63% blame Trump for high gas prices.

Asked on the White House lawn on Tuesday, before departing for Beijing, whether Americans’ financial situations were motivating him to reach a peace deal with Iran, President Trump was unequivocal: “Not even a little bit. I don’t think about Americans’ financial situation. I don’t think about anybody. I think about one thing — we cannot let Iran have a nuclear weapon.”

Information for this story was found via the sources and companies mentioned. The author has no securities or affiliations related to the organizations discussed. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.