Canada now has two recession scoreboards, and they are not giving the same answer.

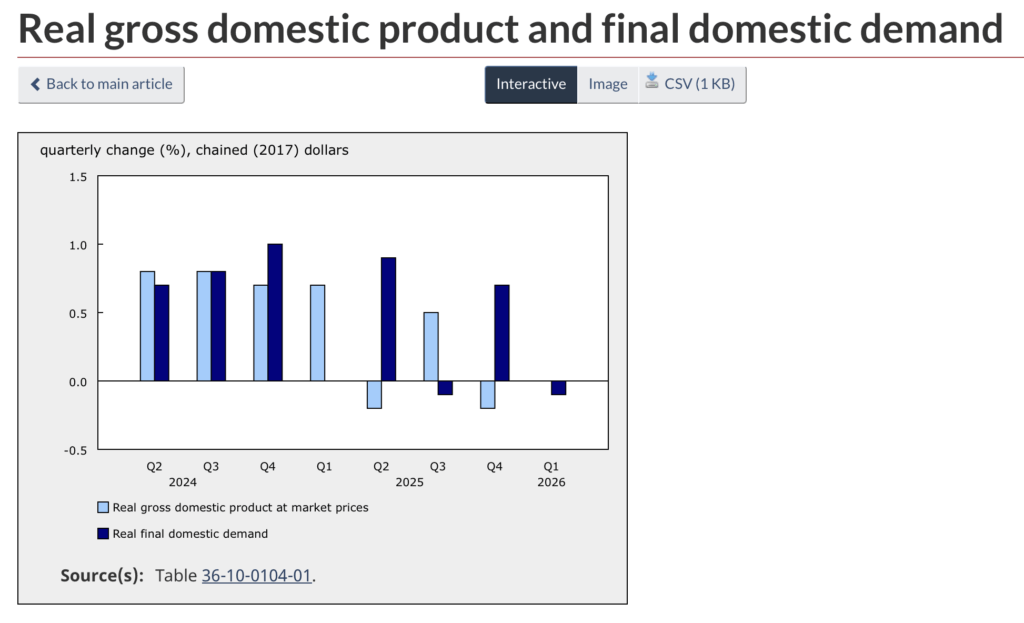

On the first scoreboard, the economy has already tripped the market’s recession alarm. Real GDP fell at an annualized 0.1% rate in the first quarter of 2026 after a revised 1.0% decline in the fourth quarter of 2025, putting Canada into back-to-back negative quarters on that measure, as per Reuters.

That is enough for the common technical-recession label used by investors, economists, and headline writers.

On the second scoreboard, the case is weaker. Statistics Canada’s expenditure-side GDP was unchanged in Q1 when measured quarter to quarter, while GDP by industry rose 0.1%. Services-producing industries grew 0.3%, offsetting a 0.4% drop in goods-producing industries.

That split is the heart of the recession debate. Canada is not growing with any real momentum, but the contraction is not yet broad enough across the data to make the official call obvious.

The pressure is concentrated in the economy’s more rate-sensitive and trade-exposed corners. Residential investment fell 2.0% in Q1 after dropping 2.4% in Q4, with ownership transfer costs down 9.9% as resale activity weakened. Exports slipped 0.1%, with fewer passenger car and light truck exports tied to US tariffs. Final domestic demand also edged lower, falling 0.1%.

But the economy did not roll over cleanly because consumers and inventories absorbed part of the hit. Household spending rose 0.4% in Q1 after a 0.7% increase in Q4, led by financial services and food. Inventory accumulation also helped cushion the quarter, while higher crude oil, crude bitumen, and natural gas shipments partly offset export weakness.

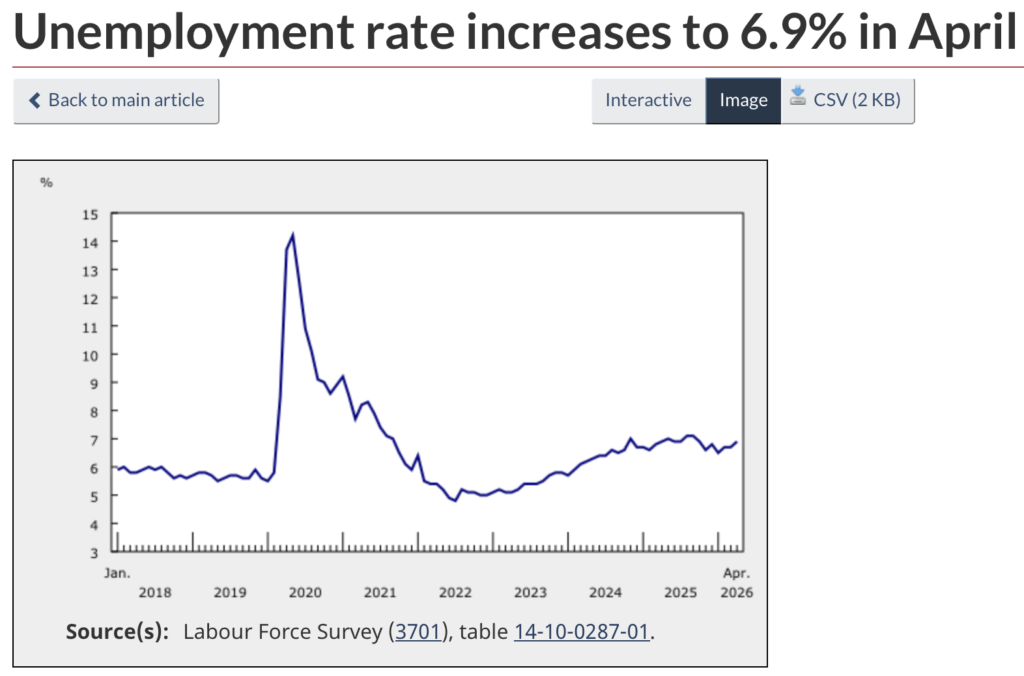

The more important recession test may now move from GDP tables to paycheques. Canada’s unemployment rate rose to 6.9% in April, up 0.2 percentage points from March. The labor market has not collapsed, but it has weakened enough to make the technical-recession label feel less academic for households.

The Bank of Canada is treating the GDP signal as a warning, not a verdict. In a Reuters report, Senior Deputy Governor Carolyn Rogers told lawmakers that the numbers met one technical definition of recession, but she argued the central bank needed to look beyond a single indicator. She also pointed to Statistics Canada’s advance estimate showing GDP likely rebounded 0.4% in April.

That April estimate is the escape hatch in the recession argument. If confirmed, it would suggest the Q4 and Q1 weakness may have reflected a shallow interruption rather than the start of a deeper contraction. Statistics Canada said the preliminary April gain was led by mining, quarrying, oil and gas extraction, manufacturing, and wholesale trade.

The official recession bar in Canada is higher than the two-quarter shortcut. The C.D. Howe Institute’s Business Cycle Council defines a recession as a pronounced, persistent, and pervasive decline in aggregate economic activity, using depth, duration, and breadth rather than one mechanical GDP rule.

For now, the most accurate answer is conditional: Canada is in a technical recession on annualized quarterly GDP, but it has not clearly entered a broad, officially recognized recession. The next confirmation will not come from the label. It will come from whether April’s rebound holds, whether unemployment keeps rising, and whether household spending finally loses altitude.

Information for this story was found via the sources and companies mentioned. The author has no securities or affiliations related to the organizations discussed. Not a recommendation to buy or sell. Always do additional research and consult a professional before purchasing a security. The author holds no licenses.